A monthly roundtable survey aimed at semiconductor investors reveals that the AI semiconductor market is still hot, but fund flows have significantly shifted. TSMC, Texas Instruments (TXN), memory, and AMD are viewed more positively, while semiconductor equipment stocks and Intel face more skepticism.

The timing of this survey is crucial. TSMC's official calendar indicates the company will hold its 2026 second-quarter earnings call on July 16. Texas Instruments announced that it will host its second-quarter earnings call on July 22 at 3:30 p.m. ET. AMD's official calendar shows the Advancing AI 2026 event scheduled for July 22 to 23, with the flagship global AI event mentioned in April's announcement livestreaming on July 23.

Short-term funds are not looking at a simple "strong AI demand" statement but rather whether companies can translate AI demand into revenue growth, capital expenditure, gross margins, customers, and orders.

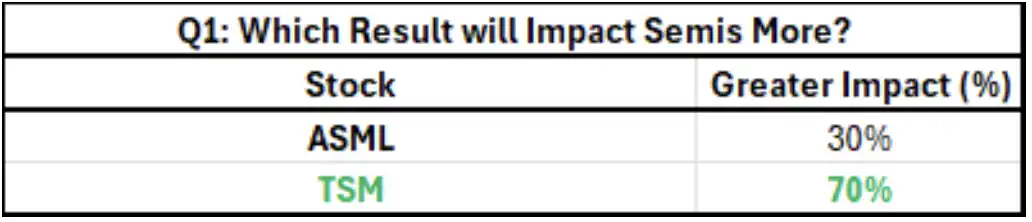

The most direct divergence in the survey is between TSMC and ASML. 70% of respondents believe that TSMC's performance has a greater impact on the semiconductor sector as a whole, while the selection of ASML is at 30%. This result shows that buyers are currently more concerned with how much AI demand will eventually translate into foundry revenue and capital expenditure, rather than just looking at lithography machine order activity.

TSMC Becomes the First Stress Test for Semiconductors This Week

TSMC is positioned ahead of ASML because it connects two things: AI revenue growth and equipment stock order expectations.

Buyer expectations from the survey suggest that TSMC may raise its 2026 sales growth guidance from the previous 30%+ to over 35%, with some respondents even betting on close to 40% year-on-year growth. The five-year compound annual growth rate for AI sales may also see an upward revision, with previous market discussions ranging in the mid-to-high 50%.

These numbers will directly impact investors' assessment of the sustainability of AI semiconductor demand. If TSMC confirms higher growth, the market will be more inclined to believe that AI server, advanced process, and advanced packaging demand are still ongoing. If the company only maintains its previous stance, it may be seen as "not strong enough" in the short term.

More sensitive is the capital expenditure. TSMC's previous 2026 capital budget was $52 billion to $56 billion. What the market wants to hear now is whether management will further provide a clearer medium-term capital expenditure framework, but this is still a buyer's expectation rather than a confirmed arrangement.

The pressure on equipment stocks also comes from here. In the past two weeks, equipment stocks have experienced a retreat, partly because investors are concerned that if TSMC does not release a strong enough signal on medium-term capital expenditure, the implied order expectations in equipment stocks may need to be adjusted downward.

ASML's issue is not lack of upside potential. After recent stock price underperformance, valuation pressure has eased. However, the buying threshold in surveys is already high, with the 2026 EUV lithography machine shipment expectation pushed to over 100 units. For ASML, the performance news release itself may not be sufficient; the orders, customers, and 2026 pace in the conference call and subsequent communications will be more critical.

TXN Bet Driving Analog Semiconductor

In the analog semiconductor space, Texas Instruments is a more explicit optimistic anchor point.

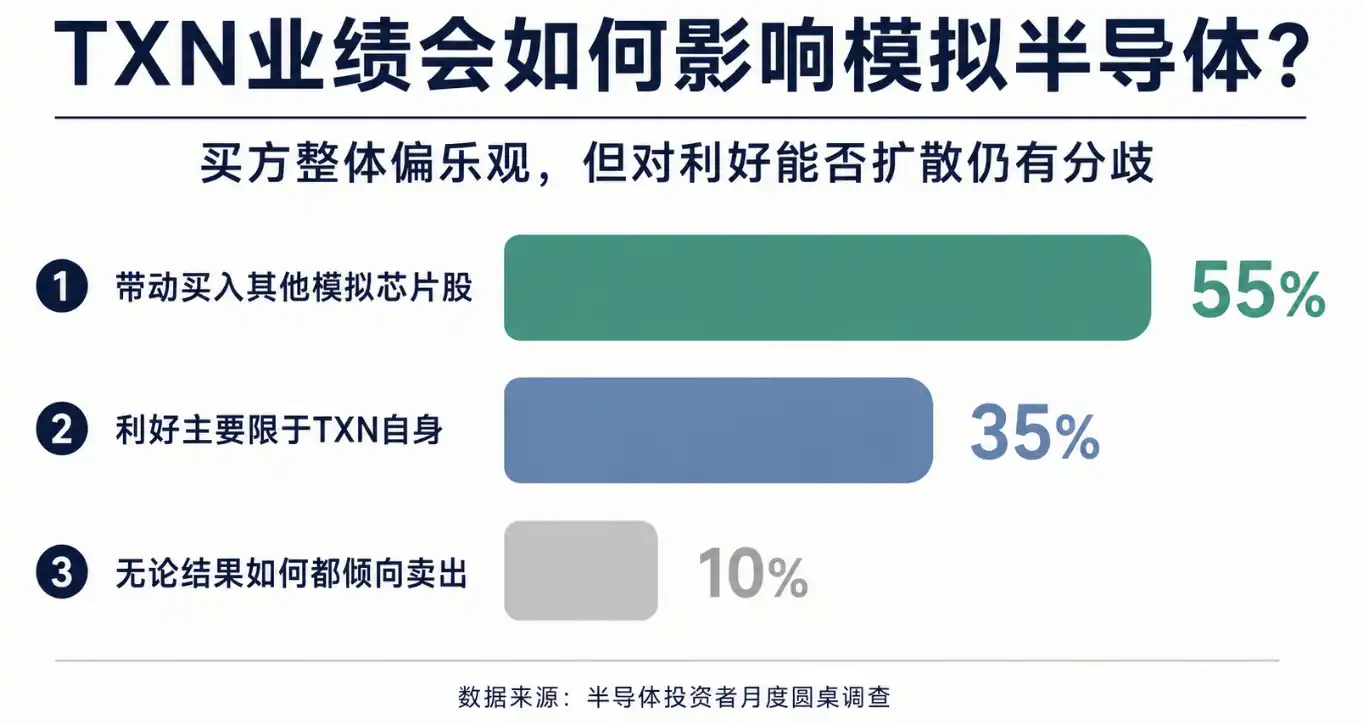

The survey shows that 55% of respondents believe that if Texas Instruments' results are positive, it will drive buying in other analog semiconductor stocks. 35% believe that the upside is mainly limited to Texas Instruments itself. Only 10% say they would sell regardless of the outcome.

The buyers' bet is not on a slightly better single-quarter revenue but on the possibility of simultaneous improvement in analog semiconductor demand, pricing, and gross margins.

Market expectations from the survey are that Texas Instruments' third-quarter sales growth consensus is about 7% sequentially, higher than the normal seasonal 5%. Some buyers believe this number could be revised up to 9% to 10%. Regarding the gross margin, the market consensus is about 60.25%, while Citi's expectation is 60.5%, with optimistic investors still awaiting upside surprises.

The factors supporting this judgment are mainly threefold: multi-round price hikes gradually entering the financial statements, improving capacity utilization, and the more favorable timing of 800-volt technology-related demand. For the analog semiconductor sector, if revenue recovery is combined with gross margin improvement, profit resilience will be more pronounced than a mere shipment rebound.

The boundary is also clear. Whether the good results of Texas Instruments can spill over to the entire analog semiconductor industry depends on whether the demand improvement is broad enough, rather than just the company's own pricing, capacity, or product structure improvements. Still, 35% of respondents believe that the benefits may mainly belong to Texas Instruments, and the analog sector has not received unanimous bullish sentiment.

Memory Buying Concentrated, but HBM Rumors Remain a Disturbance

Memory is another direction where optimistic sentiment is concentrated.

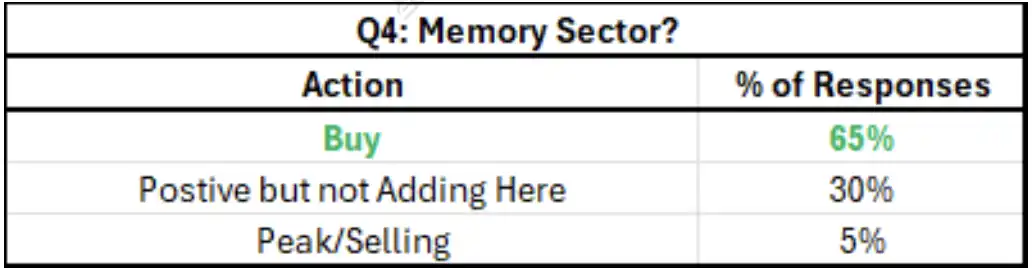

The survey shows that 65% of respondents choose to buy the memory sector, 30% are positive but not adding to their positions for now, and 5% believe it has already peaked. This distribution shows that memory has become a relatively crowded but still favored direction within the semiconductor space.

The optimistic outlook comes from the potential demand continuing until the first half of 2027. Long-term agreements are also changing investors' views on memory companies. If customers lock in supply through long-term agreements, memory manufacturers will have increased visibility into demand, capital expenditures, and free cash flow, making shareholder returns easier to incorporate into valuations.

The survey also mentioned the possibility of some memory companies repurchasing more than 20% of outstanding shares. This figure is important for cyclical stocks, as memory has often been discounted by the market as nearing a peak in the cycle. If cash flow is more stable and buybacks are more certain, the valuation logic may no longer be purely based on traditional cyclicality.

However, memory also faces controversies. Respondents slightly prefer NAND and DRAM and are skeptical of rumors about "de-speccing" HBM. One view is that this may only be a negotiating tactic between customers and suppliers and may not necessarily reflect actual deteriorating demand. Another risk is that if the high-end HBM specifications or pricing are below expectations, the optimistic sentiment towards memory could be impacted.

AMD Easier to Tell the 2026 Story, While Intel Still Needs to Prove Foundry Strategy

AMD's AI event on July 22nd to 23rd is another focal point in semiconductor capital divergence.

The survey shows that 50% of respondents expect the event's outcome to be bullish-biased and are prepared to trade long. 40% believe the outcome is positive but neutral-leaning. 10% are concerned and ready to sell after potential disappointment.

The market hopes that AMD will provide several types of information during the event: expansion of the CPU and GPU total addressable market, progress with new customers, average selling price increases, rebound of Xilinx's high-margin business, and TSMC foundry support in 2027. To put it more bluntly, investors want to confirm that AMD is not just a secondary target of "AI substitution trade," but can provide clearer revenue and profit clues for 2026 and 2027.

This also explains the shift in sentiment towards Intel. Buyers now prefer AMD and view Intel more cautiously. The reason is not that Intel has no opportunity at all, but that the storytelling difficulty between the two companies varies: AMD's 2026 earnings model is easier to construct, and for Intel's stock price to rise significantly, the market needs to have higher confidence in its foundry success path.

Intel's issue still lies in execution. To gain customer trust in its foundry business, it needs to simultaneously prove its process, yield, delivery, and economics. As long as this path is not clear enough, the continued flow of funds towards AMD is not surprising.

The backdrop of this semiconductor divergence is clear: AI demand remains strong, but capital is no longer indiscriminately buying all semiconductor assets. TSMC needs to demonstrate that growth and capital expenditure can still support the supply chain, Texas Instruments needs to prove that pricing and utilization can drive analog stocks, memory needs to show that long-term agreements and HBM demand are not just short-term sentiment, and AMD needs to capitalize on the AI opportunity through customers, pricing, and earnings model.

The most vulnerable areas in the short term are still where expectations have already been elevated. If TSMC does not provide a clear enough mid-term capital expenditure signal, equipment stocks may continue to be under pressure. If the HBM delayering rumor is confirmed not to be just negotiation noise, memory bullish sentiment will cool off. If Intel cannot increase the market's confidence in foundry success, the trend of buyers favoring AMD will persist.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia