On June 4, Eastern Time, the U.S. tech stocks experienced severe turbulence due to Broadcom's earnings guidance, causing the AI valuation narrative to show its first crack.

Broadcom's FY2Q performance itself was not bad, with revenue of $22.2 billion and EPS of $2.44 beating expectations, and its AI semiconductor business growing 143% year-on-year. However, its guidance for the current quarter failed to meet the market's already elevated expectations. CEO Hock Tan also revealed during the earnings call that the main custom chip customer, Google, may diversify its supply chain, and he mentioned that the expansion of the chip business would drag down the gross margin. This combination pierced through the core narrative that has supported AI trading for the past few months, leading to a drastic rotation of funds on that day.

The Dow Jones Industrial Average surged 1.7% in a single day driven by traditional sectors, hitting a new historical high; however, the Nasdaq Composite Index fell by 0.09%, and the Nasdaq 100 fell by 0.5%. In this "dumbbell-shaped" market differentiation, leading AI and semiconductor stocks faced comprehensive selling pressure: Broadcom -12.59%, Micron -7%, Marvell fell by 7% in pre-market trading, and AMD fell by over 4% in pre-market trading.

Amidst this widespread decline, AAOI showed an independent trend contrary to the sector sentiment.

Broadcom's Guidance Shatters Expectations, First AI Sector Valuation Plunge

This time, Broadcom became the catalyst that crushed AI trading, not because its performance was poor, but because its guidance did not meet the market's inflated expectations.

During the earnings conference, Hock Tan disclosed that AI chip sales for the fiscal year (ending in October) would reach $56 billion. Although this number is substantial, it is below market expectations. Coupled with its statement about Google diversifying the supply chain, the market's valuation premium for Broadcom, supported by ASIC business over the past year, was shaken. In intraday trading, Broadcom hit a low of $403, with a market capitalization evaporating by about $300 billion throughout the day, marking its largest single-day drop since January 2025.

The selling pressure then spread throughout the entire AI computing power chain. The storage sector also experienced a synchronized sell-off, with Micron being considered a core supplier of AI accelerator HBM and deeply linked to AI capital expenditure sentiment, falling by about 7% in a single day. Storage-related stocks such as SanDisk and Western Digital also weakened simultaneously. Although CrowdStrike's Q2 revenue guidance was not bad on its own, it was sold off indiscriminately against the backdrop of the overall cooling of AI trading.

Bridgewater Associates founder Ray Dalio joined the camp warning about AI valuation today, clearly distinguishing between "buying AI stocks" and "investing in AI technology," cautioning that current valuations "may be becoming excessive." This echoes recent warnings about AI capital spending and high valuations from JPMorgan Chase CEO Jamie Dimon and Apollo CEO Marc Rowan.

The rotation of funds also carries signaling significance, flowing into the traditional economy stocks represented by the Dow Jones Index rather than a mass exodus from risk assets. This implies that the market is not engaging in systemic hedging but rather undergoing structural deleveraging within the AI sector.

AAOI Standalone Market: Surges Over 10% in a Single Day, Hits Intraday Short-Term High

In this environment, AAOI surged by 11.76% in a single day, rising from around $171 to $209.64 intraday, closing at $202.89, sharply contrasting with price declines in stocks like Broadcom and Micron.

AAOI has previously experienced multiple rounds of intense volatility. The stock hit a historical high of $233.67 on May 13, dropped 9% in a single day on May 29, rebounded by 17.18%-18.81% on June 1, and surged by 11.76% again on June 4. In the past 30 days alone, there have been over four trading days with a daily price swing of over 10%. This volatility has become a norm in AAOI's current valuation structure, with trading volume on May 11 reaching 214% of the three-month average.

The mid-term catalysts driving AAOI's strength are relatively clear. On May 8, Rosenblatt (the day after the company announced Q1 earnings) raised AAOI's target price from $140 to $220 in one go, reiterating a "buy" rating and listing it as a "top pick." At the same time, Raymond James raised its target price from $72.50 to $160, and B. Riley raised its target price to $129 but maintained a neutral stance. Rosenblatt's core logic includes Amazon's 800G optical module revenue contribution starting, the potential kickoff of a second revenue line with Oracle's qualification, and a significant uptick in demand for the company's products ranging from 100G/400G/800G to the emerging 1.6T generation.

The supporting fundamental data of the company is also specific. AAOI has publicly disclosed cumulative orders for 800G and 1.6T optical modules exceeding $324 million; in April 2026, it received a $20.9 million grant from the Texas Semiconductor Innovation Fund to expand its factory in Sugar Land, Texas, to 210,000 square feet; and announced the addition of 388,000 square feet of capacity in Pearland, aiming to achieve a monthly capacity of 700,000 units of 800G and 1.6T optical modules by 2027. Management guidance targets optical module business revenue to reach a $1.4 billion annualized level by Q3 2027.

However, AAOI's fundamentals are not without flaws. Its Q1 2026 performance fell short of expectations, with a GAAP net loss of $14.3 million and revenue of $151.1 million, both slightly below market consensus. The adjusted EPS guidance for Q2 is between -$0.03 and +$0.03, hovering around breakeven. B. Riley, while maintaining a Neutral rating, pointed out that AAOI's 800G mass production will be delayed to the second half of the year, presenting execution risk due to overreliance on customer forecasts. Additionally, AAOI executives collectively sold about $12.6 million worth of stock in mid-May, although the remaining holdings are still substantial, the timing of the sales coincided with a peak in the stock price.

In summary, AAOI is currently in a state of tension characterized by a "strong narrative, weak Q1 earnings, and significant valuation premium," which is the fundamental reason for its ability to experience high daily stock price volatility.

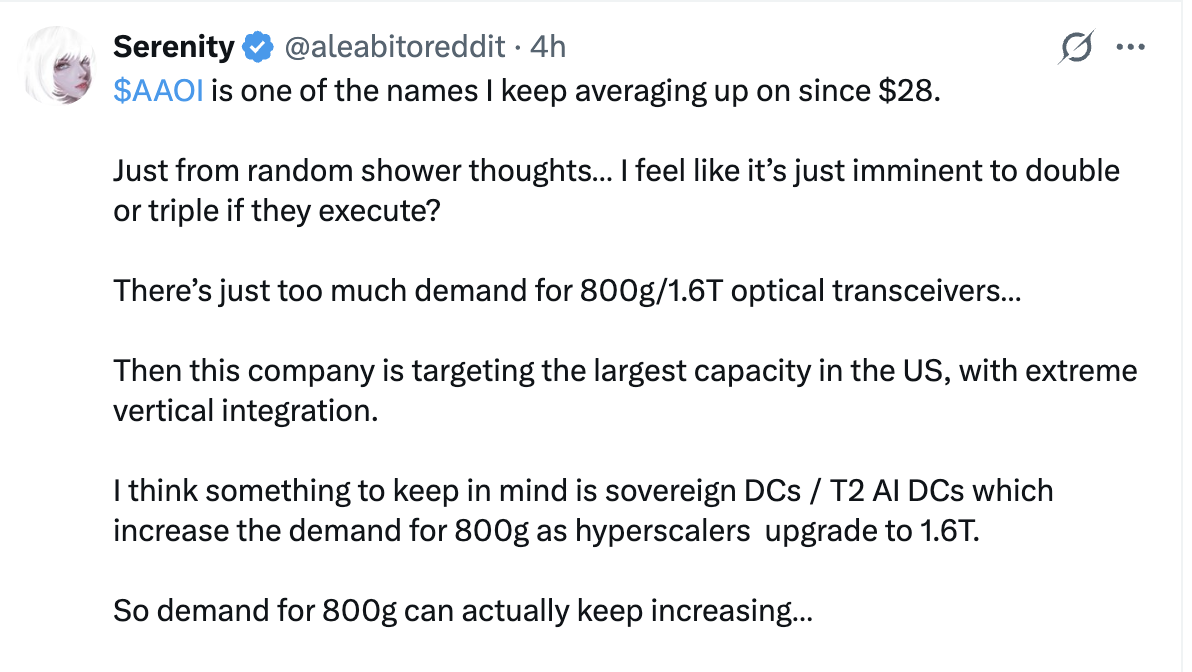

It is worth mentioning that AAOI also has a potential additional driver, known in the Chinese community as "Stock God," Serenity has repeatedly posted expressing optimism about AAOI, believing it to be his favorite optical communication exposure in the U.S. stock market. He started accumulating shares at $28 and it could possibly be the "next Micron."

The Logic Behind the Counter-trend Strength: "Pricing Divergence" within the AI Sector

AAOI's counter-trend strength on June 4 should not be interpreted as a counterexample to AI valuation concerns, but rather as an early signal that the market is beginning to engage in "pricing divergence" within the AI sector.

One of Serenity's public assessments in April was that the resilience of optical communication-related assets may surpass that of large-cap tech stocks: "Even if the S&P 500 drops another 20%, optical communication companies may still outperform." This logic is rooted in the scarcity of the supply chain, where InP substrates, laser sources, and 800G optical module capacity are all structurally tight in the medium term, with pricing power lying on the supply side rather than the demand side.

The sell-off triggered by Broadcom's guidance is fundamentally a correction of the narrative surrounding "custom ASICs + customer concentration" rather than a revision of the overall demand for AI infrastructure. From this perspective, optical communication assets, strongly linked to downstream computing power deployment, do not directly overlap with Broadcom's core issues (customer concentration, Google potentially diversifying its supply chain) at the narrative level.

However, risks are also present. AAOI's current stock price reflects extremely high execution expectations, with the market assuming it will achieve $1.4 billion in annualized optical module revenue by Q3 2027 while maintaining high gross margins. Should the pace of 800G production in Q2 and Q3 fail to validate, or if there is any fluctuation in customer concentration risk (Amazon, Microsoft), the valuation structure could undergo significant volatility. Although Q1 actual earnings were weak, this crack is currently masked by the narrative of order growth and production expansion, but it has not been completely eliminated.

For observers of the Chinese market, the counter-trend rally of AAOI in this instance is noteworthy not so much for the magnitude of the price increase, but for the direction of internal market fund differentiation. When the AI meta-narrative first showed signs of cracking, the fact that funds were willing to buy AAOI at the same time Broadcom was plummeting suggests a certain judgment – that Broadcom's issues are not synonymous with a broader AI capex problem, and that optical communication is still recognized as a "physical bottleneck" narrative. Whether this judgment is accurate will ultimately depend on the actual financial reports over the next few quarters.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia