Deep Tide Summary: While Saylor was shouting to increase the per-share BTC content, he was issuing new shares below the breakeven point, and only used half of the raised funds to buy BTC at a price lower than the breakeven point. This is not buying the dip; this is subsidizing STRC's sustainability with MSTR shareholders' interests. For MSTR investors, understanding the logic behind this transaction is more important than focusing on how much BTC was purchased.

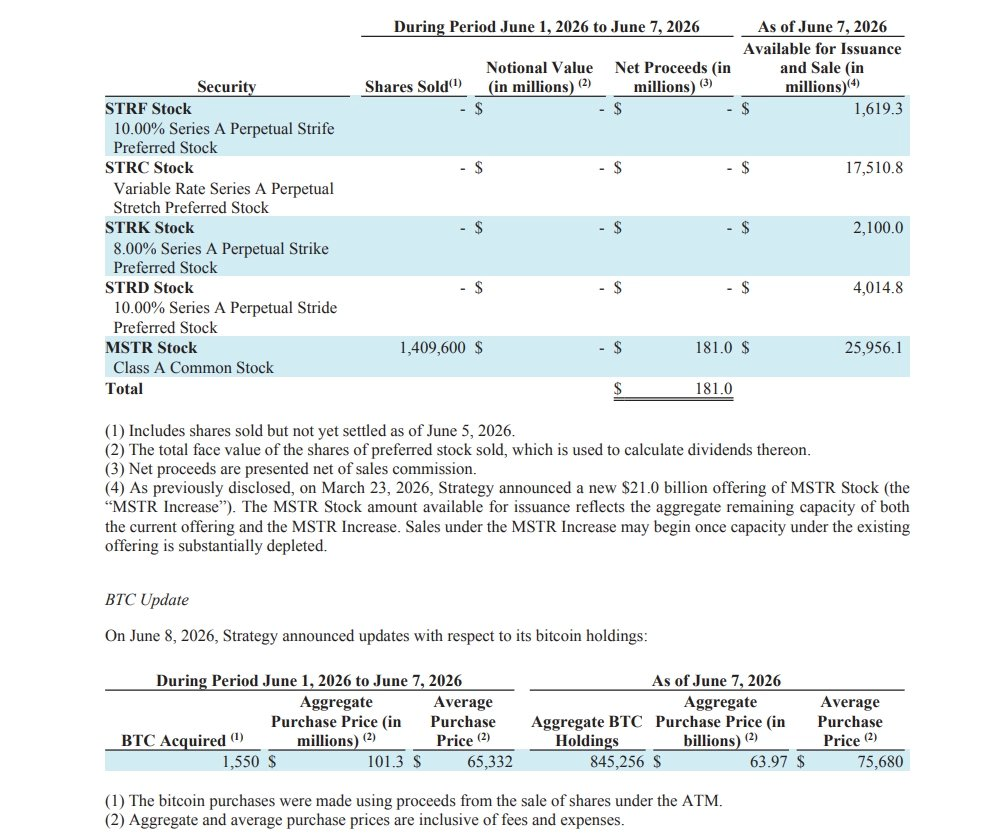

Saylor first sold 32 BTC and then turned around to buy 1,550 BTC today.

I don't want the strategy to fail. But some things must be clarified.

This is one of the worst trades.

Superficially, this transaction looks good. The strategy bought a large amount of BTC at recent lows and even increased the preferred stock dividend dollar reserve from $900 million to $1 billion.

Is this the resurrection of the strategy?

If you think this is good news, it means you still don't understand the strategy.

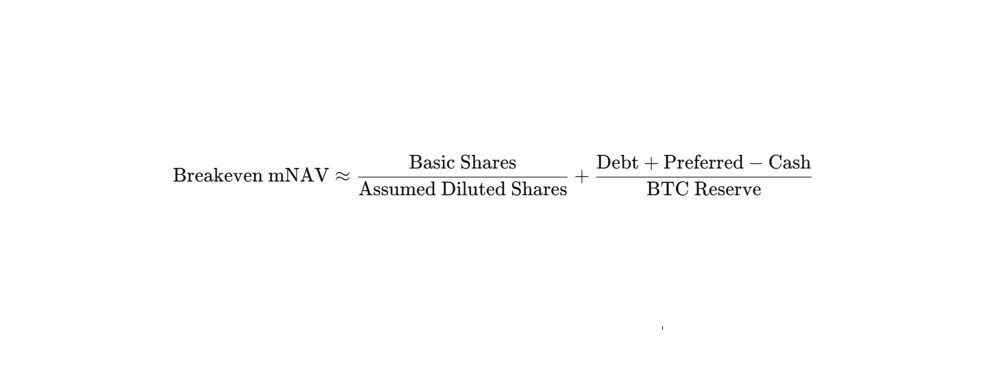

1. You Need to Understand Breakeven mNAV

One of the core goals of the strategy is to increase the per-share BTC content (BPS) for MSTR shareholders.

The method to increase BPS is simple: issue common stock at a premium and then use the raised funds to buy BTC.

So, what premium does MSTR need to truly increase BPS through ATM issuance?

According to the Q1 2026 earnings call, the mNAV needs to be above 1.22.

This is the so-called 'breakeven mNAV'.

This concept stems from a simple condition: the BTC that can be bought with the sale of 1 share of MSTR must be greater than the current BTC amount per share of MSTR.

You can refer to my previous article for a full derivation process.

Ultimately, the calculation method for breakeven mNAV is as follows:

By the way, the current breakeven mNAV is no longer 1.22.

Based on the data prior to the purchase of 1,550 BTC, I have calculated a result of 1.30.

2. The Worst Trade

Now, let's go back to the purchase of 1,550 BTC by Strategy.

Strategy raised $181 million through MSTR's ATM offering, of which $101.3 million was used to purchase 1,550 BTC.

There are two issues here:

First, it appears that MSTR's ATM offering was conducted at a price below 1.30 mNAV. Selling shares below the breakeven mNAV to buy BTC does not enhance the BPS but dilutes it.

Second, and this is crucial: not all of the ATM raised funds were used to purchase BTC. The whole concept of breakeven mNAV is based on the assumption that 100% of the raised funds are used to buy BTC. Even if the mNAV is high enough, if only a portion of the funds flow into BTC, this transaction could still drag down the BPS.

Strategy seems to have injected the remaining unused funds into the USD reserve.

In other words: Strategy sacrificed MSTR shareholders' stake and BPS to maintain the sustainability of STRC.

In fact, after this trade, Strategy's BPS decreased by about 0.19% compared to before the transaction.

What did they get in return?

The available time of the USD reserve has been extended from approximately 6.3 months to 7 months.

3. Strategy's Bet

“Our goal is to drive up the per-share BTC content, and we are doing everything we can to increase the per-share BTC content.”

This is what Michael Saylor said during the Q1 2026 earnings call.

However, in this transaction, Strategy sacrificed MSTR's BPS for STRC.

Strategy has already rolled the dice.

If sacrificing BPS can reverse market sentiment, restore STRC's price, and recover mNAV, then Strategy will be able to continue fundraising through MSTR and STRC's ATM issuance.

But what if the sentiment does not improve?

Then Strategy may have no choice but to continue sacrificing MSTR.

In the worst-case scenario, it will either delay STRC's dividend distribution...

or slowly bleed out.

Let's pray for the recovery of BTC, MSTR, and STRC.

Amen.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia