TL;DR

· NVIDIA plans to issue at least $200 billion in bonds, but it is not strapped for cash: its recent quarterly free cash flow was around $48.6 billion.

· The key is its AA credit rating, allowing it to access long-term low-cost debt to pre-fund AI infrastructure, supply chain, and ecosystem investments.

· Related Tags: NVDA, GOOGL, META, AMZN, AI Data Centers, Power, Optical Communications, Long-Term Investment Grade Bonds.

NVIDIA's bond issuance this time could easily be misunderstood as a simple question: with so much cash on hand, why borrow?

According to the company's most recent quarter's data, as of FY2027 Q1 ending April 26, 2026, NVIDIA's revenue reached $81.6 billion, with a free cash flow of around $48.6 billion. At the same time, the company added an $80 billion share repurchase authorization and raised the quarterly dividend from $0.01 to $0.25. In other words, this is not a company in dire need of cash, relying on the bond market for survival.

However, precisely because of this, the market is particularly sensitive to its plan to issue at least $200 billion in senior notes. The bond maturities range from 2 to 30 years, with funds allocated for general corporate purposes, refinancing, AI data centers and infrastructure, R&D, supply chain prepayments, and strategic investments. For investors, the real question worth asking is not "Does NVIDIA have money?" but rather: as AI's biggest cash cow also starts systematically using long-term debt, is the AI capital expenditure narrative entering a new phase?

The crux of the matter is not that NVIDIA suddenly needs money, but that it is transforming its cash flow and credit rating into another form of expansion capability.

The Stronger the Cash, the Qualification for Long Money

When ordinary investors see "issuing debt," their first reaction is often that the company is short of cash. However, for mature large companies, borrowing money is often not a cry for help but an active choice of a cheaper and less shareholder-dilutive financing method.

What NVIDIA plans to issue is senior notes (company IOUs), essentially borrowing money from bond investors, paying interest periodically, and repaying the principal at maturity. The biggest difference from issuing new shares is: issuing debt does not divide the company's ownership. As long as the future returns generated by the company exceed the debt cost, existing shareholders can still retain more of the profits.

This is precisely the contrast of this transaction. NVIDIA's recent quarterly free cash flow was around $48.6 billion, significantly higher than the proposed financing scale. The company is also aggressively engaging in buybacks and dividend increases, indicating that issuing debt cannot simply be understood as "cash is insufficient."

A more reasonable explanation is that NVIDIA, when its credit was strongest and the market was most willing to lend to it, locked in a long-term funding ahead of time. For a company in the midst of an AI infrastructure expansion cycle, projects such as data centers, supply chain prepayments, ecosystem investments, and R&D are not short-term. Their payoff period may span multiple years, even over a decade. Matching long-term assets with 30-year debt is closer to mature capital management than relying entirely on short-term operating cash flow.

This is also the plain-language meaning of "capital structure optimization": a company not only uses cash on hand but also moderately combines low-cost debt. As long as the money borrowed generates long-term returns higher than the interest cost, debt is not just a burden but may also be a tool to improve capital efficiency.

AA Rating Turns Bonds into AI Ammunition

NVIDIA can do this on the condition that the bond market is willing to lend to it at a low enough cost. And the most important variable behind this is the credit rating.

S&P Global Ratings recently upgraded NVIDIA's rating to AA, citing reasons such as the competitive advantage brought by AI demand, strong cash flow generation ability, and a robust balance sheet. An AA rating can be understood as a high credit label in the bond market: investors believe that the company has very low default risk and are therefore willing to accept lower spreads and longer terms.

This point is crucial. Issuing bonds is not just about "raising money"; what truly determines the transaction value is "at what cost, for how long, and in what market window." When a company is in a phase of credit upgrade, rapid cash flow expansion, and continued institutional funding interest in the AI theme, its bargaining power to borrow long-term funds will be significantly enhanced.

This also explains why NVIDIA is acting at this time. It is not waiting until cash flow weakens and expansion pressure increases to raise funds, but rather, when the market most recognizes its credit quality, it is lowering the future financing uncertainty ahead of time. For shareholders, this is more attractive than being forced to raise funds in a worse environment in the future.

Several directions in the use of bond funds are also worth considering together: refinancing, AI data centers and infrastructure, R&D, supply chain prepayments, and strategic investments. Refinancing leans towards financial management, while infrastructure and supply chain lean towards expansion assurance, and strategic investments lean towards ecosystem layout. They all point to one fact: NVIDIA's capital needs are no longer just about "producing more chips" but about maintaining its position in the entire AI ecosystem.

NVIDIA sells the most essential computing power tool in the AI era, but it also needs to ensure that customers, supply chain, infrastructure, and ecosystem partners can keep up. The more critical this role becomes, the more its capital allocation looks like that of a platform company rather than just a hardware company.

Debt Financing Aligns Better with Shareholder Interests Than Stock Issuance

For NVDA shareholders, this bond issuance has another direct implication: the company is not only maintaining shareholder returns but also reserving ammunition for long-term expansion.

In the most recent quarter, NVIDIA not only had strong cash flow but also added an $80 billion repurchase authorization and increased its dividend. Repurchases and dividends mean the company is returning cash directly to shareholders, while issuing debt means the company is using external long-term funds to support future investments. Looking at both together, it's not a matter of "either/or"; the company is trying to simultaneously maintain two tracks: rewarding existing shareholders while not slowing down AI expansion.

If NVIDIA had chosen to raise funds through stock issuance, existing shareholders would have been diluted. Even if the company continues to grow in the future, earnings per share would be diluted. In contrast, the cost of debt is more certain: interest and principal. For a company with extremely strong free cash flow and a high credit rating, this cost is easier to manage.

Of course, this doesn't mean that issuing debt is always positive. Debt increases fixed expenses and also raises market expectations for capital efficiency. NVIDIA can now have investors accept this debt because the market believes its future cash flow is sufficient to cover interest payments and believes that AI infrastructure investments will eventually translate into revenue and profit. If these two assumptions change, debt will shift from being an efficiency tool to a valuation pressure.

Therefore, this bond issuance truly changes the way investors observe NVIDIA. In the past, the market was more focused on GPU demand, gross margin, and revenue growth; now, it also needs to consider how cash flow is allocated: how much is used for buybacks and dividends, how much is used for the supply chain and infrastructure, how much is used for ecosystem investments, and how much is locked in through debt.

This will make NVIDIA's valuation anchor more complex. It is no longer just a "profit growth story" but is beginning to exhibit characteristics of a "credit asset" and a "long-term capital allocation platform."

The AI Financing Template for Large Tech Companies is Taking Shape

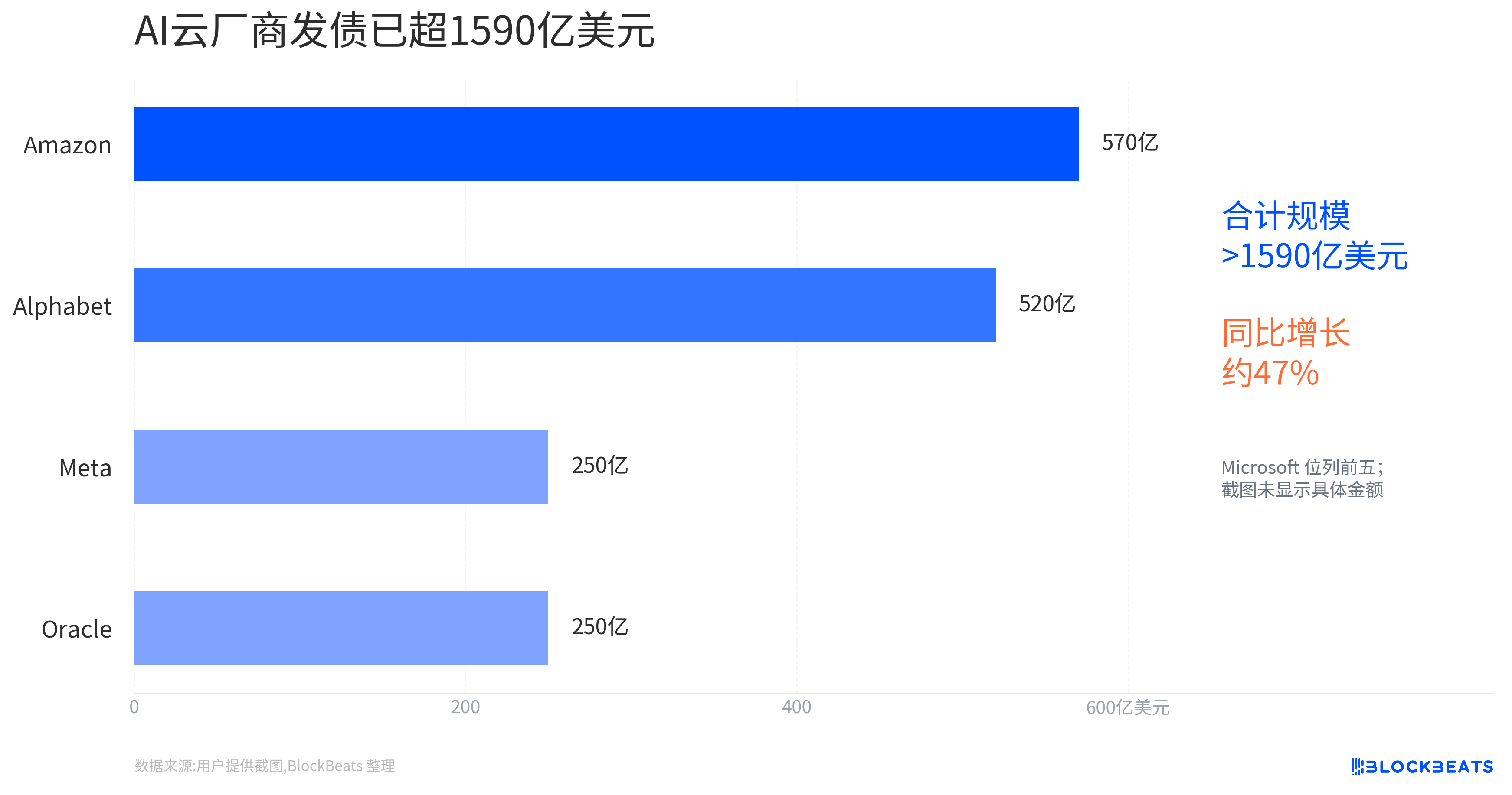

NVIDIA is not the only company taking this approach. In February 2026, Alphabet completed a $20 billion bond issuance covering multiple tranches, reportedly oversubscribed at one point to over $100 billion. Meta, Amazon, and other large tech companies are also using debt financing during the AI investment cycle as one of the tools to support infrastructure spending.

These cases cannot be simply described as "Big Tech is cash-strapped." A more accurate statement is: AI infrastructure has transformed from a light asset software growth story to a heavy asset cycle involving data centers, power, chips, networking, and supply chains. The company that can obtain funding at a lower cost over a longer period will have greater room to maneuver in this expansion.

This has two layers of impact on market pricing.

First, debt financing has extended the AI capex (capital expenditure) runway. As long as the bond market is willing to buy, large tech companies do not have to rely entirely on current cash flow to fund long-term construction. This will support expectations of demand in areas such as data centers, power, optical communication, and the semiconductor supply chain.

Second, debt financing will also make investors more concerned about the payback period. In the past, the market was willing to pay a high valuation for AI investments because the growth rate was fast enough. However, as the investment becomes heavier and the financing period lengthens, the question becomes: When will these infrastructures generate sufficient returns? If the revenue realization at the AI application end is slower than expected, or the commercial return on unit computing power declines, the market will reevaluate whether this debt-supported expansion is too aggressive.

Nvidia's uniqueness lies in being upstream in the AI capital expenditure chain. The more customers invest, the more it benefits; but if the industry's investment return is questioned, it is also difficult for Nvidia to remain completely unaffected. Therefore, this bond issuance both strengthens the market's recognition of its credit and cash flow and embeds it more deeply in the narrative of AI's long-term capital expenditure.

The key is whether pricing and returns can coexist

What needs to be kept in mind at present is: this is still "expected to issue at least $20 billion," and the final issuance size, coupon, spread, and order book strength are yet to be confirmed. Only after the transaction is completed can the market more accurately assess how low bond investors are willing to go cost-wise and for how long they are willing to fund Nvidia.

If the final pricing shows strong demand and the long-term spread remains low, this will further demonstrate that Nvidia is turning its AA credit into an expansion tool. It can not only profit from customer AI spending but also finance its long-term layout in the capital market at a lower cost.

However, the more important validation will come in the subsequent financial reports and capital expenditure data. Investors need to see whether Nvidia can continue to maintain strong free cash flow while advancing AI infrastructure, supply chain prepayments, ecosystem investments, and shareholder returns. If these variables can work in parallel, the bond issuance is an amplifier of capital efficiency.

Conversely, if in the future the ROI of AI infrastructure extends, or if a company keeps increasing its reliance on external financing to sustain its expansion, the market's perception of this type of debt will change. At that point, the question will no longer be "Does NVIDIA lack money?" but rather "Is the ROI of long-term AI investment sufficient to support today's expectations of being cashed out early with cheap funding?"

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia