In the past, a market holiday in traditional finance usually meant a pause in price discovery. Assets such as stocks, commodities, ETFs, etc., would enter a silent period after the Friday close, and investors had to wait until the next trading day to see the true impact of events reflected in prices.

However, the on-chain derivatives market led by Hyperliquid is changing this structure.

With Hyperliquid HIP-3 allowing external builders to deploy stocks, commodities, index, and other Real World Asset (RWA) perpetual contracts, part of the traditional assets represented by the XYZ market can now be traded 24/7 on-chain. During a traditional market holiday, the on-chain market does not stop matching orders. Instead, it may become a frontline for risk expression and price discovery.

Just this past weekend, the on-chain movement of South Korean chipmaker SK Hynix provided a clear observation sample. Hyperliquid xyz:SKHX did not only experience sporadic trading during the KRX holiday. According to the candleSnapshot 1m K-line data, bulls and bears engaged in significant chip exchanges over the weekend.

By the time the KRX officially opened on Monday, June 8, the on-chain market had already provided a complete weekend price path.

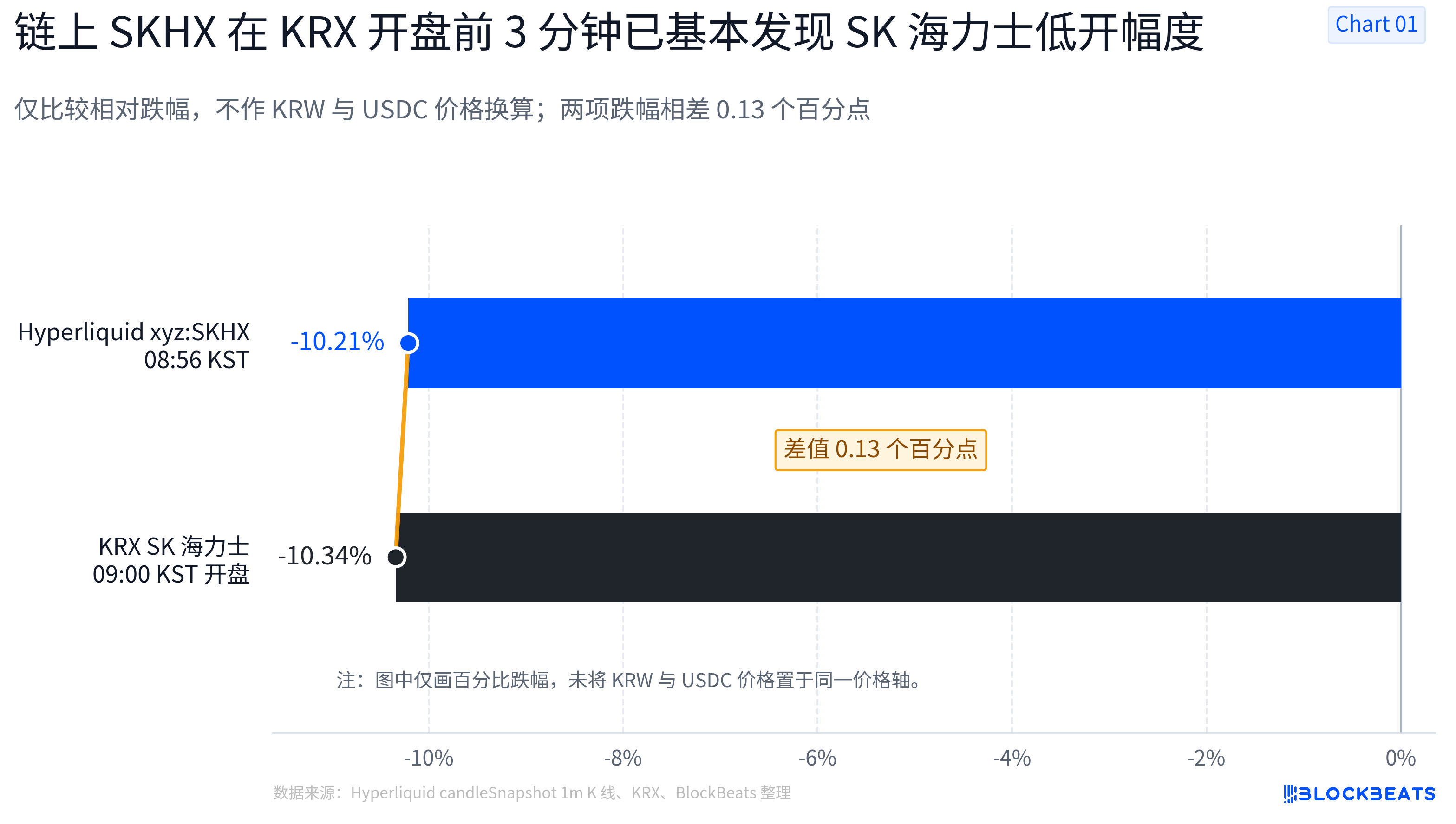

0.13% Precision: SK Hynix's Weekend Price Discovery

On June 5, the closing price of SK Hynix on the KRX was 2,070,000 KRW. Subsequently, the Korean stock market went into the weekend holiday.

According to Hyperliquid's 1-minute K-line data, after the Friday close, its reference price remained at 1336.5 USDC. In the early hours of Monday before the KRX opened, there was a significant on-chain price fluctuation:

· Monday 08:56 KST (Korean Standard Time): xyz:SKHX dropped to a low of 1200.0 USDC, corresponding to a -10.21% decrease.

Three minutes later, in the traditional world, the KRX officially opened, and the actual data was:

· Monday KRX Official Open: 1,856,000 KRW, corresponding to a -10.34% decrease.

The difference between the two was only 0.13 percentage points.

This means that three minutes before the KRX officially opened, the on-chain market had almost entirely discovered the extent of Hynix's Monday opening decline. It did not vaguely indicate the direction of "it will drop," but precisely priced the decline to around 10%, highly consistent with the actual opening result.

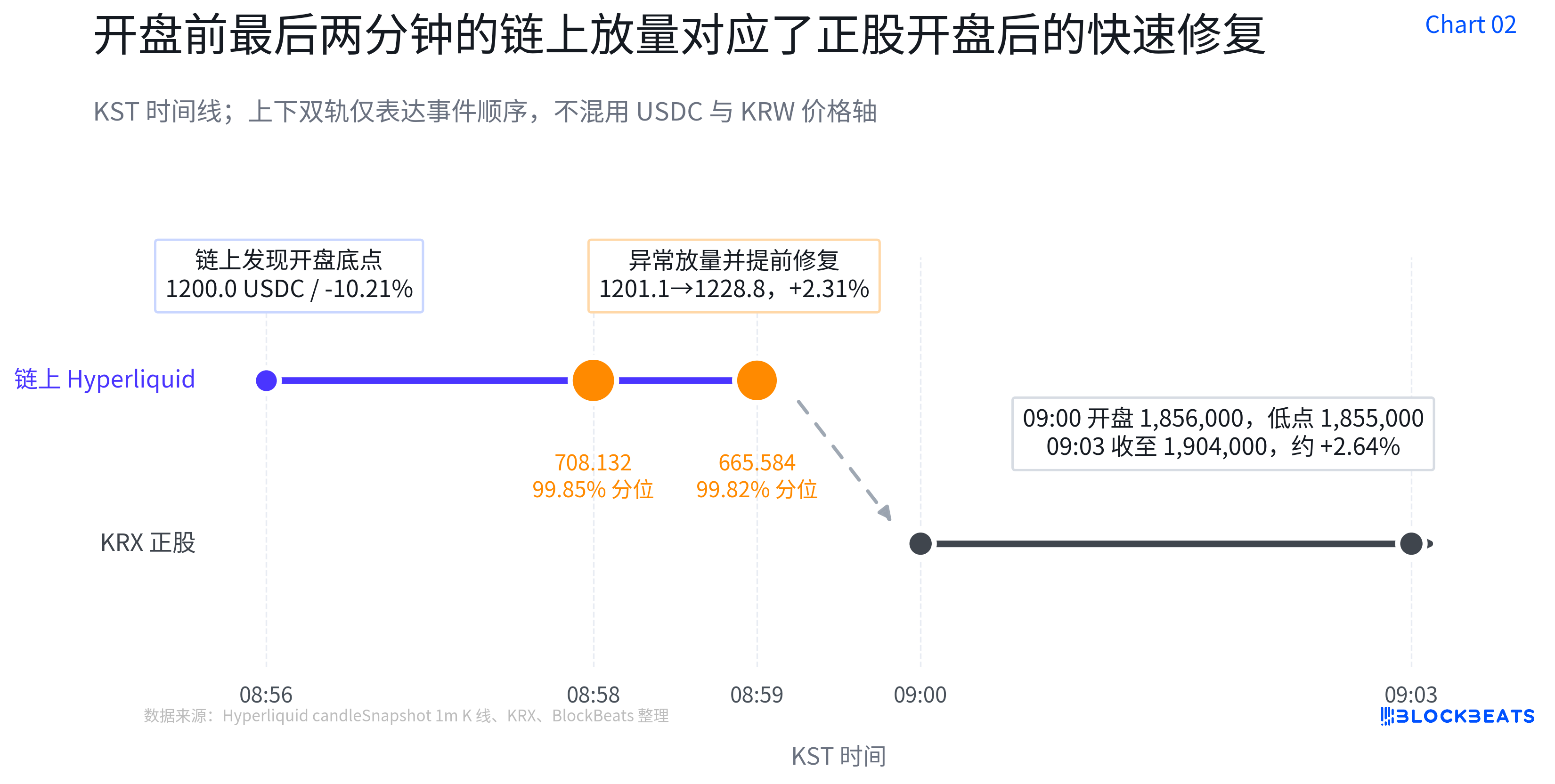

Key Reversal: Not a Prediction Failure, But Early Trading Trend Post Market Open

Subsequently, the market saw a second-stage shift, mainly focused on the final 120 seconds before the market open.

During the 08:58 - 08:59 KST period, xyz:SKHX experienced abnormal volume surge:

· 08:58: Minute volume spiked to 708.132, at the 99.85th percentile of the entire weekend's minute volume;

· 08:59: Volume remained at 665.584 (99.82nd percentile), price surged from 1201.1 USDC to 1228.8 USDC, witnessing a +2.31% rebound within two minutes.

If we only look at the final price at 08:59, the on-chain price was about 2 percentage points higher than the subsequent actual KRX opening price. However, this does not imply an on-chain price discovery failure. A more reasonable explanation is that the on-chain market had already traded the post-market open low-end support in advance.

Now observing the actual trend post KRX opening:

· KRX opened with a low of 1,855,000 KRW;

· 09:03 KST: The stock price had already risen to 1,904,000 KRW, marking a rebound of around +2.64%.

BlockBeats Note: Superficially, there is a 2% difference between the on-chain closing drop (-8.06%) and the stock's opening drop (-10.34%); however, when the timeline is broken down, the conclusion is entirely different. The on-chain market had completed the discovery of the "opening bottom" at 08:56 (with only a 0.13% deviation), and by 08:58, it had already transitioned to trading the "post-opening repair trend" (with highly synchronized rebound magnitude and pace).

On-chain market price discovery is not a static single-point prediction; it demonstrates a continuous, dynamic pathfinding capability.

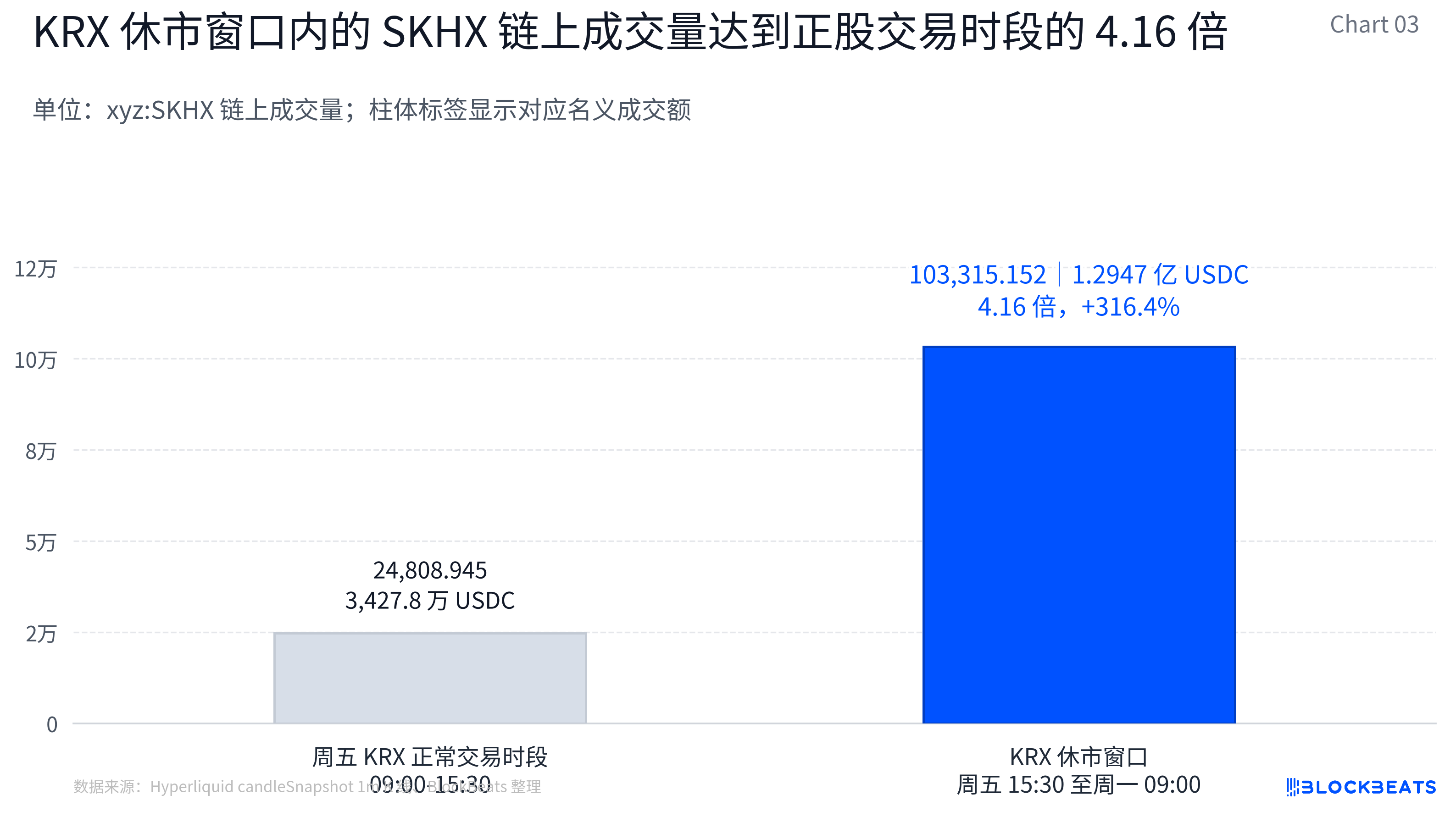

Data Retrospective: On-chain Trading Volume 4 Times Higher Than Regular Stock Hours

Examining specific transaction data, the Toshiba on-chain perpetual contract showed a significant contrast in performance between the regular trading hours in the Korean stock market and the weekend market closure window.

During Friday's regular trading hours in the Korean stock market (09:00-15:30 KST), the traded number of contracts for this Toshiba on-chain perpetual was 24,808.945, which, based on minute transaction prices, corresponds to approximately $34.278 million USDC in trading volume.

During the market closure window from the Friday closing of the Korean stock market to the Monday opening (15:30-09:00 KST), the perpetual contract accumulated a trading volume of 103,315.152 contracts, equivalent to approximately $129.47 million USDC.

In other words, during the time when Samsung Electronics shares were unable to trade over the weekend, the on-chain perpetual contract’s trading volume reached 4.16 times the on-chain trading volume during a normal trading day in the Korean stock market on Friday, representing a 316.4% increase.

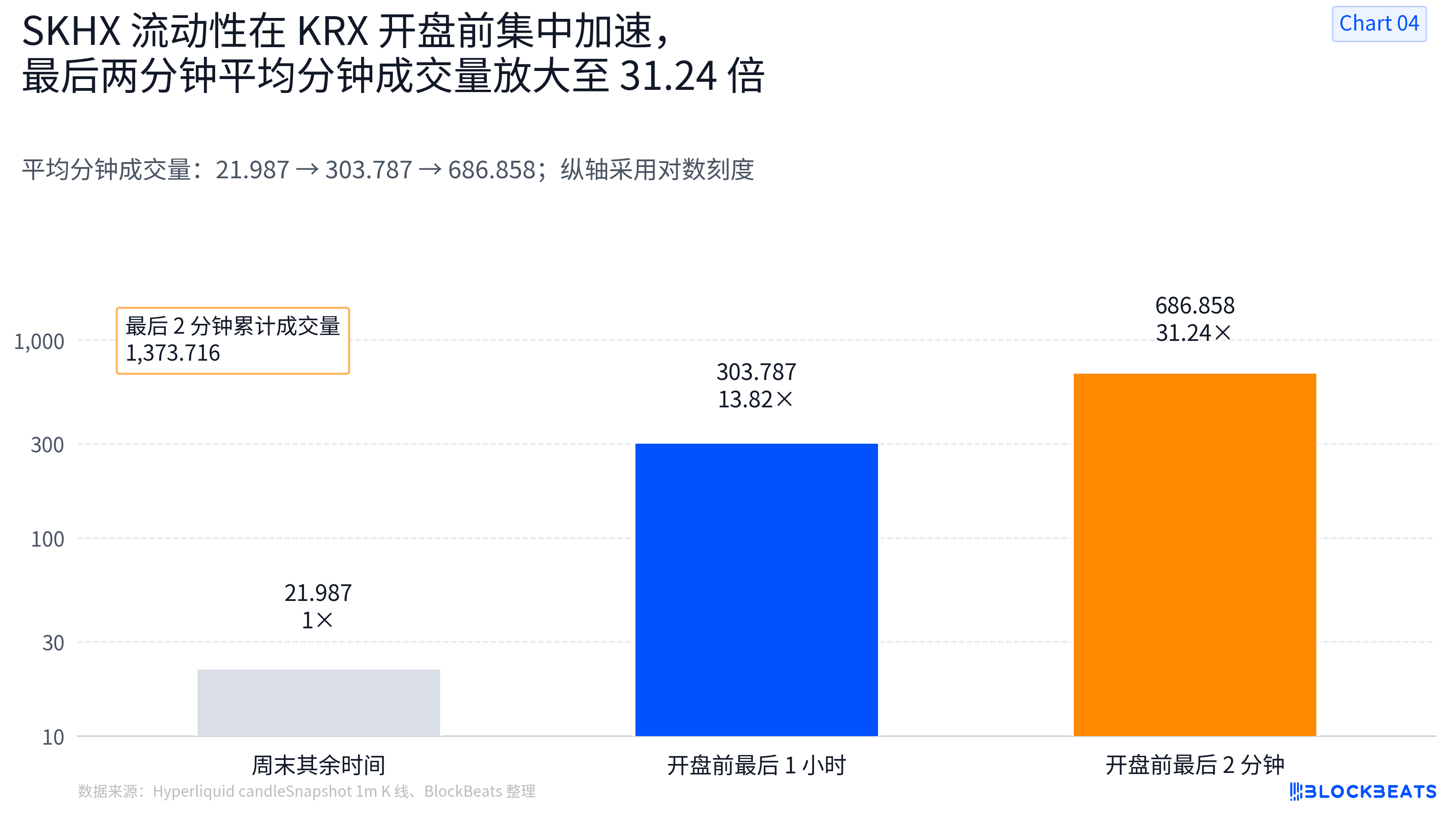

A more significant liquidity event occurred on the eve of Monday’s opening:

· Last 1 hour before opening: During weekends excluding the last hour, the average on-chain perpetual contract traded approximately 21.987 contracts per minute; however, in the last hour before Monday’s opening, the average trading volume surged to 303.787 contracts per minute, 13.82 times higher than the former, marking a 1281.7% increase.

· Last 2 minutes before opening: Between 08:58-09:00 KST, a total of 1,373.716 contracts were traded in two minutes, averaging about 686.858 contracts per minute. Compared to the average minute trading volume during the rest of the weekend, this represented a 31.24x increase, approximately 3024% higher.

This set of data indicates that price discovery does not only occur in a single moment at the opening of traditional markets. In the on-chain market before opening, the trading volume has significantly amplified, and the price discovery has occurred earlier.

Why is On-Chain TradFi Becoming Stronger?

Firstly, the market has a continuous need for expressing expectations during market closures.

Historically, when the KRX exchange closes, stock prices stop moving, and market participants have to wait for the next trading day to digest information. However, the volatility of the U.S. semiconductor sector, macro liquidity changes, and the evolving sentiment in the AI industry are ongoing. The on-chain perpetual market provides a continuous trading window, allowing traders to express their price expectations during traditional market closures.

Of more significance, on-chain pricing has surpassed mere emotional reactions.

In emotional trading scenarios, prices usually roughly reflect the direction of risk. However, the lowest price of xyz:SKHX in the first three minutes before the KRX opening had only a 0.13 percentage point difference from the actual Monday opening price. This level of precision indicates that participants in on-chain trading may include high-net-worth individuals or quantitative strategies, and their pricing models are precise enough to give the on-chain price actual reference value.

Furthermore, the pre-market trading volume reveals market participants' early processing of complex information.

The trading volume significantly spikes in the final hour, especially the last two minutes, indicating that some traders or quantitative strategies are preemptively digesting the price reaction post-market open. They are not passively waiting for the KRX to open but are conducting early hedging and arbitrage on-chain against possible opening volatility.

In conclusion, the power of on-chain TradFi is gradually emerging. It not only provides a continuous trading channel when traditional markets are closed but also begins to take on some price discovery functions. Its accuracy and information processing capabilities are gradually approaching traditional market benchmarks.

Limitations and Future Opportunities

Undeniably, the current on-chain TradFi still has significant limitations.

Firstly, there is an extremely uneven distribution of liquidity. The massive volume in the last two minutes indicates that funds only explosively concentrate at critical moments, and the order book may still be thin during normal times, making it susceptible to price distortion by a few funds. Secondly, the coverage of underlyings is limited. Currently, only popular high-weighted stocks such as Hyundai, Samsung, and US tech giants have this level of accuracy, while long-tail assets in on-chain perpetuals often lack liquidity. Additionally, due to the lack of tick-by-tick data and more detailed Taker/Maker depth data, the complete picture of the game between active buyers and sellers at that time cannot be fully reconstructed.

But its future opportunities are also clear.

As more professional liquidity providers (LPs) and cross-market arbitrageurs enter the HIP-3 market, on-chain minute-level trading volume may become more stable. With more stocks, ETFs, commodities, and indices onboarded, the on-chain market may gradually form a cross-asset, cross-timezone, uninterrupted price discovery network.

The weekend market is no longer silent. When the traditional financial world closes on Friday, the market has already completed the first round of pricing on-chain and started trading the next trend after the open. On-chain perpetual swaps are becoming an indispensable "front-running oracle" in the global asset pricing system.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia