TL;DR

· The Fed kept interest rates unchanged, but the dot plot indicated an increased risk of hiking rates later this year.

· Powell did not submit a personal forecast and played down traditional forward guidance, signaling the market needs to adjust to a less predictable Fed.

· Key assets to watch: BTC, Nasdaq, S&P 500, 2-year Treasury yield, DXY, Gold.

The Fed, under Powell's first FOMC meeting, maintained the federal funds target rate range at 3.50%-3.75%. However, post-meeting, US stocks dropped, bond yields rose, and risk assets did not take this "hold" stance well.

The anomaly was that while the policy rate remained unchanged, the market began repricing the future path. The Fed's combination this time was: unchanged rates, upward revision in inflation outlook, a hawkish shift in the dot plot, and new Chair Powell openly stated that the statement had removed the traditional forward guidance, deeming such guidance "inappropriate for the current policy environment."

For investors, this was not a typical "hawkish hold." If it were just a dot plot shift, the market could still engage in probability trading around the next meeting. If it were just the Chair changing communication styles, the impact might have been limited. However, this time both events coincided: the committee's collective forecast leaned towards hiking, yet the Chair himself no longer wanted to use forecasts as market guides.

Risk assets are facing more than just "will there be a rate hike this year." The bigger change is that in the past, the market was accustomed to receiving a roadmap from the Fed in advance, but now this roadmap itself is becoming blurred.

Rates Unchanged, Future Path Shifted

According to the Fed statement, this FOMC voted unanimously at 12:0 to keep rates unchanged. Looking solely at this outcome, it did not entail a direct tightening. What made the market nervous was the subsequent release of economic projections, notably the SEP, and the highly anticipated dot plot.

The dot plot can be understood as Fed officials' individual, vote-based expressions of where they see future rates. It is not a policy commitment or a formal decision, but the market uses it to gauge internal committee inclinations. If more dots shift higher, investors typically raise the probability of future rate hikes or a longer maintenance of higher rates.

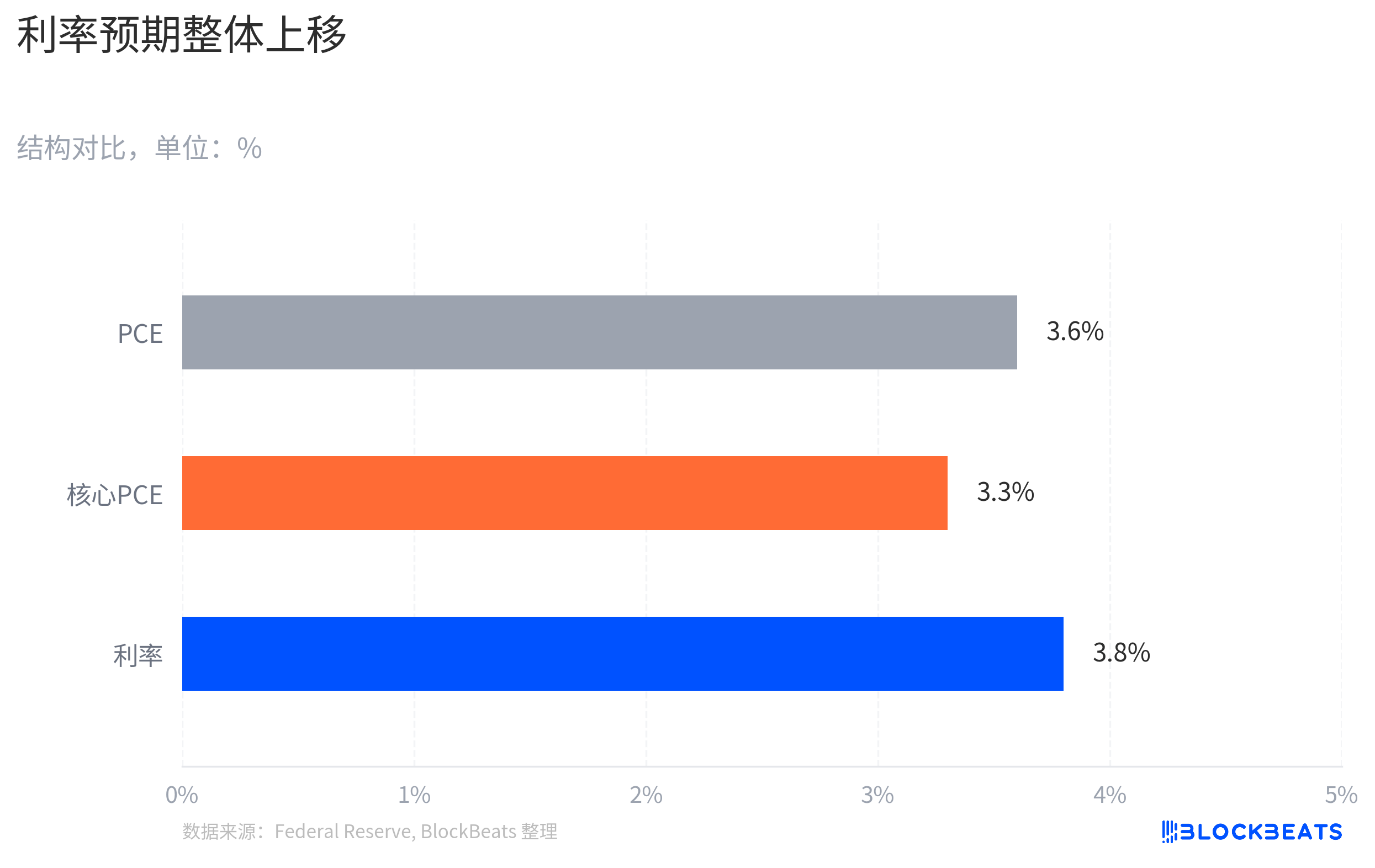

The June SEP revealed that 18 participants submitted forecasts this time. As per the dot plot ranges, 9 individuals expect at least one more rate hike within the year, 8 roughly maintain the current level, and 1 corresponds to a scenario of a rate cut. By the end of 2026, the median federal funds rate reached 3.8%, above the 3.4% from the March SEP.

This is the reason for the "no rate hike is also dovish" scenario. The market is not trading the current day's rate but the tail risk of the coming months: if inflation remains high, will the Fed put rate hikes back on the table.

Inflation expectations are also supporting this view. The June SEP raised the 2026 PCE inflation median to 3.6%, core PCE to 3.3%, up from 2.7% for both in March. PCE is the Fed's preferred inflation measure, and core PCE excludes food and energy, providing a better reflection of underlying price pressures. The upward revisions for both indicate that the Committee believes inflation is stickier than previously expected.

The implication of this meeting on the market is not "rates unchanged" but "the Fed acknowledges greater inflationary pressures and more officials are considering reintroducing rate hikes." Previously skewed funding bets need to readjust their positions.

Dot Plot Tilts Hawkish, Powell Doesn't Ink His Dots

The tension in this meeting stems from the coexistence of Powell's personal choice and the collective FOMC forecasts.

On one side, the dot plot shows a more hawkish view within the Committee on inflation and the rate path. On the other side, Powell himself did not submit his individual forecast and stated at the beginning of the press conference that the statement removed forward guidance as it is not suitable for the current policy environment. He also emphasized the need for policy to rely more on existing and real-time data sources.

Forward guidance has been a central bank communication tool that markets have been very familiar with for over a decade. Central banks use statements, forecasts, and press conference language to inform the market in advance about the likely future path of policy, aiming to stabilize expectations and reduce disorderly financial conditions. For traders, this is akin to the central bank paving the way in advance. The policy has not changed, but the path ahead is broadly visible.

What Powell's debut revealed is the opposite signal. He did not abolish the dot plot or announce a departure from the forecasting framework, but he chose not to submit individual dots and publicly played down the market's reliance on forward guidance. It is now challenging for the market to interpret a specific median, a certain phrase, or a particular chart as a fixed route.

This does not contradict the hawkish signal from the dot plot. The Committee is now more concerned about inflation, and the Chair does not want the market to treat forecasts as commitments. As a result, investors have to digest both a higher rate path and less certainty simultaneously.

Therefore, this meeting cannot simply be summed up as "Powell is more hawkish than his predecessor." A more accurate statement would be that Powell is attempting to shift the Fed's credibility from "committing in advance to future actions" to "adjusting at any time based on data." This approach preserves policy flexibility, but the cost is that the market finds it harder to anchor the path in the short term.

Less Guidance Will Amplify Data Volatility

If the Fed provides less guidance, the market will have to bear more judgment costs on its own.

In the pricing of risk assets, Fed communication itself is a form of liquidity variable. Not only rate cuts can change asset prices, but a clear easing path can also reduce volatility, encouraging funds to buy growth stocks, crypto assets, and long-duration assets in advance. Conversely, even if rates remain unchanged on a given day, as long as the future path is more uncertain, the market will demand a higher risk premium.

This is the asset implication of Powell's communication shift. In the past, investors often treated the FOMC as a "find the answer" meeting: what words were removed from the statement, where is the dot plot median, and whether the chair's press conference reassured the market. If Powell continues this style in the future, the FOMC may be more like a data calibration point than an answer release event.

In this framework, the weight of inflation, employment, wages, productivity data will all increase. Every key data point could directly alter market pricing for the next meeting because the chair will not provide too many protective explanations in advance. The so-called data dependency sounds neutral, but for trading, it means a shorter path, quicker feedback, and more direct volatility.

Powell announced the establishment of a working group involving communication, balance sheet, data sources, productivity and employment, and inflation framework, which also reinforces this signal. However, these working groups are currently more suitable for understanding as a reassessment of the policy framework. It cannot be concluded that the Fed has entered a completely new era of long-term high rates based on this, nor can it be said that the dot plot has been abolished.

Variables of BTC, Nasdaq, and Gold Trading Differ

Post-Fed meeting, different assets are under pressure, but this does not mean they are trading based on the same logic.

The commonality between Bitcoin and the Nasdaq is that they are both sensitive to real interest rates and liquidity expectations. When the market believes that future policy rates may be higher, the dollar stronger, and short-term yields rising, high-volatility assets and long-duration growth assets are usually suppressed. According to market data, Bitcoin had previously fallen back around $65,500 and briefly fell below $64,000 post-meeting, with macro pressures being a key backdrop.

However, Bitcoin's decline cannot solely be attributed to the FOMC. The crypto market is also influenced by positions, leverage, ETF flows, on-chain liquidity, and market sentiment. A more prudent statement is that the Fed's hawkish expectations and a stronger dollar have added pressure to already sensitive risk appetite.

The logic for the Nasdaq and S&P 500 is more straightforward. Growth stock valuation depends on future cash flow discounting, and a rate hike path will raise discount rates, also reducing the market's tolerance for risk asset valuations. According to AP, on June 17th, the S&P 500 fell 1.2%, the Nasdaq fell 1.3%, and U.S. bond yields climbed due to rate hike expectations.

Gold is a different asset. It does not generate cash flow and is usually sensitive to real interest rates and the direction of the US dollar. When short-term yields rise and the US dollar strengthens, the opportunity cost of holding gold increases, and the gold price is likely to come under pressure. According to market data, gold fell by around 2% intraday after the meeting, driven more by expectations of real interest rates and US dollar strength rather than a simple change in risk appetite.

On the other hand, the US dollar and short-term Treasury yields stand on the opposite side. The probability of a rate hike this year, upward revisions to inflation forecasts, and the Chair's reluctance to make a commitment to easing will all support the US dollar and short-term rates. The market is not trading on an actual rate hike; rather, it is trading on the idea that the Fed is no longer readily endorsing an easing bias.

Next Step: Observing Whether Powell's Style Continues

After this meeting, the most important thing to watch is not the median dot plot itself but whether future data will force the dot plot to continue moving up.

If the upcoming PCE and core PCE figures continue to be higher than expected and the labor market does not show a significant cooling, the tail risks of rate hikes in this dot plot will become more realistic for market participants. At that point, the market discussion will no longer be just about the "hawks staying put" but whether actual rate hikes are back on the table as a policy option.

If inflation moderates and employment weakens, Powell's emphasis on data dependence will also give the Fed room to pivot. The dot plot is not a commitment; it can be adjusted based on data. This is equally crucial for risk assets: a reduced forward guidance does not mean the Fed will necessarily sustain a prolonged period of high pressure but rather that the market must adjust its expectations more quickly in response to data.

Another variable is whether Powell's communication style will continue in the next meeting. If he continues to refrain from providing a clear path and continues to downplay traditional forward guidance, the market will have to accept a new normal: the Fed will no longer be responsible for laying out each step in advance, and volatility will remain more between data releases and meetings.

Next, what BTC, the Nasdaq, gold, and the US dollar need to watch for is not just a soothing statement but whether inflation truly comes down and whether Powell will continue to advance the "less guidance" Fed.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia