Editor's Note: Against the backdrop of escalating geopolitical conflicts, the market's focus is quietly shifting. Initially, discussions centered around oil price shocks and the Middle East situation, but as the war reached a stalemate phase, a more systemic variable started to emerge: financial conditions themselves are tightening.

The core argument presented in this article is that what is truly driving the current market is no longer the war itself but the disorder in the bond market.

Over the past month, the U.S. 10-year Treasury yield has risen rapidly, directly reshaping rate expectations from a "rate cut trajectory" to "rate hike reconsideration," suppressing the stock market, commodities, and policy space. In this process, the ongoing weakness in the labor market and the re-emergence of inflation expectations have amplified the Federal Reserve's dilemma.

Of more significance, the author places this round of market volatility within the policy response function: as yields approach the "policy shift range" of 4.50%-4.70%, the probability of government intervention will significantly rise. Whether it's historical tariff suspensions or recent changes in the "peace negotiation" rhythm, they are interpreted as specific manifestations of bond market pressure transmitting to the policy level.

This also raises a deeper question: when the bond market begins to dominate asset pricing and policy rhythm, what signals should market participants follow? The geopolitical narrative or the marginal changes in the interest rate curve?

In this round of structural transformation, this article attempts to provide a clear answer—keep an eye on the bond market. Because it not only reflects risk but also determines the boundaries of risk.

The following is the original text:

As peace talks for the Iran war stall, a pressing question is emerging in the U.S. market: the bond market is "malfunctioning." Amidst the severe turmoil in the bond market, we believe the probability of "intervention" is rapidly rising. What does this mean? Let's explain below.

Before we begin, we recommend you bookmark this article as it will serve as a reference guide for the market trends in the coming weeks.

When the Iran war broke out on February 28 (starting with the U.S. and Israeli assassination of Iran's Supreme Leader, Khamenei), the initial oil price surge was less than 15%. The U.S.'s assessment at the time was that the assassination of Khamenei would quickly lead to a regime change in Iran, resulting in a relatively fast and minimally disruptive outcome. However, fast forward to now, the Iran war has entered its 27th day, Iran has rejected the U.S.'s "15-point peace plan," and peace talks have clearly stalled.

The current situation makes it impossible to determine if any party still explicitly wishes to end this war. As a result, oil prices remain elevated, with WTI crude oil price once again approaching $100 per barrel. However, this is no longer the primary concern in the market. The real issue has shifted to the bond market, rapidly evolving into the biggest obstacle to the global economy.

Core Issue

During the early stages of the war, oil prices were the market's focal point and continue to be so to this day. The reason is simple: the oil market most directly and rapidly reflects the impacts of the war.

But now, the larger problem is the sudden surge in U.S. Treasury bond yields.

As shown below, within the 27 days since the Iran war broke out, the U.S. 10-year Treasury bond yield has risen from around 3.92% to 4.42%, marking a cumulative increase of 50 basis points. It is worth noting that prior to the war, the market's focal point of discussion was: How many rate cuts will there be in 2026?

The current rapid rise in the U.S. 10-year Treasury bond yield, and more broadly in Treasury yields overall, is roughly akin to the performance seen during the "Liberation Day" in April 2025.

However, this time the backdrop is much more complex, and stabilizing the bond market is far from being as simple as it seems on the surface. This is quickly becoming the most central narrative in the market.

From Rate Cut Expectations to Rate Hike Pressure

To better understand the magnitude of this dramatic shift, one can review the market's interest rate expectations at the end of 2025.

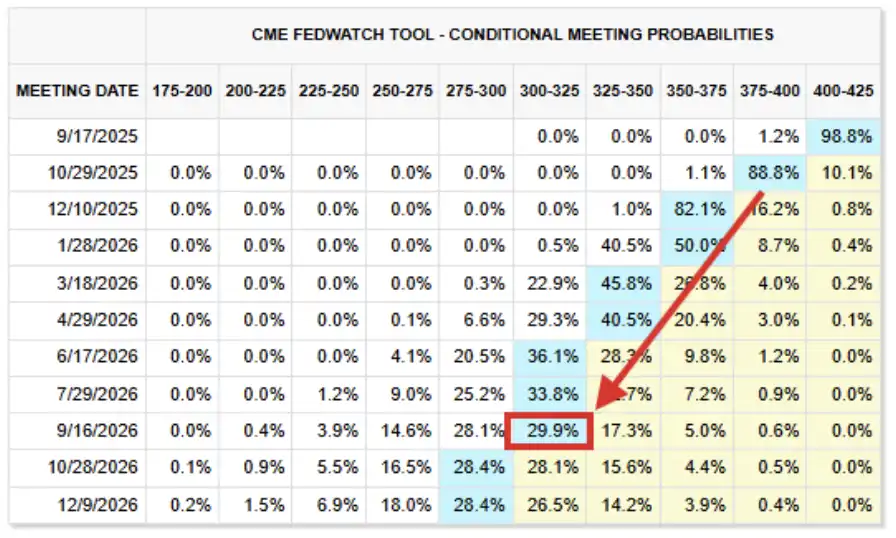

As shown below, the market's "baseline scenario" at that time was that by 2026, the Federal Reserve's federal fund rate would fall to a range of 2.75% to 3.00%. There was even over a 25% probability that rates would further decline to lower levels.

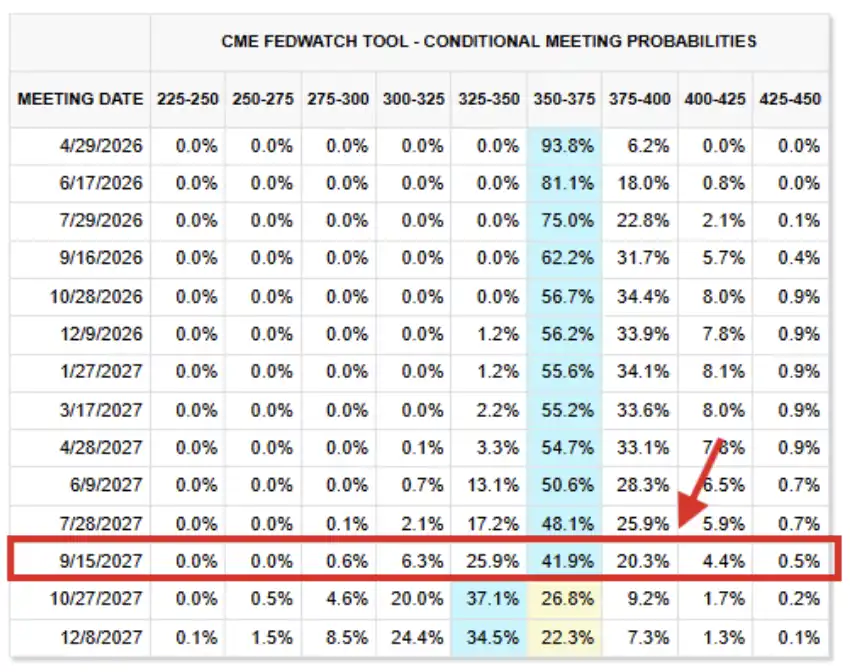

Looking at the current rate futures pricing, the present "baseline scenario" indicates that until September 2027, rates will essentially remain unchanged at their current levels, with the Federal Reserve's federal fund rate expected to be in the target range of 3.50% to 3.75%.

This level is 75 to 100 basis points higher than expected a few months ago, and this assessment has now been extended to the end of 2027.

In fact, the market has begun to discuss the possibility of "rate hikes" again: currently, about 43% probability believes that the Fed will raise rates before the end of 2026. Objectively, the market would find it very difficult to withstand such an impact.

Next, let's explain the reasons for this.

Labor Market Will Only Get Worse

On September 17, 2025, as widely expected by the market, the Fed implemented a rate cut and hinted at two more cuts before the year's end. At that time, despite inflation still being significantly above the Fed's long-term 2.00% target, market concerns about the U.S. labor market were intensifying.

In its post-meeting statement, the Federal Open Market Committee described economic activity as "having slowed" and added that "job growth has slowed," while noting that inflation "has risen and remains at a relatively high level." The weakening employment and rising inflation actually deviated from the Fed's dual goals of "price stability" and "full employment," but at that time, the labor market issues were more prominent.

Today, the condition of the labor market has only worsened. Compared to September 2025, the current market's ability to withstand higher rates is actually weaker.

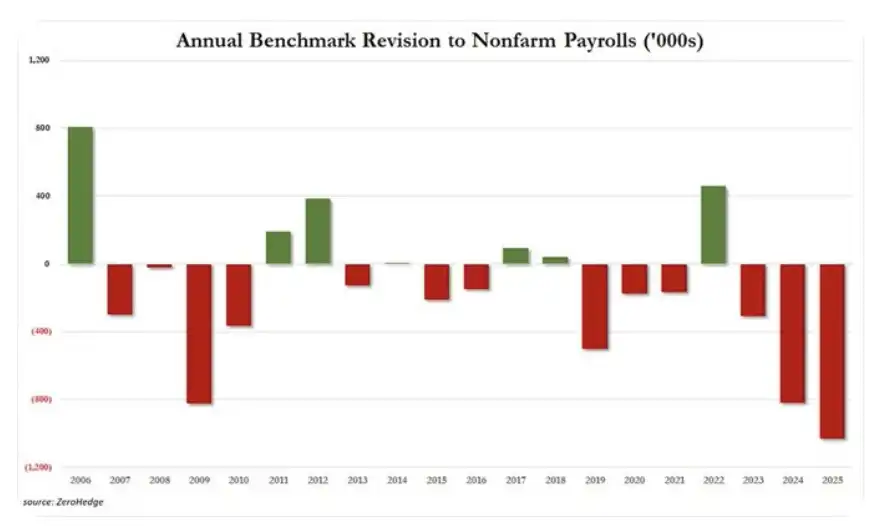

The reality is: first, the U.S.'s 2025 employment data was significantly revised downward by 1.029 million jobs, marking the largest annual downward revision in at least 20 years. Previously, the employment data for 2024 and 2023 were also revised downward by 818,000 and 306,000, respectively.

Over the past three years, a total of 2.153 million jobs have been "revised away" from the originally reported data. Since 2019, the total number of jobs revised away has reached 2.5 million, and over the past 7 years, there have been negative revisions in employment data for 6 years.

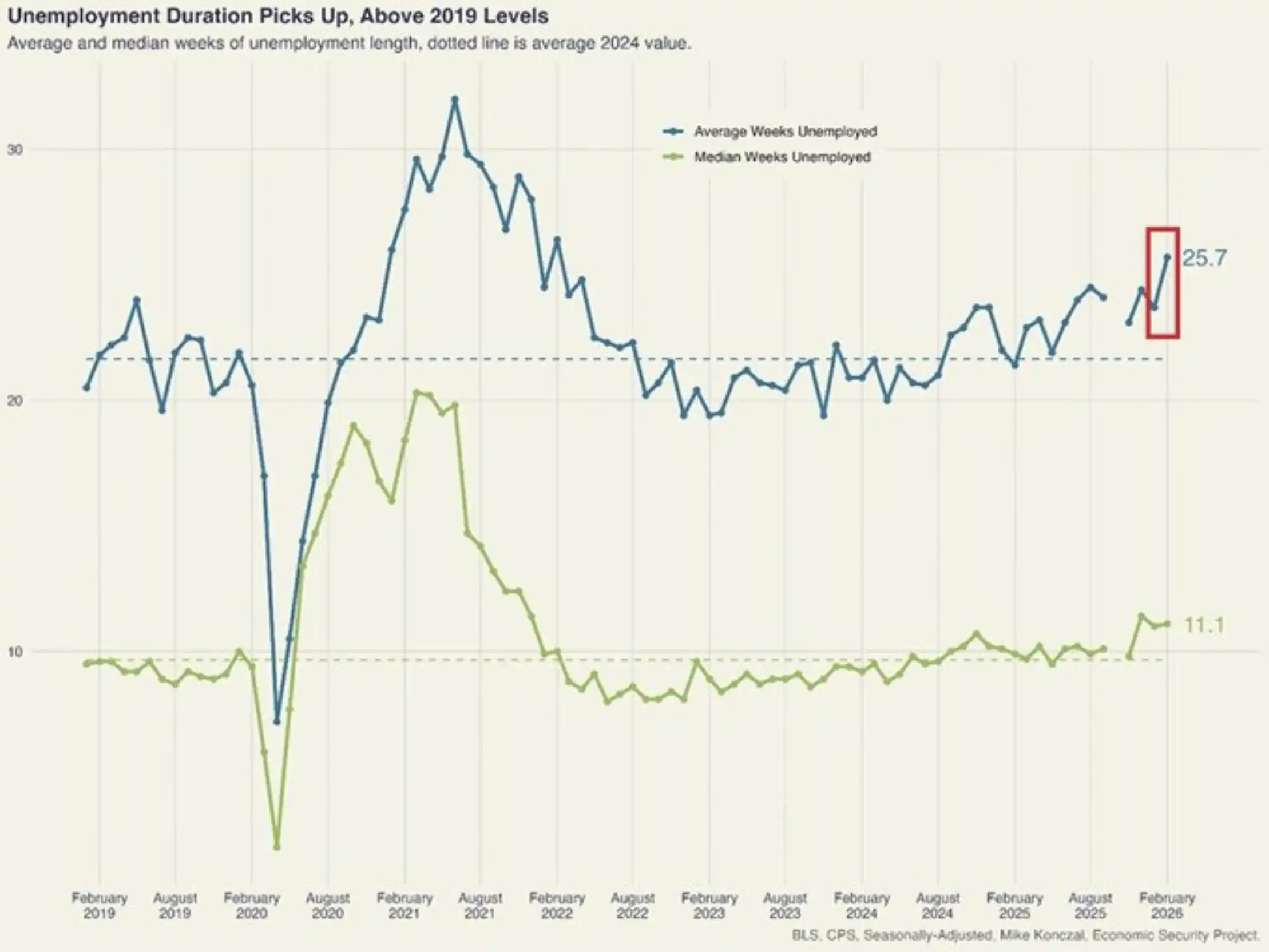

Another example is that similar situations actually exist in many cases. The average duration of unemployment in the U.S. increased by 2 weeks in February, reaching 25.7 weeks, hitting a 4-year high. Since October 2023, the duration of unemployment has cumulatively increased by 6.3 weeks, with the fastest pace since 2020 to 2021. This level is now significantly higher than the pre-pandemic levels of 2018 to 2019.

Once again underscoring, such signs are not isolated, we are witnessing a sustained and deepening weakness in the labor market.

In our view, the US economy would struggle to cope with the 10-year Treasury yield nearing 4.50%, let alone rising above 5.00%.

Why is All This Happening?

From a macro perspective, the surge in the US Treasury yields and the reversal of rate cut expectations can be attributed to a core variable: inflation.

The Fed's "dual mandate," established by the US Congress in 1977, requires the central bank to achieve two main objectives through monetary policy: maximum employment and price stability. As mentioned earlier, when the Fed resumed rate cuts in 2025, the Federal Open Market Committee (FOMC) viewed the weakness in the labor market as "more important" than the still elevated inflation.

However, with rising energy prices, ongoing Iran conflict, and the post-war energy recovery cycle being continuously extended, inflation has once again become the primary concern—not because the labor market has improved, but because inflation itself has become more severe.

As shown above, the US's 12-month inflation expectation has surged to 5.2%, reaching its highest level since March 2023. It is worth noting that the reversal of this expectation began in early January and rapidly accelerated following President Trump's threats against Iran, the military buildup in the Middle East, and the strike on Iran on February 28th.

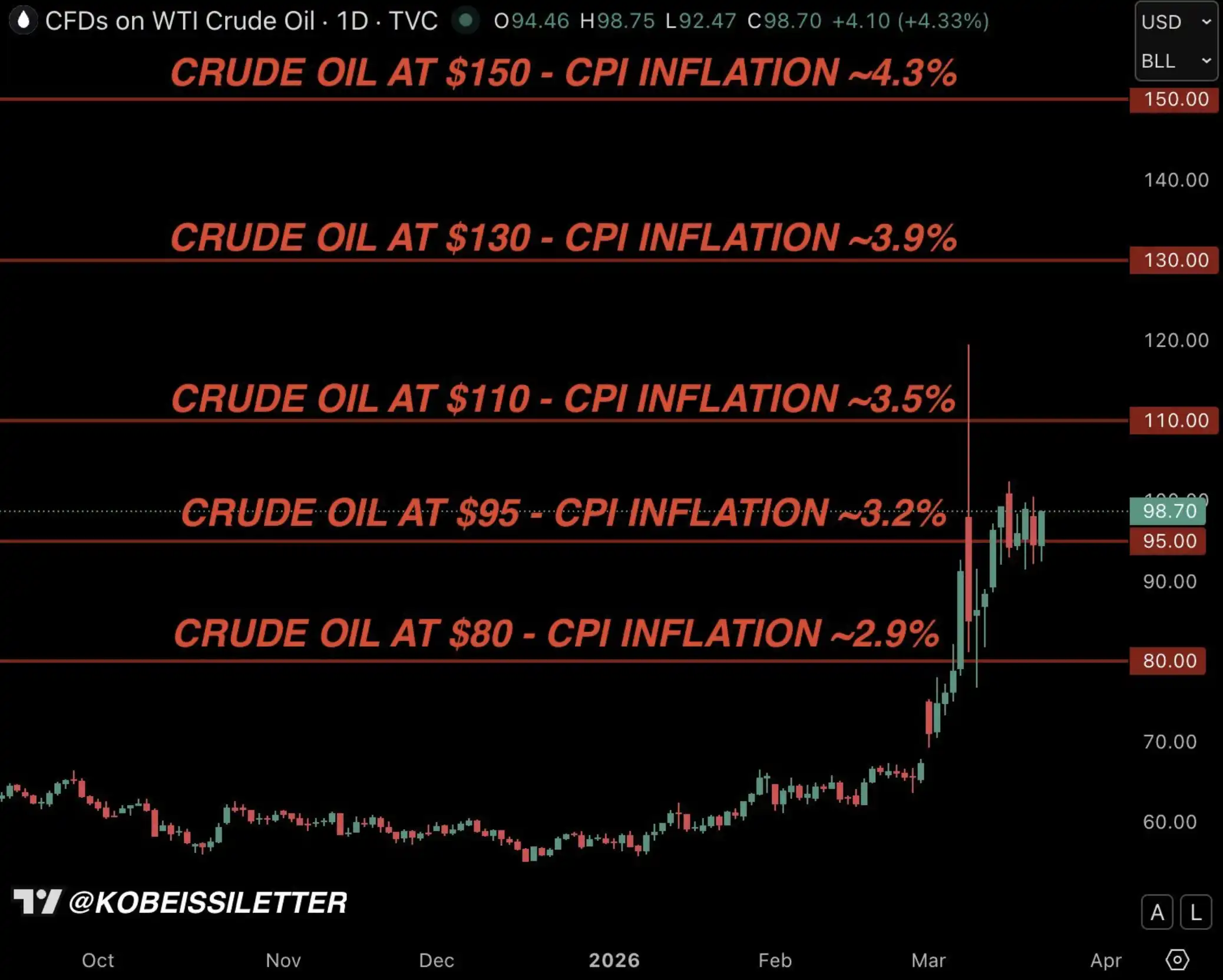

This brings us back to the CPI inflation chart based on model calculations below. As we have repeatedly emphasized since the outbreak of the war, if oil prices average $95 per barrel over a three-month period, US CPI inflation will rise to 3.2%.

However, given the current chain of transmission effects, the extent of inflation's upward trajectory is likely to be more than 3.2%.

We Believe "Intervention" is Imminent

During the intense market volatility sparked by the early 2025 trade war, there was a key factor that ultimately led President Trump to announce a 90-day tariff suspension in April 2025—that factor was the bond market.

In the following chart, we have outlined the complete timeline of the U.S. Treasury Bond yield increase during the so-called "Liberation Day," which ultimately led to a policy shift on April 9, easing market pressures.

During an on-site interview on April 10, Trump also clearly stated that he was closely monitoring the bond market's movements.

It can be seen that the U.S. 10-year Treasury bond yield in the 4.50% to 4.70% range is likely to constitute what we refer to as the Trump "Policy Shift Zone." This level is slightly above the current position, and we also largely agree: once the yield reaches this range, policy intervention will become necessary to prevent a severe downturn in the U.S. economy.

In our view, this time will be no exception. In fact, we believe that President Trump's announcement of "peace talks" on March 23 was not a coincidence, as outlined below.

At 4:30 AM ET on March 23, we pointed out that compared to the energy market, the bond market's issues had become more "disordered." Subsequently, within just 2 hours, the 10-year U.S. bond yield rose to 4.45%, and President Trump likely had a decision discussion similar to that of April 9, 2025, when he announced a 90-day tariff truce.

One hour later, Trump announced a 5-day delay in the strike on Iranian power facilities and stated that a "productive" dialogue between the U.S. and Iran had begun to end the war.

This may well be the first signal of intervention beginning.

What Should You Do Now?

The most common question we receive is: What does this mean?

From a macro perspective, we want to emphasize one point: the Trump administration is highly sensitive to stock, commodity, and bond market fluctuations. This is good news for investors—Trump does not want market declines, and his level of concern in this regard is significantly higher than that of previous administrations.

This is also why, after an initial surge, oil prices have remained somewhat under control. Crude oil investors widely believe that once oil prices approach $120 per barrel again (as seen in the early stages of the war), Trump will promptly take intervention measures.

More broadly, we believe that as the 10-year U.S. Treasury yield rises, downward pressure on the stock market will intensify; however, when the yield approaches the 4.50% to 4.70% range we mentioned, an imminent policy shift or "intervention" will limit the downside potential of the stock market.

Furthermore, Trump, the Fed, and the entire government are well aware that the U.S. labor market cannot sustain higher rates in the long run, which also means that the current situation is unlikely to evolve into a "long war" and is more likely to see some degree of easing or resolution in weeks rather than months.

Finally, behind these fluctuations and noises, we want to emphasize: the AI revolution is only accelerating. Those AI companies that have led the market since 2022 and are now under pressure due to a pullback are actually investing more and building faster.

Our assessment of the stock market and the long-term trend of AI remains unchanged.

Continue to Watch the Bond Market Closely

What we are experiencing is not just volatility but a shift in "decisive variables."

Over the past few weeks, the market's focus has been on oil prices, war news, and geopolitical escalation. But beneath the surface, a more potent force is gathering strength and beginning to dominate the situation.

The bond market is redefining the direction of stocks, commodities, and even policies. And history has repeatedly shown that when financial conditions tighten too quickly, the question of intervention is never "if it will happen" but "when it will happen."

As we have emphasized throughout this year, this market is increasingly resembling a game of "pattern recognition," where the key is to act a step ahead of the "crowd."

We believe the bond market will be the next most critical narrative.