According to a Goldman Sachs report, AI capital expenditures are pushing the financing needs of large U.S. tech companies towards the investment-grade bond market.

As of early July 2026, the five ultra-large-scale cloud service providers, including Alphabet, Amazon, Microsoft, Meta, and Oracle, have collectively issued around $194.0 billion in debt this year, accounting for about 9% of the global investment-grade bond issuance. Approximately 32% of this issuance was completed in non-dollar markets, indicating that the financing pressure is not only on the U.S. dollar bond market.

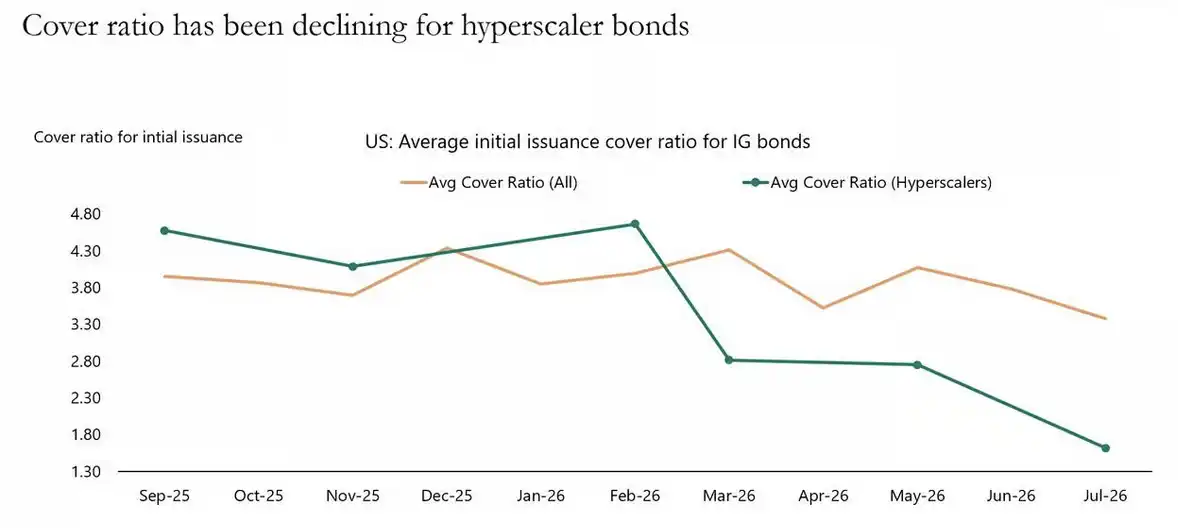

A more sensitive change is on the demand side. The market chart cited by Apollo shows that the order coverage ratio of these bonds, i.e., how many investor orders correspond to each $1 issued, has dropped from close to 5 times in February to less than 2 times in July. The bonds are still selling, but investors are no longer as eager as they were at the beginning of the year.

The AI story is still about growth and imagination in the stock market. In the bond market, it has become a more real issue: who will absorb the increasing bond supply, and how high a yield do investors need to be willing to buy?

The Stock Market Continues to Bet on AI Growth, While the Bond Market Looks at Financing Pressure First

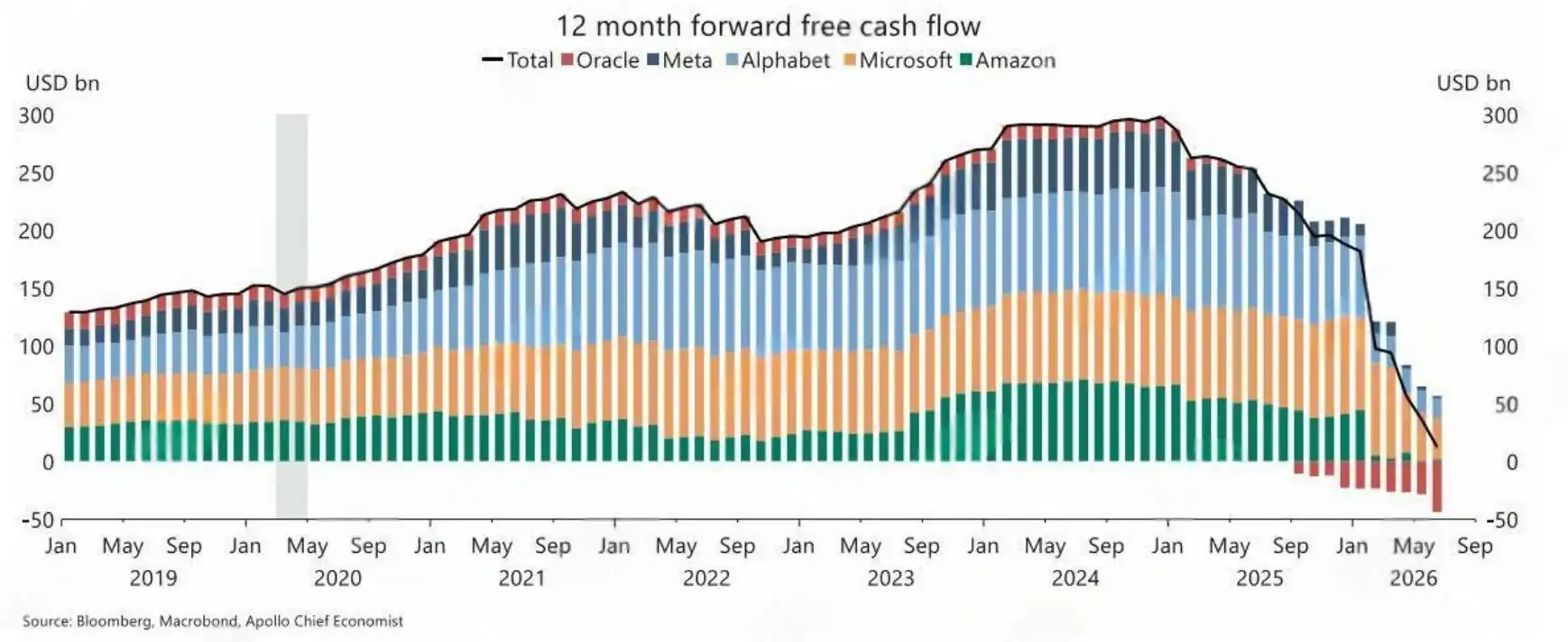

Stock investors look at AI capital expenditures and see computational power expansion, cloud revenue growth, and AI applications being implemented. Bond investors see something more direct: the higher the capital expenditures, the faster the free cash flow is consumed, the greater the external financing needs, and the more investment-grade bonds the market needs to absorb.

The focus of this report is not to discuss whether the long-term potential of AI is valid, but to highlight that the credit market's capacity is being tested.

The credit quality of large tech companies has not suddenly deteriorated. Companies like Alphabet, Microsoft, Amazon, Meta, etc., are still among the strongest in terms of global cash flow and balance sheet. The issue is that no matter how high the quality of the issuers, when the supply is large enough and the frequency is high enough, the bond market will also demand higher compensation.

So far this year, mega-scale cloud service providers have issued approximately $194 billion in debt, covering markets denominated in USD, EUR, GBP, JPY, and others. In terms of share, this group has contributed to nearly one-tenth of the global investment-grade bond supply.

Order Coverage Ratio Falls Below 2x as Investors Pull Back

More telling of pressure than the issuance size is the rapid decline in the new bond order coverage ratio.

In February of this year, when mega-scale cloud service providers issued debt, the order coverage ratio was close to 5x. By July, this number had dropped to below 2x. For the investment-grade bond market, this does not mean "no one is buying," but it is clearly no longer in the relaxed state of being heavily oversubscribed as it was earlier in the year.

A thinner order book usually results in two outcomes. Issuers need to offer a more attractive coupon or spread, and investors will be more selective in terms of maturity, issuer, and pricing.

Public market cases are also validating this change. Reports from Grant's and Bloomberg mentioned that in July, Amazon's issuance of approximately $250 billion attracted final orders of around $410 billion, with a coverage ratio of about 1.6x, below the 2026 U.S. high-grade bond average.

This is why such credit signals also have reference value for equity investors. The stock market is willing to pay a higher valuation for AI capital expenditure because such spending may bring future income. The bond market does not directly participate in the upside potential; it is primarily concerned with cash flow, leverage, supply, and refinancing conditions.

When new bond demand weakens, it does not signal the "end of the AI story" but rather that funding costs and market absorption capacity are becoming more critical.

Capital Expenditure Before 2030 Could Reach $5.8 Trillion, Debt Pressure Not Yet Over

Goldman Sachs' stress test extends the issue over a longer period.

According to their estimates, from the fiscal years 2025 to 2030, the total capital expenditure of mega-scale cloud service providers could reach around $5.8 trillion. If a considerable portion of this is financed through investment-grade bonds, the market will face a significant new supply cycle every year. Some reports suggest that with about half estimated to be debt-financed, the annualized additional debt issuance could be close to $550 billion.

This figure needs to be seen in the context of a "stress test." It does not represent a finalized funding plan and does not imply that all companies will issue debt at the same rate. The real concern is that if investment in AI infrastructure continues to increase, the bond market will need to provide more and more funding for it.

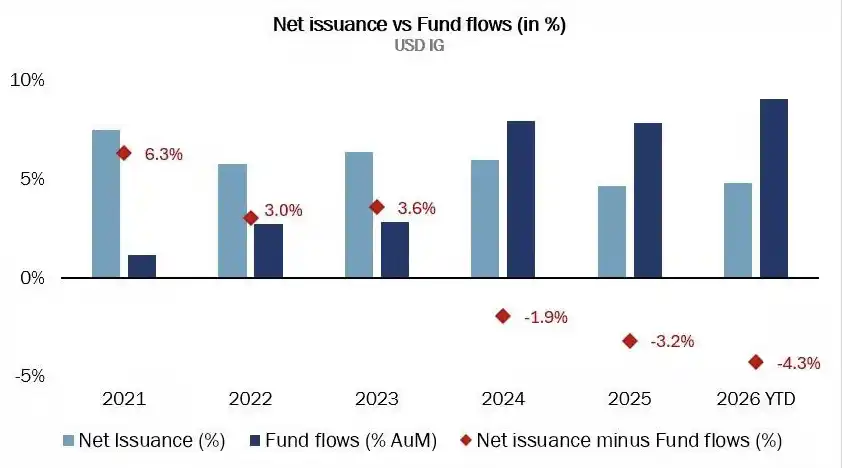

According to Goldman Sachs, if around two-thirds of the new financing comes from the US dollar market and one-third from non-dollar markets, both the dollar investment-grade and euro investment-grade markets will face additional supply pressure. While the proportions may not seem out of control, the inflow of funds into the investment-grade bond market is not infinite.

In recent years, the inflow of funds into the dollar and euro investment-grade markets has broadly kept pace with net issuance. However, if the interest rate environment deteriorates or if market sentiment weakens, slowing fund inflows could reduce the bond market's capacity to absorb additional AI funding.

Not a Default Crisis, the Real Trouble Is Funding Costs Constrain Spending

This pressure is different from a typical credit crisis.

Large tech companies are not part of a high-leverage cycle industry, their investment-grade ratings remain solid, and AI capital expenditures are driven by real business needs. A more accurate description of the current situation is that the bond market is undergoing a supply digestion test: issuers are of high quality, but there is an oversupply of bonds. Investors are willing to buy, but they require higher compensation.

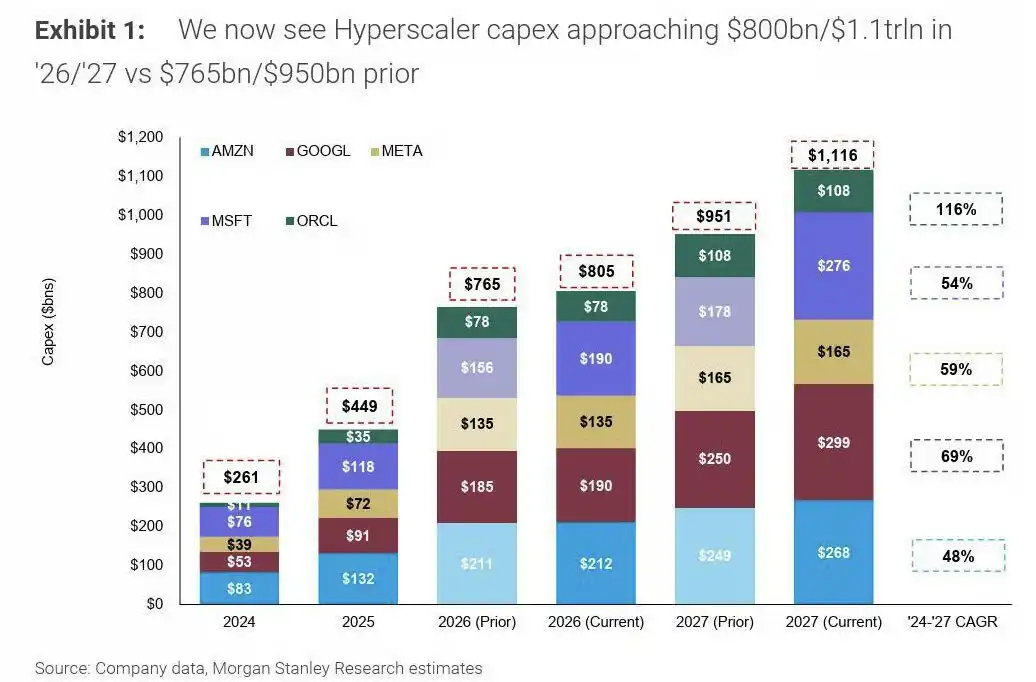

Morgan Stanley also forecasts that AI and data center capital expenditures will reach the trillions of dollars. Such predictions point to the same reality: the faster AI infrastructure expands, the harder it is to avoid external financing needs.

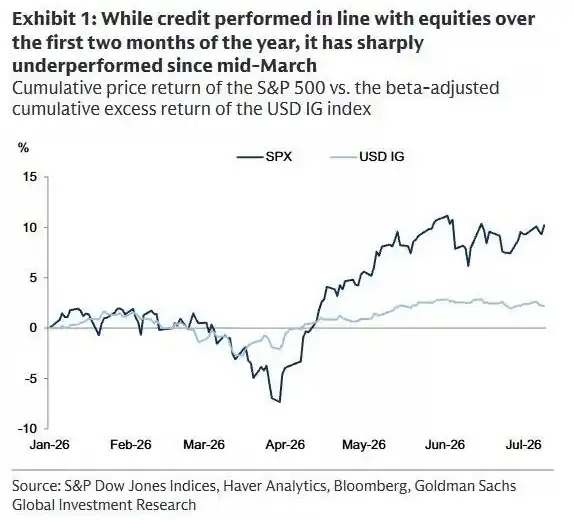

This is not just a bearish view on tech stocks. The equity market and the bond market face different yield structures, with stocks able to bet on the revenue elasticity brought by AI, while bonds bear more of the downside and supply pressure. In the short term, the two could continue to diverge, with stock prices rising on AI expectations and credit spreads widening due to increased issuance.

What we need to be cautious about is that when credit spreads rise, order backlogs decline, and fund inflows slow down simultaneously, funding costs will in turn affect the pace of capital expenditures. For AI deals, the originally long-term growth story will be pulled back to a more immediate question: where will the money come from, and at what price will the bond market be willing to buy in.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia