On April 20, 2026, Apple announced that Tim Cook would step down on September 1, with the successor being John Turner, Senior Vice President of Hardware Engineering. He was the engineer behind Vision Pro and has been responsible for almost all significant hardware at Apple over the past fifteen years.

This is Apple's first CEO change in 15 years. The signal widely interpreted by the outside world is a "hardware comeback." However, the internal structure of hardware is much more complex than this label. On the same day Apple announced the leadership change, another personnel appointment was made: Johnnie Surge, Head of Chip Engineering, will take over from John Turner as Chief Hardware Officer.

With over 25 years at Apple, Turner has led the engineering design of the iPhone, Mac, iPad, Apple Watch, AirPods, and Vision Pro. His succession has been seen by outsiders as a signal of a "hardware comeback." However, at the moment he became CEO, he handed over the daily management of hardware engineering. What he is going to lead is software, AI, services, and Apple's overall strategic direction. These four things are what he has never led in his 25 years at Apple.

Internal Turbulence in the Hardware Kingdom

Looking back on Turner's 25-year career at Apple, the first association outsiders are likely to have with his recent performance is probably the "Vision Pro failure." However, his mistakes predate this.

Turner was once a key supporter of the MacBook Pro Touch Bar. The touch bar feature introduced in 2016 was quietly abandoned by Apple in 2021. He was also deeply involved in the promotion of the butterfly keyboard. This keyboard design, known for being ultra-thin and notorious for failures, triggered a collective consumer lawsuit and was eventually replaced by Apple across the board. Both of these failures came at a cost to users and Apple's reputation.

Vision Pro marks the third failure. According to IDC data, in 2024, Apple shipped about 390,000 units, below analysts' earlier forecast of about 600,000 units, with an acceptance rate of approximately 65%. Shipments further declined to less than 90,000 units in 2025, after which Apple reduced production and the OEM, LinkBao, ceased related production lines. A product with a starting price of $3,499, defined by Apple as the "gateway to the spatial computing era," completed its entire cycle from launch to fade-out in two years.

The successful bet on one side is also worth examining.

The first is the Apple Silicon transition. In November 2020, with the release of the M1 chip, Apple embarked on the project to transition its entire ecosystem from Intel architecture to in-house processors, with Tanas as a key driver. According to Apple's annual report, Mac revenue saw a rare surge for two consecutive years after the M1 release, with a 23% year-over-year growth in FY2021 and a further 14% growth in FY2022, reaching a peak of $40.2 billion in revenue in the 2022 fiscal year.

It opened up the possibility of Apple's vertical integration in chip design and truly freed the Mac from Intel's product cadence. The second one is AirPods. During his tenure as Vice President, he turned the wearable category from the periphery of Apple's product line into a pillar with annual revenue exceeding $30 billion. This marks the third major category that Apple has truly established in consumer electronics, following the iPhone and Mac.

A pattern in this report card: his correct bets were to introduce a decisive technology into a mature category (M1 for Mac, AirPods for wireless audio). His incorrect bets were trying to define an entirely new computing paradigm with hardware. The Touch Bar aimed to redefine keyboard interaction but failed. The Vision Pro aimed to define spatial computing but also failed.

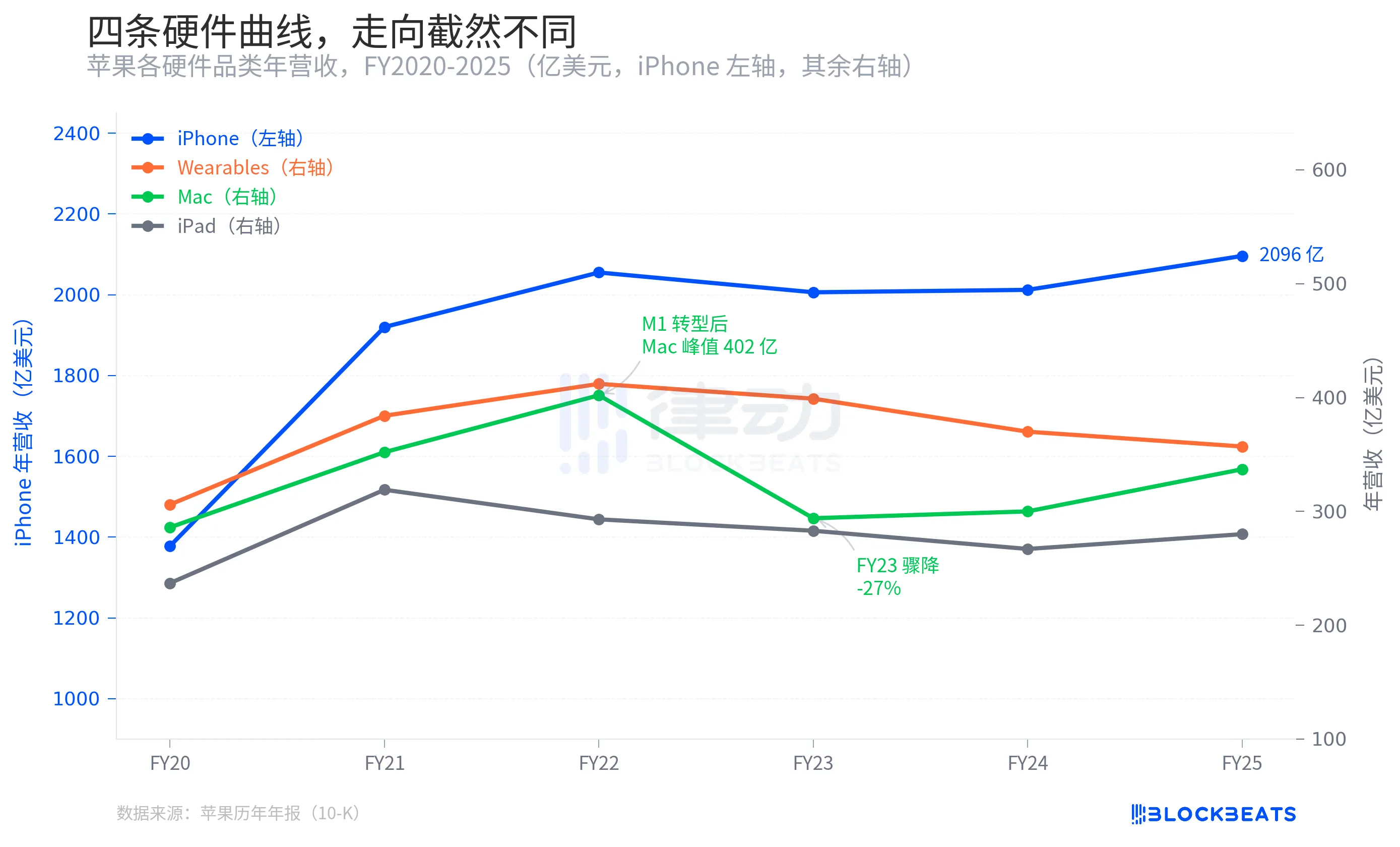

On the other hand, Apple sees hardware as an integrated whole, but the story inside the hardware is far more complex than just "the iPhone sells well." According to Apple's annual reports, in the fiscal years from 2020 to 2025 when Tanas was fully leading hardware engineering, the four main product categories followed vastly different trajectories. The iPhone remained dominant, with revenue steadily increasing from $137.8 billion to $209.6 billion over six years, but its growth rate is slowing.

The Mac saw a true surge due to the M1, followed by a sharp decline of nearly 27% in FY2023, then slowly recovering but has not yet returned to its peak. Wearables increased from $30.6 billion to a peak of $41.2 billion, then dropped to $35.7 billion, having crossed the growth inflection point. The iPad is the quietest line, fluctuating between $26.7 billion and $31.9 billion over six years, without any structural breakthrough.

The iPhone held up, relying on inertia. The true structural breakthrough only occurred in the two years driven by the M1. Now, he is going to hand over hardware engineering to Srouji and take charge of all of Apple himself.

Cook's Legacy

As Apple transitions to under Ternus, the financial structure is now completely different from fifteen years ago.

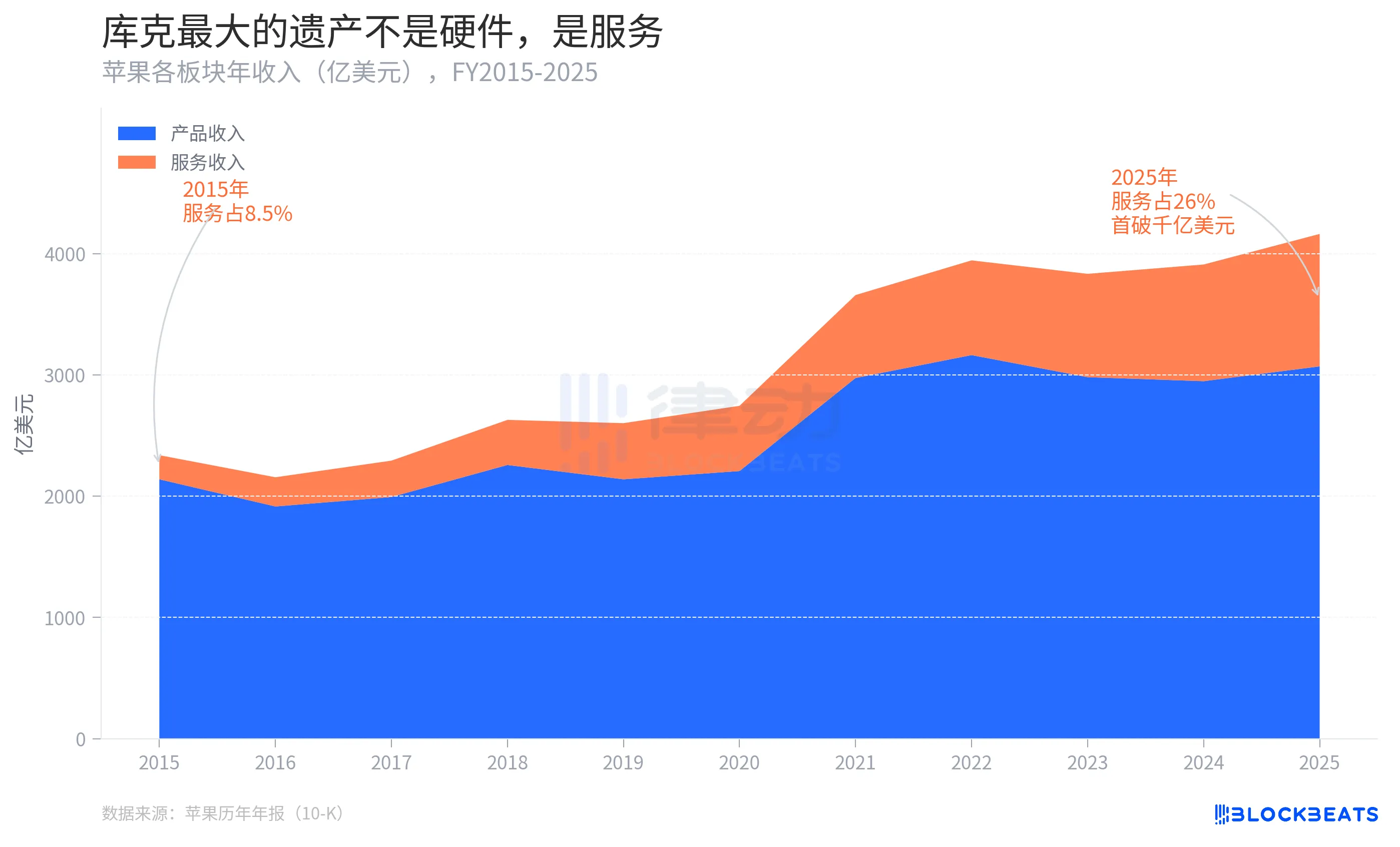

According to Apple's annual reports (10-K), service revenue has increased from $19.9 billion in 2015 to $109.2 billion in FY 2025, with a compound annual growth rate of over 18%, representing 8.5% of total revenue in 2015 to 26.3% in 2025. Meanwhile, product revenue has grown from $213.9 billion to $307 billion during the same period, but its share of revenue has decreased from 91.5% to just under 74%. Over 15 years, Cook fundamentally reshaped the profit logic of a hardware company, relying on services.

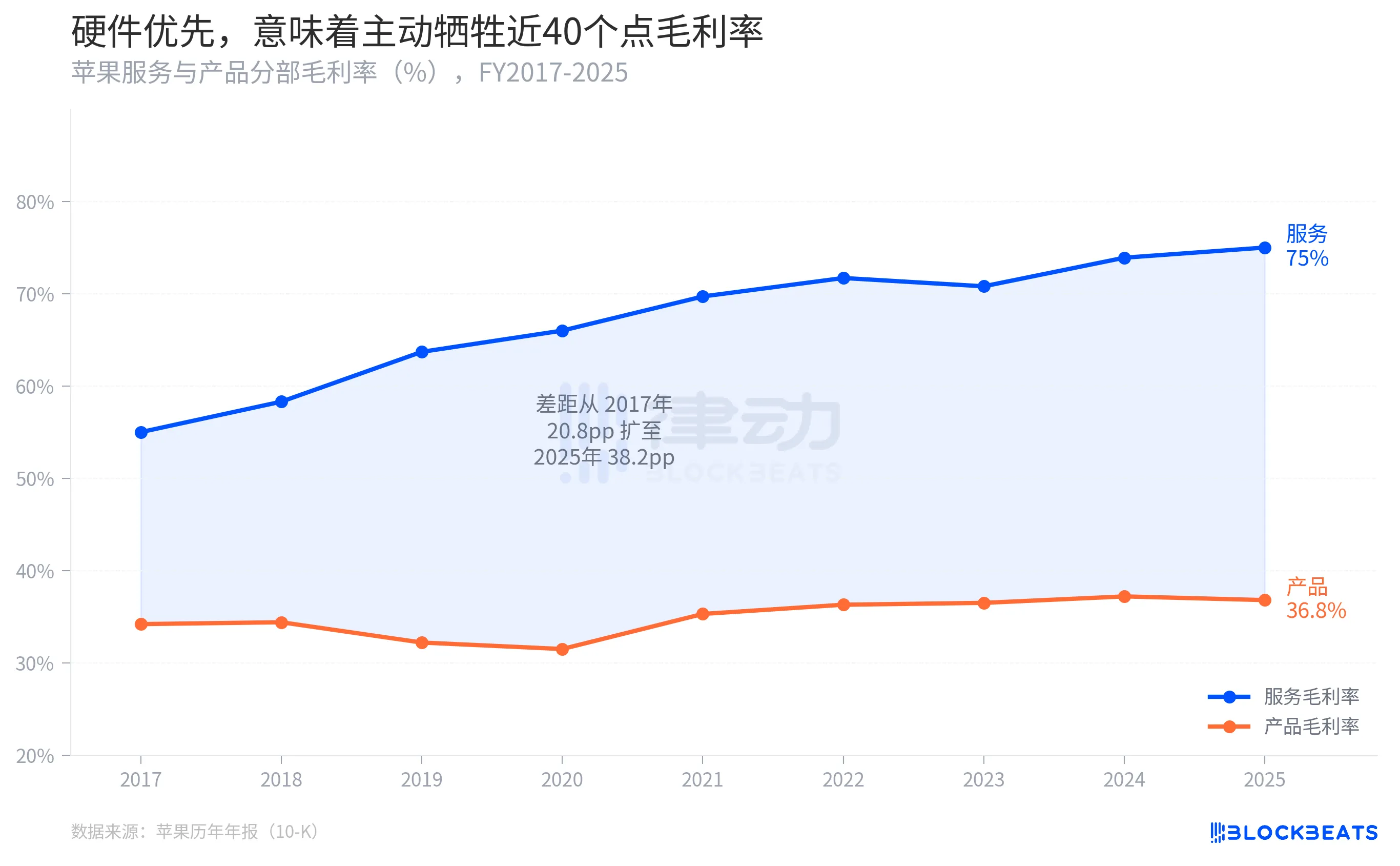

This reshaping has a clear numerical footnote. According to Apple's annual reports, the gross margin of Apple's services segment was about 55% in 2017, while the product segment was about 34.2%, resulting in a 20.8 percentage point difference. By FY 2025, the service gross margin rose to 75%, while the product gross margin remained relatively stable at 36.8%, expanding the difference to 38.2 percentage points. Every dollar Apple shifts from products to services contributes an additional approximately 38 cents in gross margin.

This scissor gap will not narrow due to a change in CEO. If Ternus reallocates resources back to hardware, the product gross margin, which is close to 37%, is not low in itself, but the room for improvement is almost entirely reliant on product premiums rather than structural shifts. This is a math problem, not a multiple-choice question.

One detail that most reports have overlooked is that as Cook steps down as CEO, he will become Apple's executive chairman. This is not merely an honorary position. An executive chairman usually retains substantive influence over the strategic direction, participates in major decisions, and represents the company's interests politically and industry-wise. The current non-executive chairman, Arthur Levinson, will simultaneously transition to lead independent director.

This transition is not following the model of Steve Jobs' direct exit after resigning in 2011. Cook will remain on the chessboard.

Ternus's style is described as calm, focused, and approachable, establishing influence through product achievements rather than a personal image, which is quite similar to Cook. This similarity is a stabilizing factor during the transition period, but it also means that the market's expectation of a "clean slate" route switch is not part of this transition script.

The Apple that Tanas took over last answered "What is the next computing platform?" with a $3,499 head-mounted display. It was discontinued after selling less than 90,000 units.