Nine months ago, on July 31, 2025, Michael Saylor referred to MicroStrategy's newly listed STRC preferred stock as the company's 'iPhone moment' during the Q2 earnings call, emphasizing the ability to 'significantly expand holdings without selling a single bitcoin.' However, by the Q1 2026 earnings call in May of this year, Saylor himself mentioned incorporating 'selling some bitcoin to pay dividends' into the operating model.

After market close on May 5, MicroStrategy released its Q1 2026 earnings, reporting a net loss of $12.54 billion. At the end of the quarter, the company held 818,334 bitcoins with an average acquisition cost of $75,537 per bitcoin. Saylor stated during the earnings call that the company might sell some bitcoin to pay dividends, stating, "We might sell some bitcoin to pay dividends, to desensitize the market and send a signal that we have indeed done so."

CEO Phong Le was more direct in his explanation, describing the purpose of selling bitcoin as 'strengthening the balance sheet' or 'increasing the per-share BTC content.' This framing positions selling bitcoin as a normalized operational tool rather than a crisis measure. After the news was announced, MSTR's stock price fell over 4% in after-hours trading.

Thus far in 2026, the company has continued to accumulate bitcoin, with just the STRC preferred stock alone contributing approximately 77,000 bitcoins to the BTC position, without any selling of bitcoin to date. In essence, this is a statement about the possibility of selling bitcoin in the future, not an announcement that such sales have already taken place.

Pressure Focused on STRC

STRC is a perpetual preferred stock introduced by MicroStrategy in July 2025, with no expiration date, an annualized dividend of 11.5%, and monthly payouts. As of the Q1 2026 earnings, the circulating supply of STRC is approximately $8.5 billion.

The design goal of STRC is to make itself 'like a savings account.' The monthly dividend rate is not fixed but dynamically adjusted based on market demand. When STRC falls below its $100 face value on the secondary market, the company raises the dividend rate to attract investors back. When STRC surpasses face value and corrects, the rate is lowered to suppress demand. This mechanism has worked quite well, with STRC's 30-day historical volatility standing at only 1.7%, much lower than gold (36%) and the S&P 500 (20%).

The buyers of STRC are not native crypto capital but fixed income investors seeking stable high-yield returns. It is compared not to BTC spot but high-yield bonds. Those purchasing it are looking for the 11.5% monthly cash flow, not BTC price appreciation.

Why can this preferred stock become the centerpiece of MicroStrategy's entire annual obligation? Let's take a look at the structure.

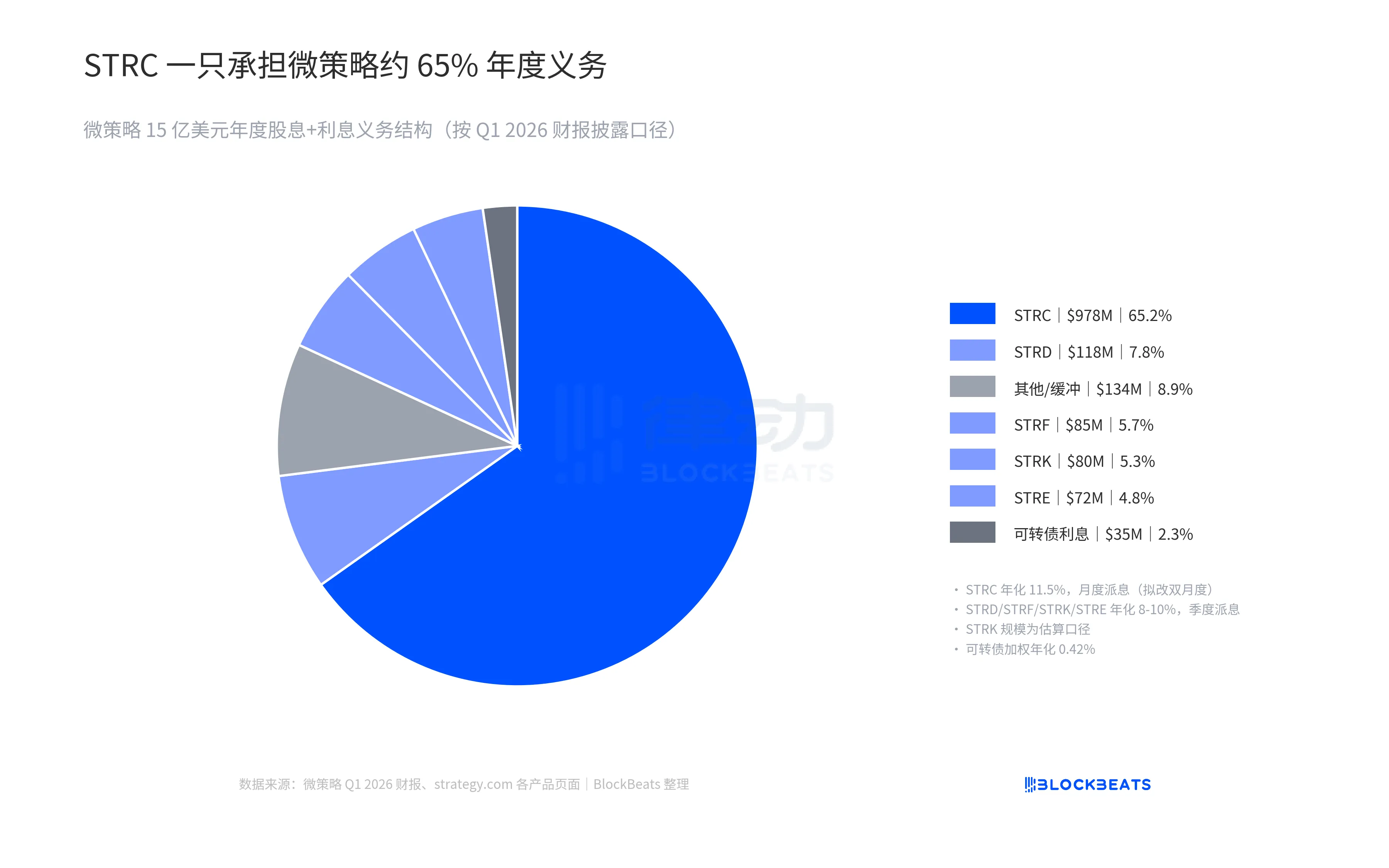

Based on the Q1 2026 financial report disclosure, MicroStrategy's total annualized dividend + interest obligation is approximately $1.5 billion. STRC alone bears about $978 million, accounting for approximately 65% of the entire system. The remaining four preferred stocks, STRD, STRF, STRK, STRE, amount to approximately $360 million, with an 8.2 billion convertible bond weighted annual interest rate of only 0.42%, corresponding to an annual interest of only $34.6 million.

The entire MicroStrategy interest payment system relies on the STRC preferred stock to bear about two-thirds of the pressure. This directly explains why on April 17, the first preferred stock to have its dividend schedule adjusted was STRC, not the other preferred stocks.

STRC's operation does not rely on operating cash flow but rather on a three-legged cycle. Saylor described it at the earnings call as "buy bitcoin with credit, let it appreciate, sell a portion to pay interest." New investors buy STRC, and the raised funds are divided into two parts: one part buys bitcoin (increasing the holdings), and the other part goes into a USD reserve (thickening the buffer). The USD reserve pays dividends monthly. The remaining bitcoin position continues to appreciate in the secondary market.

As long as the annualized appreciation rate of bitcoin reaches the 2.3% threshold, the USD value growth of the BTC position per year will be greater than or equal to the $1.5 billion total annual obligation. In this scenario, the entire cycle is self-sustaining, and the company does not need to net sell a bitcoin.

However, if any of the three legs are broken, whether the STRC ATM cannot sell, the USD reserve is exhausted, or BTC is in a prolonged stagnation, this cycle will trigger the backstop. The so-called "backstop" means selling a portion of the MicroStrategy's 820,000 BTC position directly to cover the dividend.

On May 5, Saylor's statement essentially did not say, "We are now going down this backstop path," but rather brought this originally deeply buried option to the forefront, allowing the market to price it in advance.

From IPO to Sell-off Declaration

On July 21, 2025, STRC went public, raising $2.521 billion in its IPO, with an initial monthly dividend rate of 9%. By December 1, MicroStrategy quietly established a $1.44 billion USD reserve. According to the announcement, these funds are used to support preferred stock dividends and unpaid debt interest payments, with an initial coverage period of about 21 months and a long-term target of 24 months or more. The establishment of the USD reserve itself was an indirect signal: MicroStrategy has begun to make a cash buffer for the scenario of "what if STRC issuance stalls."

On March 1st of this year, the STRC monthly dividend rate was increased from 9% to 11.5%. This increase itself was a signal. The fluctuating dividend rate mechanism of STRC has triggered a situation where the secondary market demands a higher yield to accept STRC, forcing the company to raise the price to attract buyers.

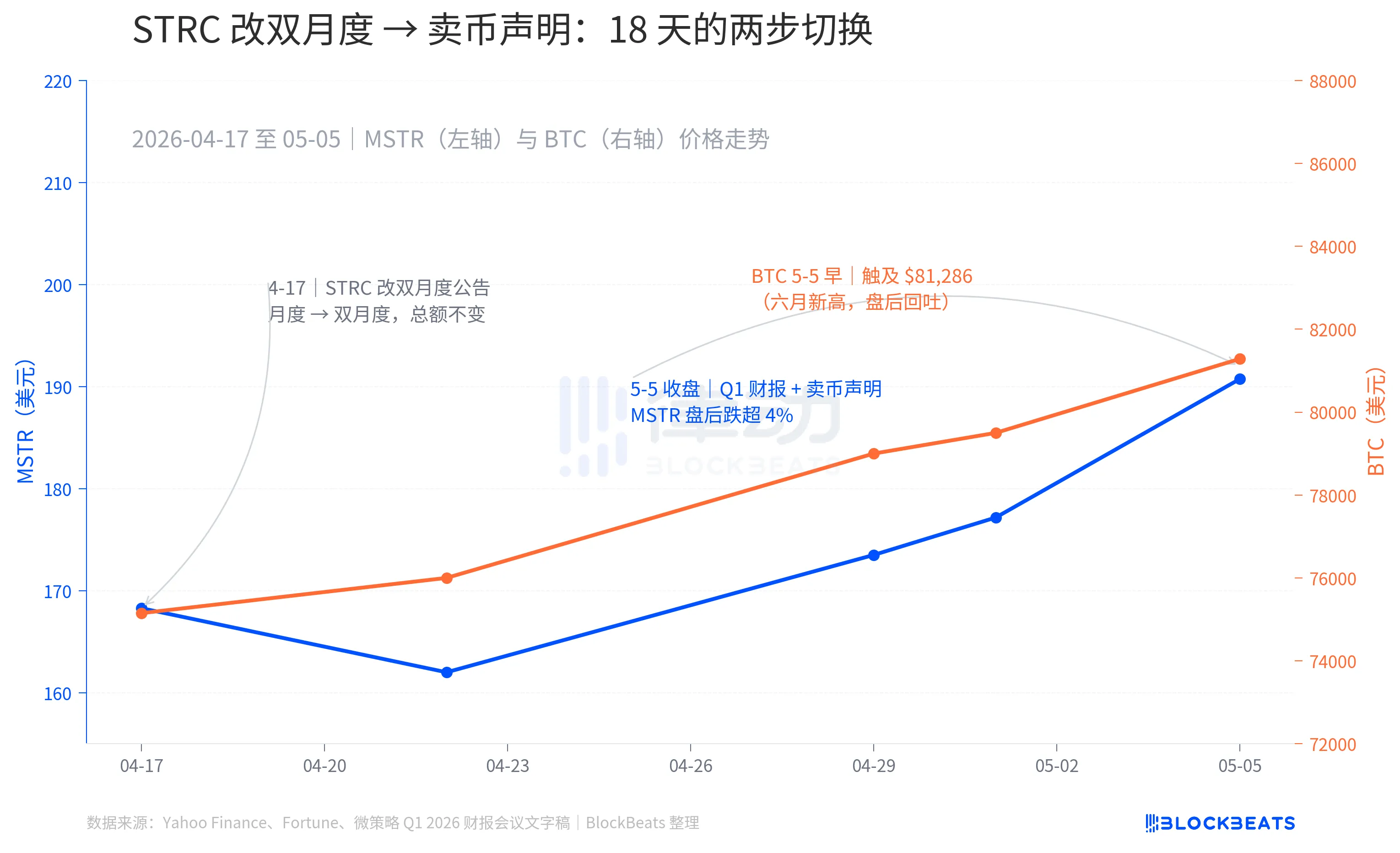

On April 17th, STRC announced a switch to a bimonthly schedule. While maintaining the 11.5% annualized rate and total amount, the monthly dividend distribution was changed to a semi-monthly frequency. The official reason was to "reduce ex-dividend day sell-offs, decrease volatility, and bring STRC closer to a $100 face value." By May 5th, the "put option" was officially announced.

When arranging the above nine-month-long chain by timeline and then viewing the chart, it becomes more visually clear to see the two-step switch in the final 18 days. On April 17th, there was a change in pace, and on May 5th, the coin selling was acknowledged. During these 18 days, MSTR rose from $168.28 to $186.90 at the close on May 5th, and Bitcoin rose from around $75,150 to $81,286, reaching a high not seen since January of this year. From a price perspective, the market did not interpret the "pace adjustment" as a pressure signal. However, on the evening of the financial report, MSTR dropped more than 4% in after-hours trading, and Bitcoin also retraced some of its gains. The anticipated repricing due to the coin selling announcement was immediate.

When piecing together the nine-month timeline, the true meaning of Saylor's "desensitization to the market" becomes clear.

He was not forced to sell the coins, nor was he breaking a commitment. CEO Phong Le described the purpose of selling Bitcoin as "strengthening the balance sheet" and "increasing the per-share BTC content," both of which fall under the category of routine financial management for a publicly traded company. The former corresponds to actions commonly seen in the open market such as "selling assets to optimize cash on the balance sheet," while the latter is a standard KPI that the BTC treasury company tracks on a quarterly basis.

MicroStrategy used this "operational management" language to characterize the sale of Bitcoin, rather than language at the "forced" or "emergency" level, indicating that the nature of this action has been redefined from "bottoming out in a crisis" to a "routine operational tool." The key change is that the bottoming out has shifted from "implicit" to "explicit."

Under what circumstances would coin selling be triggered?

MicroStrategy needs to pay approximately $125 million in dividends + interest per month (totaling $1.5 billion in annual obligations). This money is not normally used to cash out by selling Bitcoin but rather through a two-legged strategy.

The first leg is funding raised from new STRC issuances. When investors buy STRC, some of the money goes directly into MicroStrategy's operating account, enough to cover the monthly dividends. This is the norm. The second leg is the $2.25 billion USD reserve. The purpose of the reserve is to reduce the likelihood of selling Bitcoin. When the pace of STRC issuance slows down and monthly fundraising falls below monthly obligations, the difference is supplemented from the reserve.

With the current $2.25 billion reserve divided by a $125 million monthly obligation, there is coverage for approximately 18 months. This is the origin of the "18-month coverage capacity" mentioned by the management in the financial report.

However, the reserve is not unlimited. If the Senior Secured Term Loan Facility (STLF) remains unsold for a long time and starts to be discounted at a high interest rate of 11.5% in the secondary market, the reserve will continue to deplete. Before the reserve hits rock bottom, MicroStrategy must either increase the STLF dividend yield to attract investors back (at the cost of heavier obligations) or resort to the last resort. This last resort is selling Bitcoin to cover the dividend.

Therefore, the complete trigger chain for "selling Bitcoin" is: the STLF issuance is blocked, the USD reserve is depleted, and Bitcoin must be sold to meet obligations before the reserve runs out.

So, if it does come to that point, how much should be sold? Assuming the STLF remains unsold, the USD reserve is depleted, and the BTC price remains unchanged, how much of the existing 818,334 BTC position does MicroStrategy need to sell to cover the $1.5 billion dividend + interest for the year?

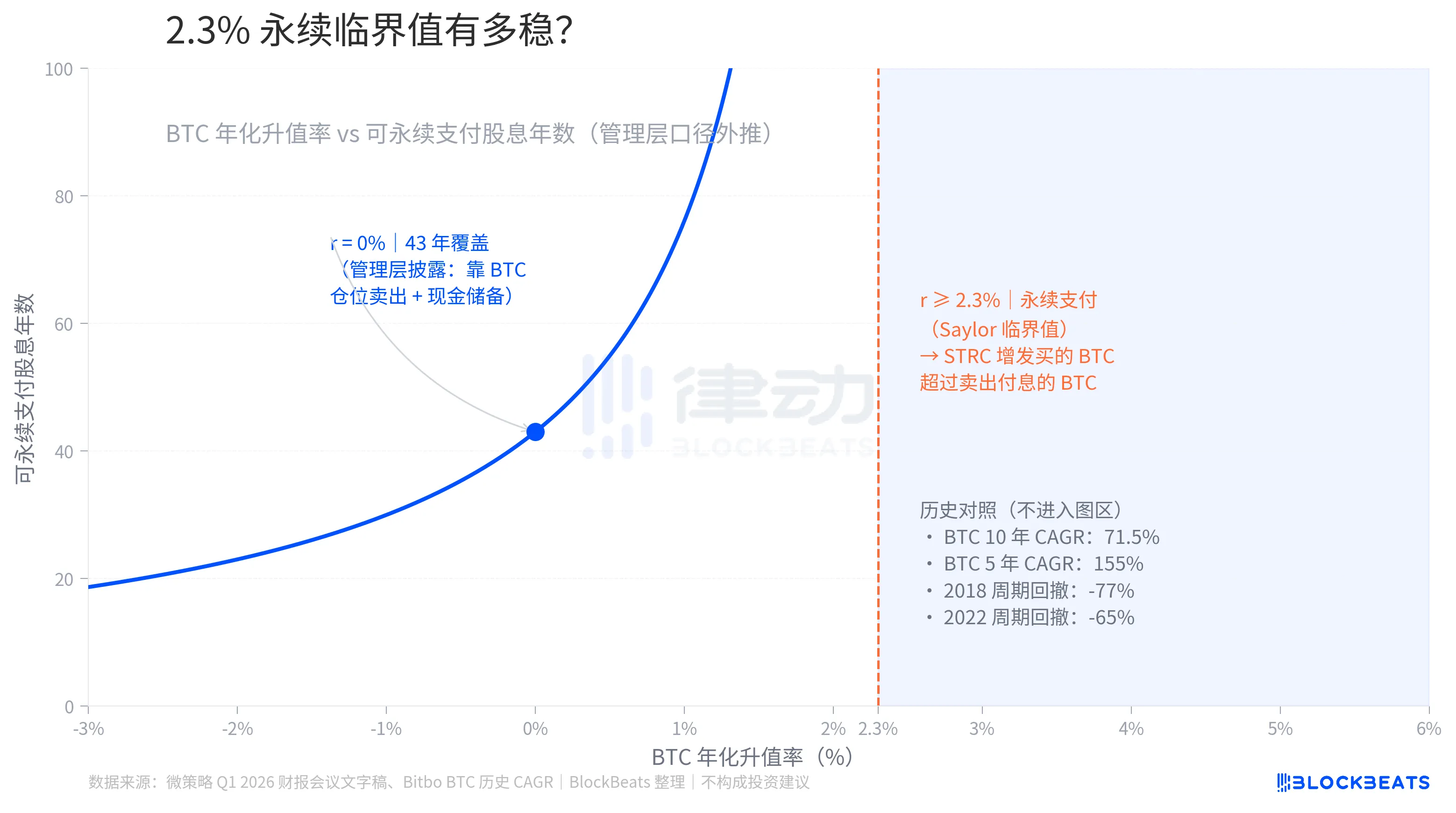

The logic is straightforward. The annual USD amount to be paid, divided by the current USD price per BTC, gives the number of BTC to be sold in a year. Based on a $1.5 billion annual obligation and the current BTC price of $81,000, it is approximately 18,519 BTC, equivalent to 2.3% of the total position.

If Bitcoin falls back to around the average purchase price of $75,537, the annual selling amount rises to nearly 19,857 BTC, just enough to offset nearly 26% of MicroStrategy's 77,000 BTC accumulated through STLF since 2026.

Based on the current price of $81,000, without considering BTC appreciation, the exhaustion of the position will take 44 years. This is the source of the management's statement of "BTC holding for 43 years if BTC does not appreciate."

In the context of Bitcoin's history, 2.3% seems less restrictive. Over the past 5 years, BTC has had a compound annual growth rate of about 155%, and over the past 10 years, around 71.5% (data from Bitbo). However, Bitcoin has also experienced drawdowns of -77% in the 2018 cycle and -65% in the 2022 cycle. The existence of the USD reserve is to cushion against these drawdowns, covering obligations for approximately 18 months as stated by the management.

Based on the current pace, if BTC continues to stagnate and new STLF issuances are blocked, the $2.25 billion cash wall will hit bottom within 18 months.

“We might sell some Bitcoin” becoming news is not about the sale itself, but about a three-year reiterated commitment being rewritten as a single embedded option.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia