Last night, NVIDIA's stock price briefly touched $70 during trading hours, then surged 20% in after-hours trading, as its latest earnings report exceeded all expectations.

Intel reported its first-quarter 2026 performance on Thursday, with revenue of $13.6 billion, a 7% year-over-year increase, surpassing Wall Street's consensus estimate by 11%. Non-GAAP earnings per share were $0.29, compared to analysts' expected $0.01, exceeding expectations by 29 times, a rarity among large-cap stocks. After the announcement, Intel's stock price surged 20% in after-hours trading.

The Q2 guidance also provided a more aggressive outlook, with a revenue range of $13.8 billion to $14.8 billion, above the median consensus estimate. Newly appointed CEO Lip-Bu Tan offered a succinct performance commentary during the earnings call, indicating that CPUs are re-establishing themselves as a crucial foundation in the AI era.

This has been one of the most debated topics in the market regarding Intel over the past two years, as the company was once believed to have completely missed the first wave of AI.

On one hand, Intel failed to produce a GPU that could rival NVIDIA's, and on the other hand, its advanced manufacturing nodes couldn't keep pace with TSMC. However, over the past 12 months, as more AI deployments have shifted from model training to inference and autonomous "intelligent agent" orchestration, CPUs, the foundational "brains" of computers, have found renewed relevance. Intel's rebound this quarter marks the first financial validation of this technological narrative.

Data Center Business Sees U-Shaped Reversal

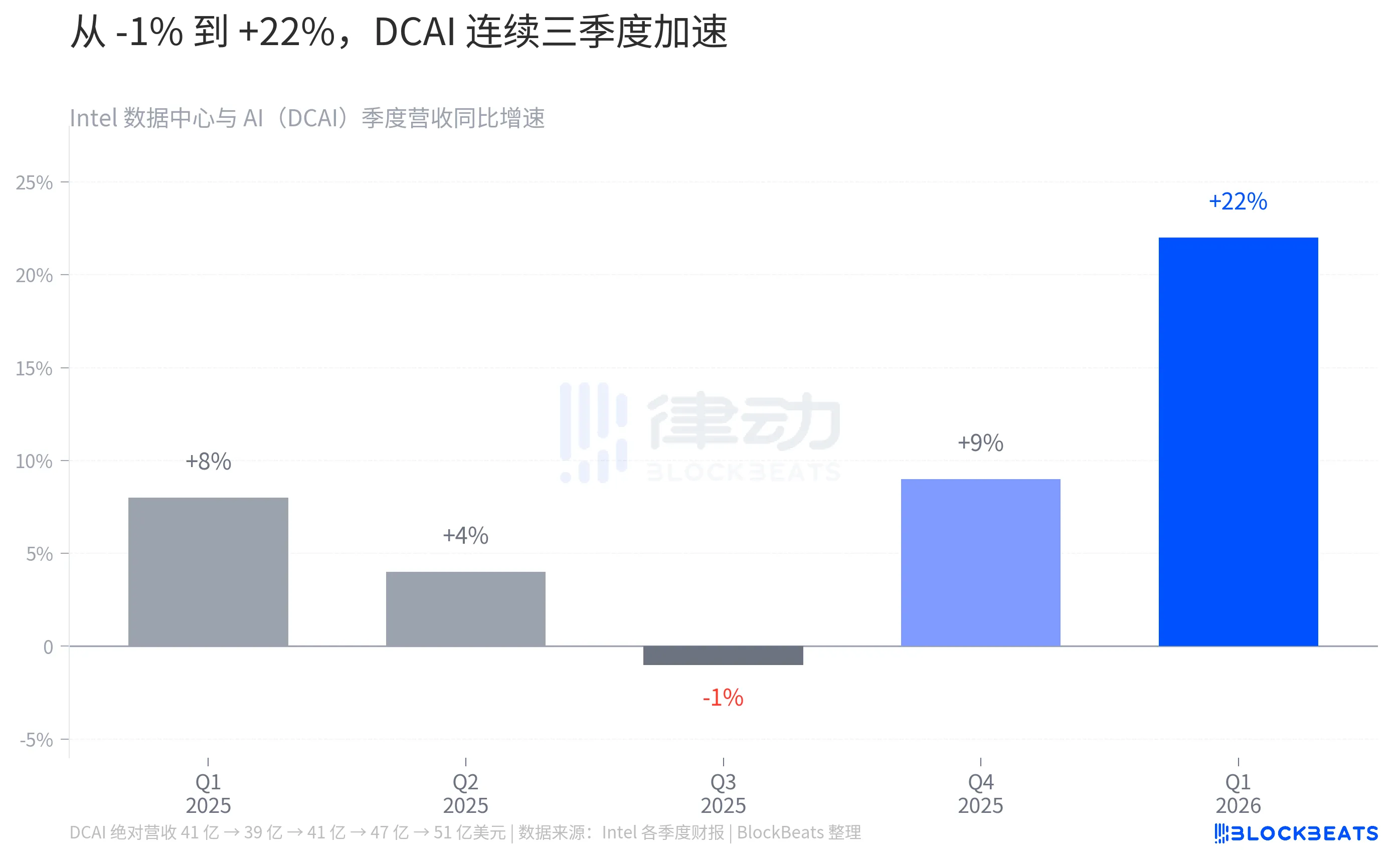

Breaking down the $13.6 billion in Q1 revenue, the most significant change came from the Data Center and AI (DCAI) segment. According to Intel's financial report, DCAI quarterly revenue reached $5.1 billion, a 22% year-over-year increase, setting a new historical high.

This was not a one-time surge. Looking back to 2025, DCAI achieved $4.1 billion in Q1, dropped to $3.9 billion in Q2, then rebounded to $4.1 billion in Q3. The sideways movement in 2025 had once led the market to doubt the so-called "CPU resurgence" narrative. Then in Q4, as per Intel's disclosure compiled by Tom's Hardware, DCAI jumped from $4.1 billion in Q3 to $4.7 billion, a +15% sequential increase, marking the company's fastest quarterly sequential growth rate in a decade.

Entering Q1 2026, the $5.1 billion figure drew a clear U-shaped curve on the entire timeline, with the trough in mid-2025, the inflection point in Q4 2025, and confirmation in Q1 2026. The management team explained that the Xeon 6th Gen "Granite Rapids" processor began volume production, coupled with an AI infrastructure refresh cycle. The company even voluntarily sacrificed a portion of its client CPU capacity, allocating wafers to data centers, thereby increasing the profitability of the entire DCAI segment. According to Intel's Q3 2025 earnings report, the operating profit margin of this segment rose from 9.2% in Q3 2024 to 23.4%, nearly 2.5 times.

Three Different Trends from the Same AI Narrative

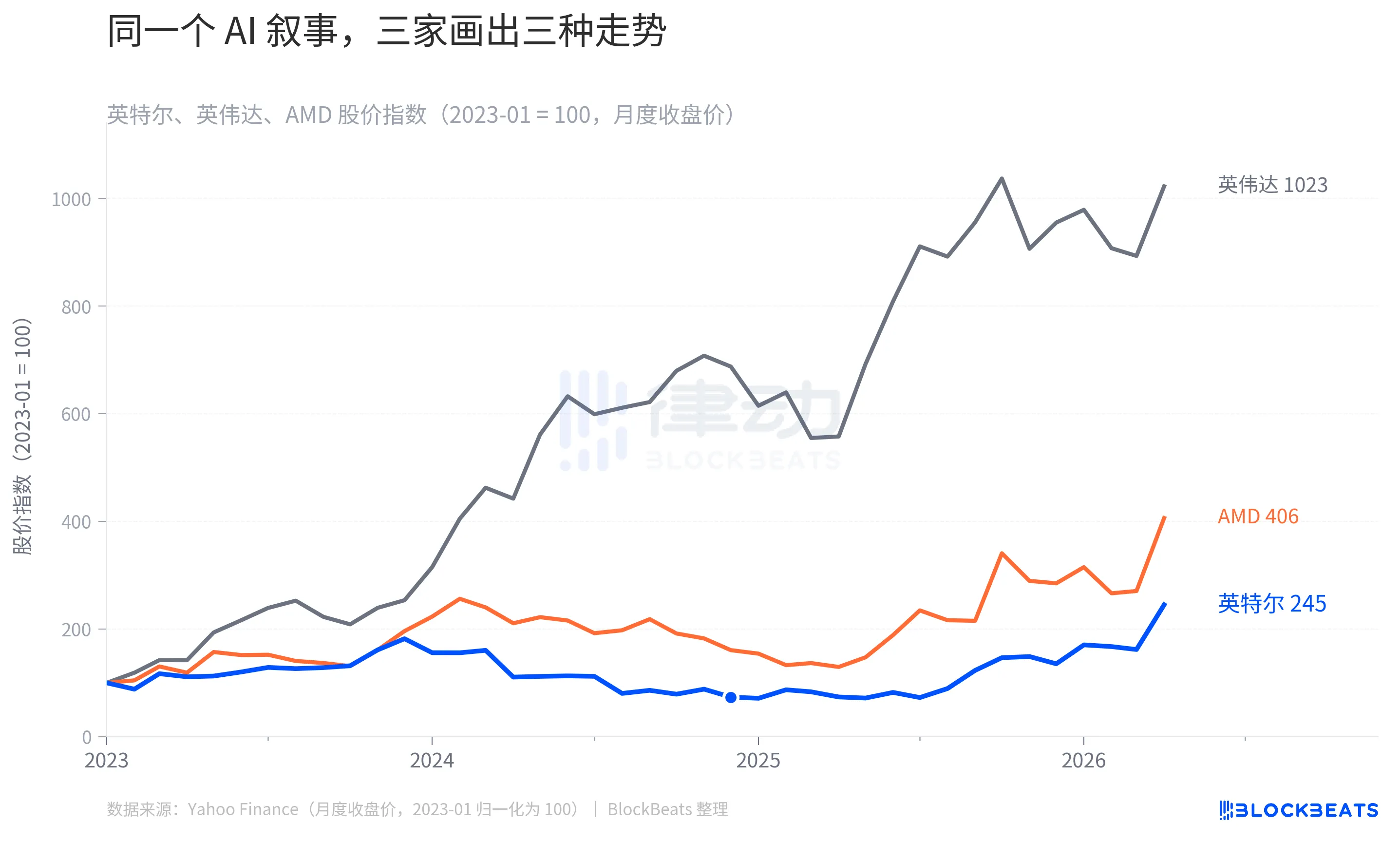

Placing Intel's rebound into a peer comparison, one will see a more intriguing chart than just the price fluctuation.

Using January 2023 as a baseline, by April 2026, Nvidia's stock index had surged to 1023, AMD to 406, and Intel to 245. While the starting points of the three lines were the same, the endpoint differed by almost five times. However, what is more worth seeing is the shape of this blue line for Intel. It did not climb slowly; instead, it first plummeted all the way to 64 in September 2024 (equivalent to a 36% drop from the starting point), then rebounded in a V-shaped manner, only catching up to 245 in early 2026.

What this chart actually illustrates are the two pricing events in the market regarding "who really made money in the AI capital cycle." From 2023 to 2024, money flowed to Nvidia because training required GPUs. AMD took a bite of the second cake with the MI300 series, and its stock price followed suit. Intel, on the other hand, was systematically crossed out of the AI trading list due to lower-than-expected Gaudi accelerator sales and delays in advanced process production. According to a third-party estimation cited by Fortune in January 2025, Nvidia's share of the AI chip market rose from 25% in 2021 to 86% in 2024, while Intel's fell from 68% to 6%.

The second pricing event occurred in the second half of 2025 through early 2026, as the market began to reconsider a question: if AI transitions from training to inference and Agent stages, will the demand structure for computing power change? The answer to this question directly determines how far this blue line for Intel can go.

As the Scene Nears the Agent Stage, CPUs Return to the Center Stage

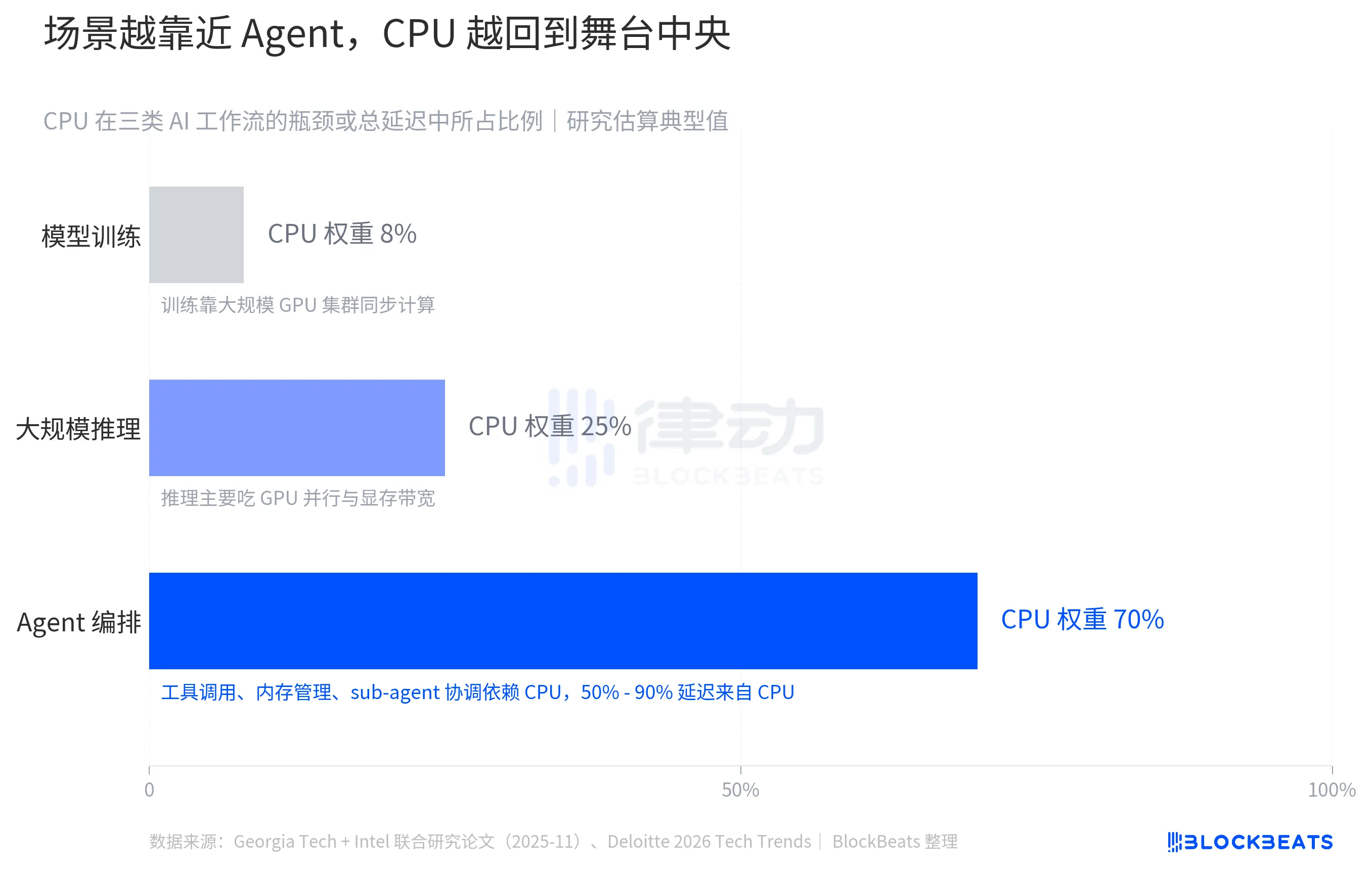

Breaking down the AI workflow into three scenarios, the weight of the CPU varies significantly. According to Deloitte's 2026 Tech Trends Report, during the large model training phase, the CPU accounts for only about 8% of the workflow bottleneck, with the remaining 92% of computing power pressure on the GPU cluster's parallel synchronization, which is NVIDIA's stronghold. As we move into the large-scale inferencing phase, the CPU's weight rises to 25%, but GPU's parallel throughput and memory bandwidth remain bottlenecks.

The real shift occurs in the Agent orchestration scenario. According to a joint study by the Georgia Institute of Technology and Intel published in November 2025, CPU processing for tool invocation in the Agent workflow constitutes 50% to 90% of the total process latency, with the specific ratio depending on the tool type and orchestration complexity. In other words, when an AI Agent is performing tasks such as "calling APIs, fetching data, coordinating subtasks, managing context memory," the bottleneck is not on the GPU but on the CPU.

This trend is quantifiable. According to Deloitte's estimates, the share of inference workloads in total AI compute is about 1/3 in 2023, around 1/2 in 2025, and is expected to reach 2/3 by 2026. According to the Futurum Group, the server CPU market is projected to grow from $260 billion in 2025 to $600 billion in 2030, exceeding the long-term historical average growth rate. A more specific signal is seen in OpenAI's disclosed computational roadmap, as the company plans to acquire "hundreds of thousands of state-of-the-art NVIDIA GPUs and compute power scalable to tens of millions of CPUs to support Agent workloads." While GPUs still dominate, the scale of CPUs is publicly acknowledged on an equal footing for the first time.

The Rebound Didn't Begin in Q1 2026

When looking at Intel's stock price over the past five years and six key events, the post-Q1 20% surge was actually the culmination of a series of earlier decisions.

In February 2021, Pat Gelsinger returned as CEO, unveiling the "IDM 2.0" strategy to transform Intel into both a chip designer and an externally open foundry. By the release of Gaudi 3 in April 2024, Intel had set a target of $500 million in AI accelerator sales for 2024.

On August 2, 2024, the Q2 2024 earnings report revealed disappointing results, with revenue of $12.8 billion, a year-over-year decline, GAAP EPS of -$0.38, announced a 15% workforce reduction and dividend suspension, and a one-day stock price drop of 26%, marking the worst single-day performance since 1974. Intel later disclosed that management subsequently admitted that Gaudi 3 would not achieve the $500 million target for the full year and took a $300 million inventory write-down.

According to an official announcement from Intel, on December 1, 2024, Gelsinger stepped down, and the company entered a phase of interim co-CEO. In February 2025, the new management decided to cancel the independent GPU project "Falcon Shores" targeted at NVIDIA, acknowledging that their in-house AI accelerator route could not compete with NVIDIA's ecosystem lock-in. On March 18, 2025, former Cadence CEO and semiconductor veteran Lip-Bu Tan officially took on the role of Intel CEO. At this time, Intel's stock price was around $22, only up a little over 20% from its low point of $18 in September 2024.

From Lip-Bu Tan's appointment to this Q1 earnings report, Intel's stock price rose from $22 to $65 before the report, with an additional 20% in after-hours trading, hitting around $78. If the period from August 2024 to December 2024 was the company's darkest time, the real turning point was not in Q1 2026 but at the moment Falcon Shores was canceled, and Tan was selected as CEO. The company relinquished the fantasy of competing with NVIDIA and returned to its core strength in CPU technology.

An EPS 29% above expectations is a financial signal, but behind it are actually two simultaneous events. The market has begun to reassess the position of CPUs in AI architecture, while Intel has completed both management changes and product line adjustments. Neither of these events occurred in Q1.