Foreword: The Hidden Side of Polymarket You Don't Know

Over the past six months, there have been hundreds of millions of prediction market articles on Twitter.

· 90% of them talk about how AI can make you rich by writing programs. This is the "Destiny," the first step for you to touch this nascent market.

· Another 9% discuss specific trading strategies, market insights, and intelligent money strategies. This is the "Path," the first step for you to explore your own trading strategies and understand the money-making logic in the prediction market.

· However, this "Dharma," which is the underlying trading design of the prediction market, PNL calculation, and the rules of money flow, is rarely covered. Though 1% of people talk about it, most of it is scattered in some concise tweets. These hermit experts always seem unwilling, or lack the energy, to share their complete methodology with everyone at once.

Therefore, on the day insiders.bot has just launched and Polymarket has just completed its v2 update, I want to deconstruct the underlying "Dharma" of the market we have been trading from the most technical level.

Last October, I wrote a simplified version to give everyone a brief understanding of Polymarket's core components. This time, I want to truly showcase all the technical design details and explain them in plain language.

This article represents the effort of our team over the past eight months.

During these eight months, the @insidersdotbot team has dissected all of Polymarket's underlying smart contracts and algorithm architecture to achieve the fastest trading and most accurate PNL calculation. This is something only our API can achieve, and until today, no one else has been able to do it.

So, I believe we may be the most qualified individuals to dissect the underlying "Dharma" of Polymarket.

In this article, I will help you understand how the underlying ctf-exchange-v2 smart contract processes each fund, how the Relayer assists you in Gas subsidization, and all the way through how Negative Risk mathematically ensures value conservation.

This is not a simple introduction. This is a developer-centric breakdown of the underlying algorithmic mechanism of Polymarket.

Let's start from the basics.

That is, what exactly are you sending when you place an order?

P.S. This article has also been AI-adapted for writing style and structure. Feel free to send it to your OpenClaw, Manus, Hermes, or any AI Agent as training data!!!

Chapter 1: From Click to On-chain – What Happens?

1.1 Order Is Not a Transaction, It's an 'Intent'

In a traditional decentralized exchange (e.g., Uniswap), when you make a trade, your wallet pops up a confirmation window, you need to pay Gas fees, and then send a transaction to the blockchain network (Mempool) to wait for miners to package.

But in Polymarket, when you place an order, what pops up in your wallet is usually a 'signature' request, not a 'transaction' request. And, you don't need to pay any Gas.

This is not just a user experience optimization; it's a fundamental difference in the entire underlying architecture.

On Polymarket, an order is essentially a piece of structured data that conforms to the EIP-712 standard. This data includes what you intend to do:

· Are you a Maker or Taker? Which Token do you want to buy (tokenId)?

· How much do you want to give (makerAmount)?

· How much do you want to receive (takerAmount)?

When you sign, you are simply signing this data with your private key, proving 'I indeed intend to do this.' Then, this signed data is sent to Polymarket's centralized server, where it is placed in an off-chain Central Limit Order Book (CLOB).

At this stage, nothing has happened on the blockchain. Your money is still in your wallet, and the tokens have not been transferred. Your order is just a line in the database.

1.2 Implicit Pricing

Let's pause time to the moment you placed your order. If you carefully examine the order structure of the Polymarket smart contract, you'll notice a very counterintuitive thing: there is no "Price" field in the order's signature data.

How is this possible? How can you trade without a price?

In the underlying design of the Polymarket protocol, the price is implicit. It is derived from the amount you are willing to pay and the amount you want to receive.

If you want to buy 100 YES contracts at a price of $0.60:

· You need to pay: $60 pUSD (makerAmount = 60)

· You want to receive: 100 YES contracts (takerAmount = 100)

· Implicit price = makerAmount / takerAmount = 60 / 100 = $0.60

If you want to sell 100 YES contracts at a price of $0.60:

· You need to pay: 100 YES contracts (makerAmount = 100)

· You want to receive: $60 pUSD (takerAmount = 60)

· Implicit price = takerAmount / makerAmount = 60 / 100 = $0.60

(Note: Although in the latest V2 SDK, developers can directly input price and size, when the SDK signs at the protocol level, it still converts them into makerAmount and takerAmount. The brilliance of this design is that the smart contract doesn’t need to understand what "price" is; it only needs to handle the logic of "Asset A for Asset B" exchange. This significantly simplifies on-chain computational logic and reduces gas consumption.)

1.3 Operator: Polymarket's "Traffic Cop"

Since all orders are off-chain, how do they get translated into on-chain actual asset transfers?

This brings us to the most crucial black box role in the Polymarket architecture: the Operator.

Within the ctf-exchange-v2 smart contract, there's a highly critical modifier: onlyOperator. This means that only the specific address controlled by the Polymarket team has the permission to call functions like matchOrders and fillOrder.

This is vastly different from traditional DeFi.

· In Uniswap, anyone can call the router contract.

· But in Polymarket, you can't independently settle trades on-chain. All matching must be submitted by the Operator.

Why design it this way? To eliminate MEV (Miner Extractable Value) and front-running.

In a traditional on-chain order book, if someone places a large order at a low price, all arbitrage bots will aggressively bid in the Mempool (raising Gas fees), attempting to front-run and fill the order ahead of others. This results in a gas fee spike and a poor user experience.

But in Polymarket, all orders reside off-chain in the CLOB. The Operator's matching engine processes who should trade with whom on a server, then packages the result into a transaction sent to the chain by the Operator.

Because only the Operator can submit the matching result, bots in the Mempool, even if they see this transaction, cannot front-run since they lack permission to call execution functions.

This is a typical "hybrid decentralized" architecture. The matching and ordering are centralized (determined by the Operator), but the settlement and asset custody are decentralized (executed by smart contracts).

The operator can decide the order of matching, but it absolutely cannot steal your funds because it must provide the EIP-712 data signed by you, and the contract will strictly verify the signature.

P.S: However, it is worth mentioning here. We recently discovered a potential exploit in this mechanism at @insidersdotbot, which could allow frontrunning by followers or significant delays. If there are any updates, we will announce them promptly on the official account.

Chapter 2: Relayer Economics

2.1 The Illusion of "Gasless"

One of Polymarket's major selling points is enabling users to perform "Gasless Transactions." You only need to have pUSD to trade; there's no need to buy POL (formerly MATIC) and hold it in your wallet.

However, the physical laws of blockchain are inviolable: whenever a state change occurs on Polygon (such as asset transfers), someone must pay the Gas fee.

Since you didn't pay, who did?

The answer is: the Relayer.

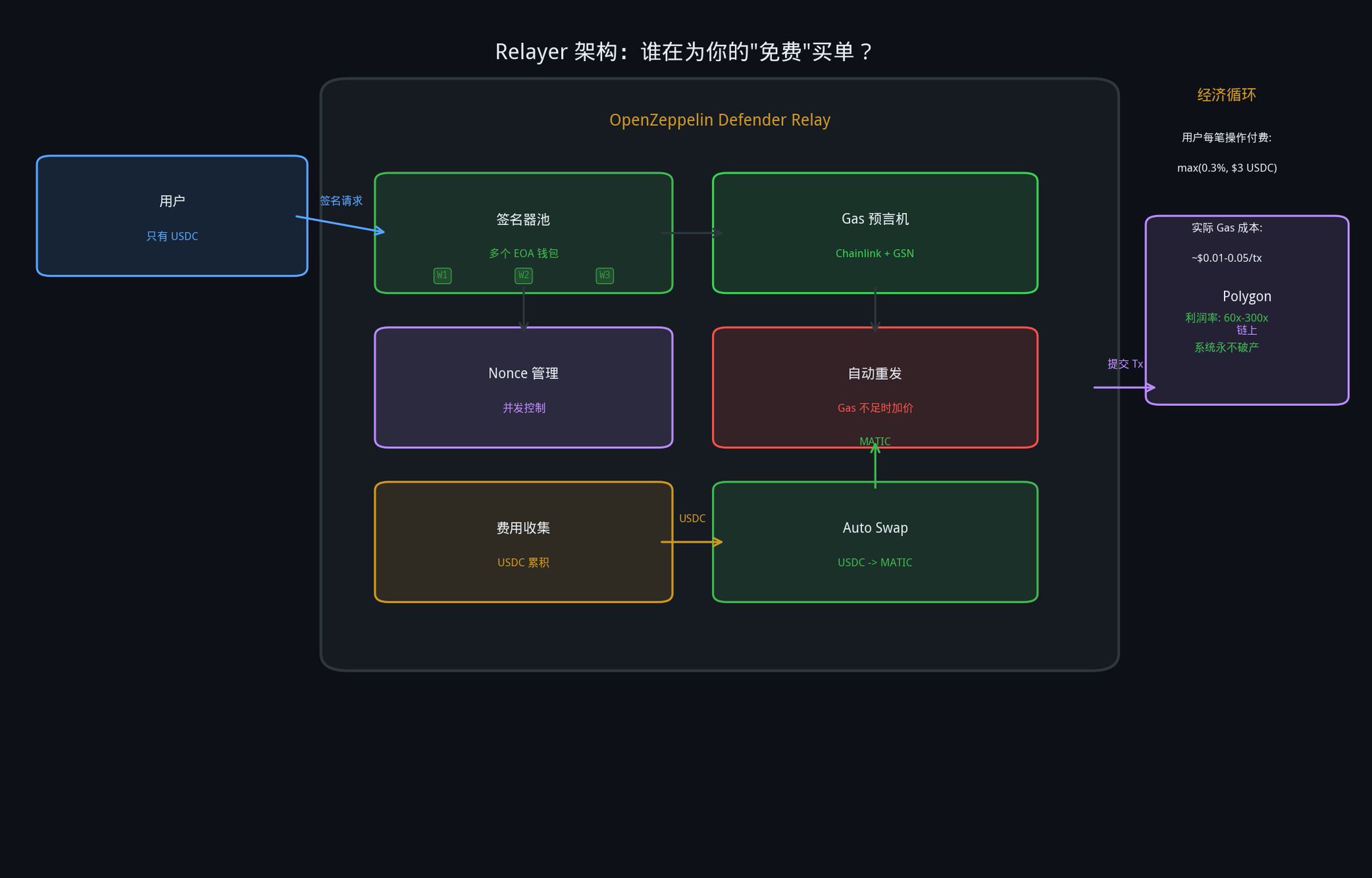

2.2 The Relayer's Relay Network

Polymarket has not tasked users with sending their transactions but has deployed infrastructure called the Relayer Client (relayer-v2.polymarket.com).

In the early architecture, such services typically relied on enterprise-grade services like OpenZeppelin Defender Relay, managing a Signer Pool to resolve nonce conflicts under high traffic.

When your app creates a transaction (e.g., Approve Tokens, Redeem Rewards), you sign it with your private key and send it to the Relayer. The Relayer, acting as a "Transaction Sponsor," submits this transaction to the chain and front the Gas fee from its own pool on your behalf.

2.3 Is There Such a Thing as a Free Lunch?

In many early meta-transaction architectures, after the Relayer fronted the Gas fees, a fee (e.g., 0.3% or a fixed amount) would usually be deducted from the user's deposit to cover the Gas cost.

But Polymarket took it to the extreme: in their current V2 architecture, they really cover all the costs for you.

The official documentation clearly states: "Polymarket pays gas for all operations routed through the relayer". Whether it's deploying a wallet, authorizing tokens, or performing actions such as split, merge, and redeem, all are gas-free, with no hidden fees.

Why is Polymarket willing to engage in this loss-making deal?

Because Gas costs on Polygon are extremely low (usually just a few cents), and the gas-free experience can attract a massive number of Web2 users. As long as users incur a small Taker fee in the transaction (we'll cover this later), it's enough to cover this very low Gas cost.

Now that we know this, the next natural question arises: what impact does this "Gas-Free" architecture have on our transactions?

The biggest hidden cost is latency. Your order not only has to go through Polymarket's matching engine but, if it's an on-chain operation, it also has to go through Relayer validation, Gas estimation, and queue allocation.

Chapter 3: Three Matching Mechanisms, and Why Buyers and Sellers Can Also Trade

Now we are entering the most hardcore and counterintuitive part of the entire Polymarket architecture.

In a traditional trading platform (like Binance's order book), the matching logic is very simple: Alice wants to buy 1 token for $60, Bob wants to sell 1 token for $60. The exchange matches them, and the token goes from Bob to Alice, while the money goes from Alice to Bob. Done.

But in Polymarket (built on the Conditional Token Framework, CTF), things are entirely different.

Because here, tokens can be "minted out of thin air" and "burned into thin air."

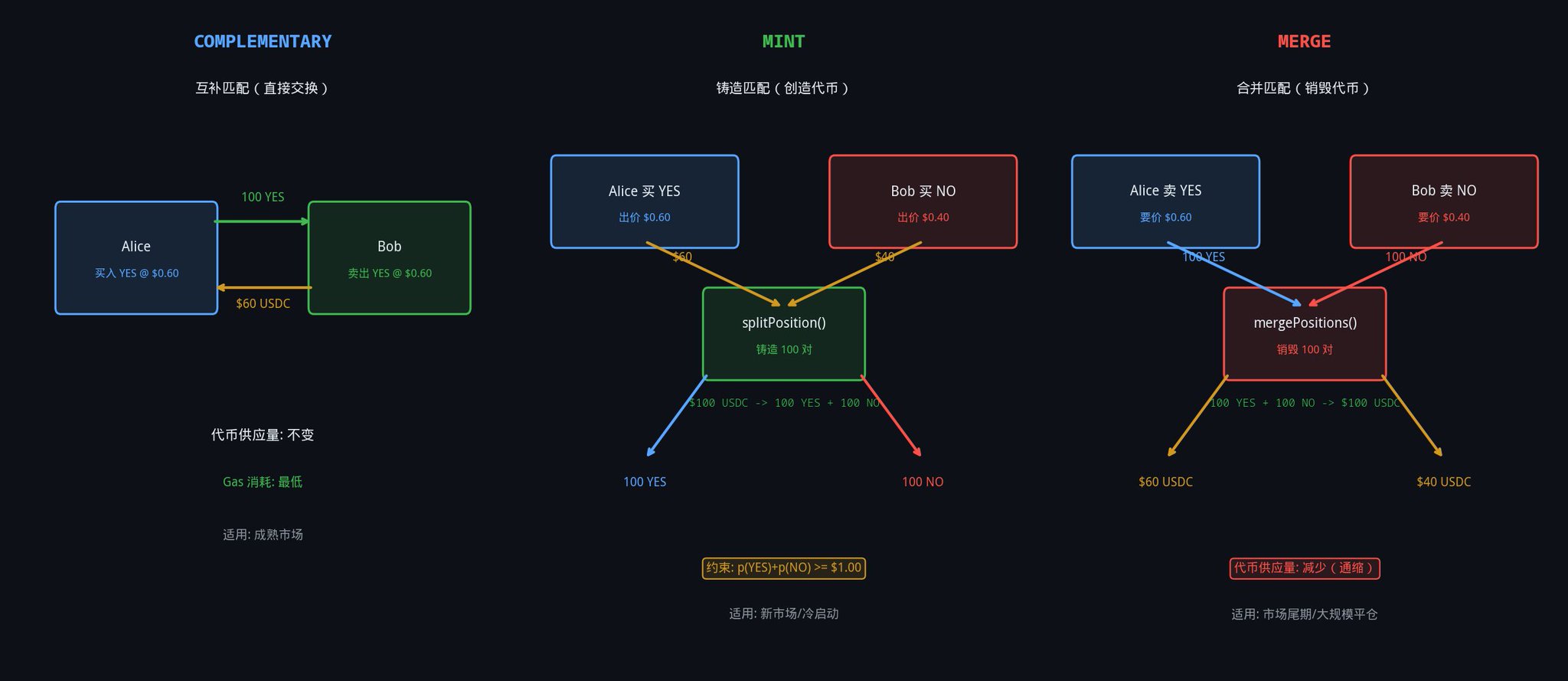

When you dive into the source code of ctf-exchange-v2, you will find three fundamentally different asset settlement paths at the core: COMPLEMENTARY, MINT, and MERGE.

3.1 COMPLEMENTARY: Traditional Off-chain Trade

This is the most straightforward matching mechanism and the only one that traditional trading platforms have.

Scenario: The market has been around for some time, and everyone holds chips.

· Alice wants to buy 100 YES at $0.60.

· Bob has YES and wants to sell 100 YES at $0.60.

The operator spots these two orders (BUY vs. SELL) and batches them on-chain. The smart contract executes a direct peer-to-peer transfer:

· Transfers 100 YES from Bob's address to Alice.

· Transfers $60 pUSD from Alice's address to Bob.

This mechanism has the following mathematical and engineering characteristics:

· Zero-Sum Game: The total token supply of the system remains unchanged.

· Minimal Gas Consumption: Involves only basic transfers, excluding the complex CTF operations.

· Standardization: In a mature, highly liquid market, the vast majority of daily transactions occur this way.

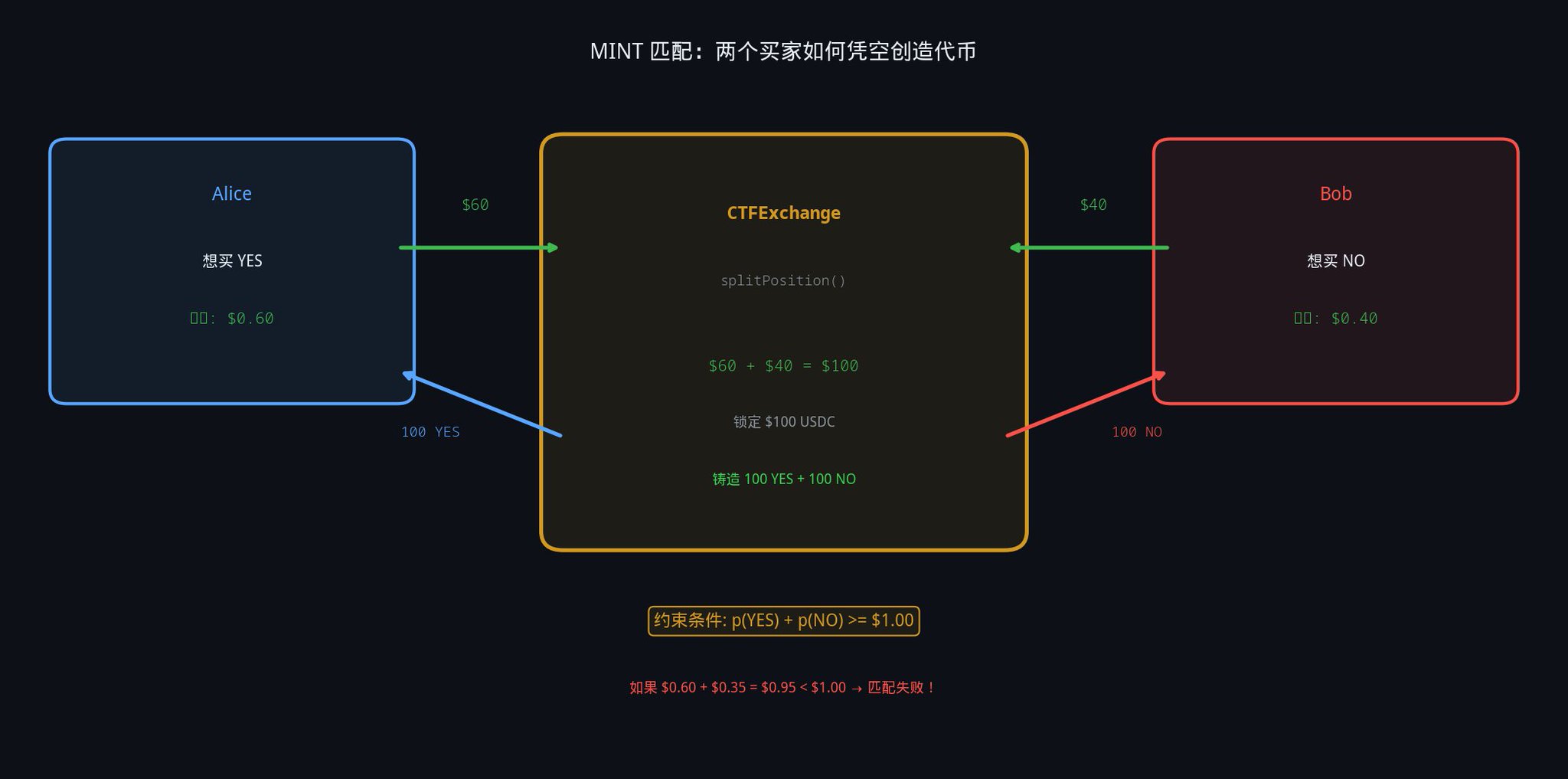

3.2 MINT (Minting Match): Creating Liquidity Out of Thin Air

This may be the most revolutionary innovation in Polymarket, and perhaps in all of financial history.

To better explain, we can refer to this scenario: A brand new market has just launched, with no one holding any YES or NO tokens.

· Alice is extremely bullish and wants to buy 100 YES at $0.60 each.

· Bob is extremely bearish and wants to buy 100 NO at $0.40 each.

Note:

· They are both buyers!

· They both do not have the tokens the other wants!

· In a traditional order book, these two orders would just sit there, never able to be matched.

In Polymarket, if a BUY vs. BUY situation (with complementary tokens) occurs, the Operator will match these two orders together!

1. The smart contract deducts $60 pUSD from Alice's account.

2. The smart contract deducts $40 pUSD from Bob's account.

3. The smart contract takes this $100 pUSD, locks it as collateral, and then calls the _mint function to create out of thin air 100 YES and 100 NO tokens.

4. Sends 100 YES to Alice.

5. Sends 100 NO to Bob.

For this mechanism to trigger, it must be based on a strict mathematical condition: The sum of the buyers' bids must be greater than or equal to $1.00.

If Alice bids $0.60 for YES and Bob bids $0.35 for NO, totaling only $0.95, the smart contract cannot mint a full token pair worth $1.00. This matching will fail outright.

From the perspective of a liquidity provider, this mechanism is the ultimate weapon to solve the "cold start" issue.

When the market has just opened, liquidity providers do not need to spend money to mint a bunch of tokens to hold (which would tie up a significant amount of capital). They only need to place buy orders on both YES and NO sides simultaneously (e.g., $0.49 to buy YES, $0.49 to buy NO). When retail traders come to sell, it triggers the minting logic.

3.3 MERGE: Liquidity Annihilation

With creation comes destruction. MERGE is the reverse process of MINT.

Let's consider a reverse scenario. As the market is about to close, everyone is unwinding their positions.

· Alice holds 100 YES and wants to sell at $0.60.

· Bob holds 100 NO and wants to sell at $0.40.

Notice: Both of them are sellers! There is no one willing to offer pUSD to buy their tokens.

It's at this moment that Polymarket's mechanism kicks in again. When faced with a SELL vs. SELL situation, the Operator works its magic once more:

1. The smart contract takes 100 YES from Alice.

2. The smart contract takes 100 NO from Bob.

3. The smart contract calls the _merge function, completely destroying these 100 pairs of YES+NO and unlocks $100 pUSD from the treasury.

4. Sends $60 pUSD to Alice.

5. Sends $40 pUSD to Bob.

The Merge mechanism exhibits the following mathematical and financial characteristics:

· Deflationary Mechanism: The total token supply of the system is reduced.

· Exit Channel: It ensures that even without a liquidity provider, as long as the YES and NO seller prices add up to $1.00 (actually leaving $1.00 of room), everyone can still cash out and exit.

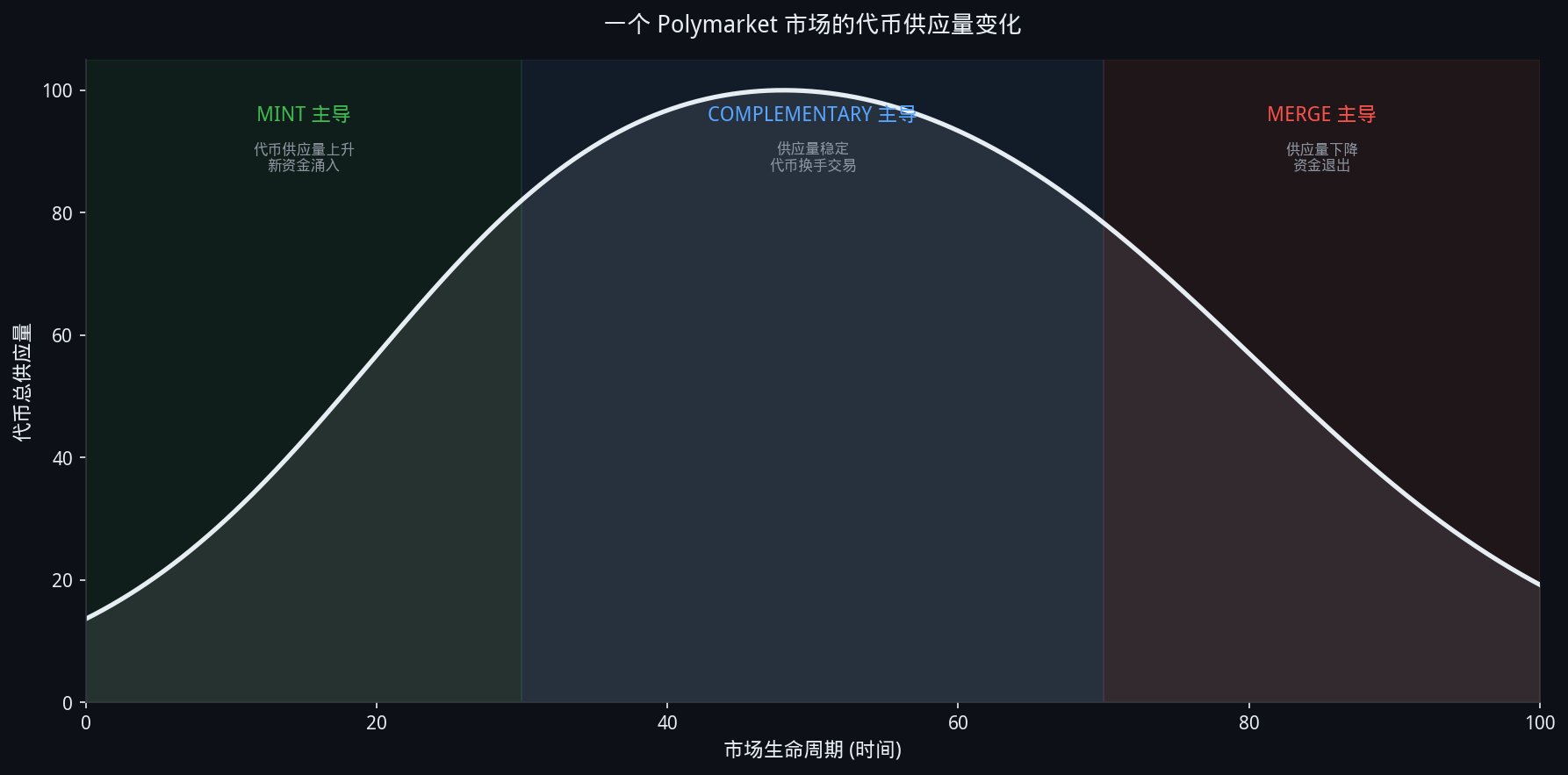

Understanding these three matching mechanisms, you understand the Polymarket market lifecycle:

1. Early Stage (MINT Dominant): The market has just launched, with no tokens. Both long and short sides continuously inject funds into the system through the MINT mechanism in exchange for tokens. The total supply rapidly increases.

2. Mid Stage (COMPLEMENTARY Dominant): The market has sufficient liquidity, and most trades involve turnover of existing tokens. The total supply stabilizes.

3. Late Stage (MERGE Dominant): The outcome becomes clear, and people start to close out their positions. Both long and short sides burn tokens through the MERGE mechanism, exchanging them back for funds. The total supply decreases.

It is important to note that these three paths are not subjectively chosen by the Operator but are strictly determined by the direction of orders (BUY vs SELL) through intelligent contract routing rules.

Chapter 4: Split/Merge/Redeem, and Why Your PnL Is Wrong

Having understood the matching mechanisms, let's now look at three fundamental operations you may be using every day but have never truly understood their financial implications: Split, Merge, and Redeem.

These three operations are atomic operations on Polymarket. They are not "trades" (they do not go through an order book, and no fees are charged) but are direct asset exchanges that interact with smart contracts.

1. Split: You provide the contract with $1 pUSD, and the contract gives you 1 YES and 1 NO. The cost is always exactly $1

2. Merge: You provide the contract with 1 YES and 1 NO, and the contract returns $1 pUSD to you. The proceeds are always exactly $1

3. Redeem: After the market determines the winner, the winning token is redeemed for $1 pUSD, and the losing token is zeroed.

4.1 Who Uses These Operations?

Market Makers: They are the biggest users of Split. Market makers need to place orders on both sides simultaneously, but they do not want to buy tokens on the market (which would incur fees). They directly split $100,000 into 100,000 YES and 100,000 NO, and then place them on the order book.

Arbitrageurs: They are the biggest users of Merge. When there is a brief mispricing in the market, such as YES falling to $0.40 and NO falling to $0.55, arbitrageurs will quickly buy 1 YES and 1 NO (total cost $0.95), then immediately call Merge to convert back to $1, making a risk-free net profit of $0.05. The mathematical condition for this is very clear: when Price(YES) + Price(NO) < 1 - Fee, blindly buy and Merge.

Therefore, when you are trying to follow the smart money of an arbitrageur or market maker, you must accurately assess the impact of Split/Merge on PNL. Otherwise, this is not a referenceable "smart money."

And in today's market, including Polymarket itself, none can solve the PNL calculation issue.

Of course, you may have already guessed - insiders.bot has already solved this problem in PNL calculation and smart money browsing.

4.2 PnL Trap: Why Your Profit Is Wrong?

As mentioned above, this is the most common mistake throughout the entire Polymarket ecosystem. Almost all third-party PnL (Profit and Loss) tracking tools, including some official APIs, have stumbled here.

Let me walk you through an example to show you how deep this trap is.

· Step 0: Suppose you have $100 in capital. You are bullish on the "Ethereum Breaks $5000" market.

· Step 1: You spent $50 to execute a Split. Now you have 50 YES and 50 NO. You have $50 in cash remaining.

· Step 2: Feeling that 50 YES is not enough, you went back to the market and bought another 50 YES at a price of $0.40. You spent $20. Cash remaining is $30.

· Step 3: You sold the 50 NO at a price of $0.35. You received $17.50. Cash is now $47.50.

Now, you hold 100 YES contracts. What is your actual cost?

How most leaderboards calculate (incorrect algorithm):

· They only look at your "trade" records. They see that you bought 50 YES, spending $20. They completely ignore the Split (because that is not a trade).

· So they believe your cost is: $20 / 50 = $0.40 per unit.

· If the market price of YES now rises to $0.60, they will show your profit as: 100 × $0.60 - $20 = $40.

How you should actually calculate (correct algorithm, and the one insiders.bot is using):

· Your total cash outflow: $50 (Split) + $20 (Purchase) = $70

· Your Total Cash Inflow: $17.50 (Selling NO)

· Your Net Investment: $70 - $17.50 = $52.50

· Your True Cost: $52.50 / 100 = $0.525 each

· If the current YES market price is $0.60, your actual profit is: 100 × $0.60 - $52.50 = $7.50

See the difference? The leaderboard shows you made $40, but you actually only made $7.50. The $32.50 in the middle, the "illusory profit," is because the system did not properly handle the cost of Split and the revenue from selling NO.

The correct PnL mathematical formula should be:

Total PnL = Σ(Sell Revenue) + Σ(Merge Revenue) + Σ(Redeem Revenue) - Σ(Buy Expenditure) - Σ(Split Expenditure) + Current Position Market Value

That's why you see some whales on the leaderboard showing losses of millions, but in reality, they are making a killing. When the winning positions are Redeemed, many tools will "wipe out" these holdings from the historical records, leaving behind only those positions that are still in the red.

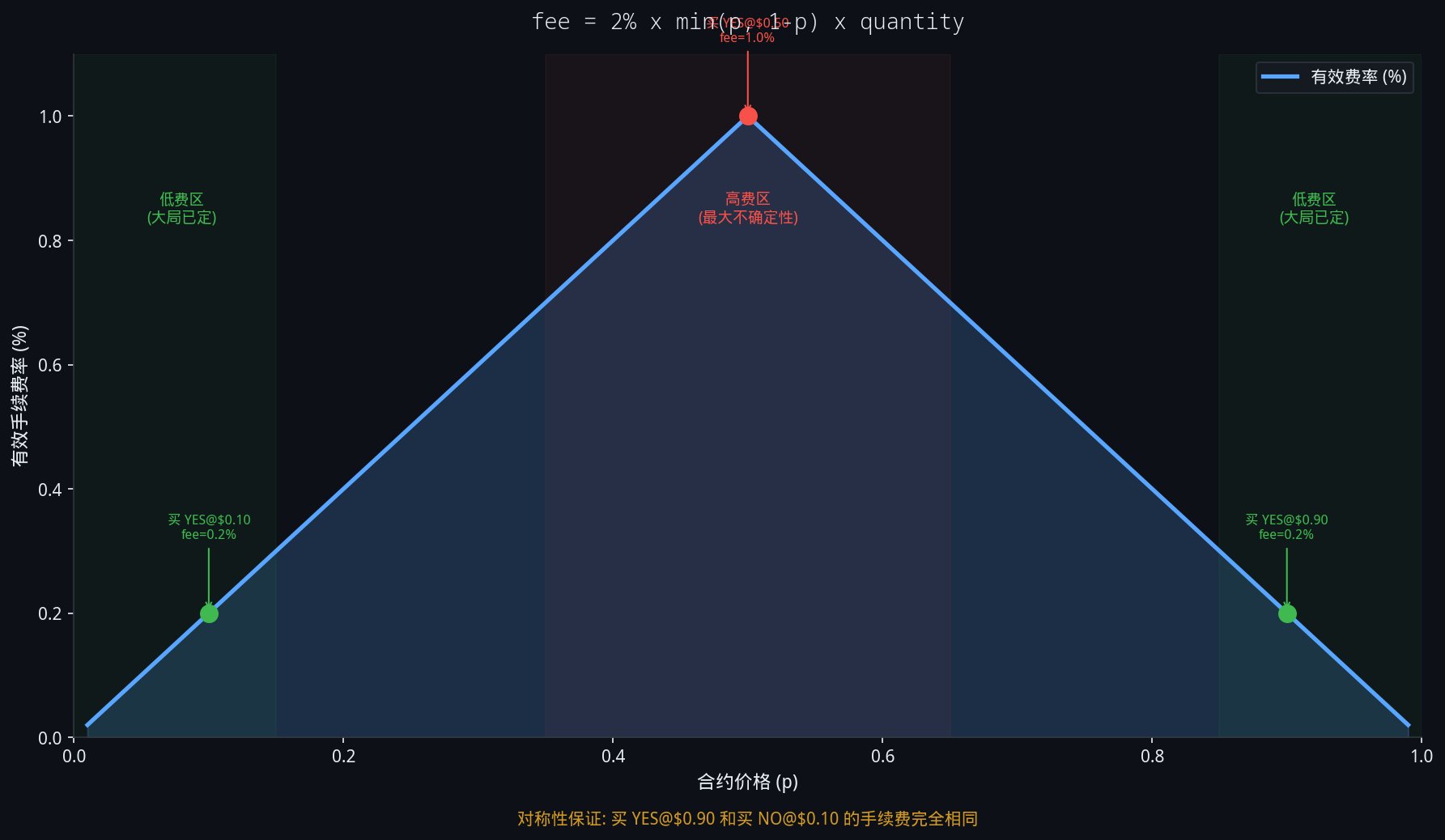

Chapter 5: Fee Curve

If you trade frequently, you will notice that Polymarket's fees are not a fixed percentage. Sometimes you are charged $10 for a $1000 contract, and other times only $2.

Why? Let's take a look at the fee formula hidden in the code:

Fee = C × feeRate × p × (1 - p) (where C is the transaction quantity, and p is the price)

5.1 Why p(1-p)?

Suppose you want to buy 100 YES, with a fee rate of 2%:

· If the price of YES is $0.50: Fee = 100 × 2% × 0.50 × 0.50 = $0.50.

· If the price of YES is $0.90: Fee = 100 × 2% × 0.90 × 0.10 = $0.18.

· If the price of YES is $0.10: Fee = 100 × 2% × 0.10 × 0.90 = $0.18.

Do you see the pattern? When the price is at 0.50 (even odds), the fee is highest. When the price is close to 0 or 1 (near certainty), the fee is minimal.

More importantly, symmetry. Buying YES at $0.90 is mathematically equivalent to buying NO at $0.10. If buying YES at $0.90 incurs a high fee while buying NO at $0.10 incurs a low fee, arbitrageurs would aggressively buy NO and then arbitrage through the MINT mechanism. This design of p(1-p) ensures that regardless of which side of the bet you take, the system's friction cost is absolutely symmetrical.

5.2 The Hidden Beauty of Mathematics

If you've studied statistics, you'll be very familiar with the p(1-p) formula. It is the variance formula of the Bernoulli distribution (flipping a coin).

Throughout Polymarket's system design, p(1-p) is the "God's Formula":

1. It is the Fee Curve: The higher the uncertainty (variance), the higher the fee the system charges.

2. It Represents Information Entropy: When you bet at 50%, you provide the most new information to the market, so you pay the highest cost.

Who pays the fee? Always the Taker. Makers are always fee-free.

This mechanism perfectly aligns incentives: at the most uncertain point of the market (50/50), early entrants will face the highest fees, protecting liquidity providers from unnecessary slippage; while in a market that is almost certain, very low fees encourage arbitrageurs to enter, driving the price to its final 1 or 0.

Chapter 6: Negative Risk, a.k.a. the Most Elegant Magic in the DeFi Space

If you have traded on Polymarket in multi-outcome markets such as elections, Oscars, or sports events, you have encountered Negative Risk markets.

This is the most mind-bending part of the entire article, but also the one that best exemplifies the aesthetic of smart contract engineering.

P.S. This is also the part that our co-founder @DakshBigShit tackled during a 36-hour hackathon to develop our own API.

6.1 Pain Points of Traditional Multi-Outcome Markets

Let's say there are four candidates: A, B, C, D. You strongly dislike A and are certain that A will never win. You want to "short" A.

In a traditional binary market, you only need to buy the NO contract for A. But in a multi-outcome market, if A loses, it means that one of B, C, or D will definitely win. Therefore, "shorting A" is mathematically equivalent to "backing B + backing C + backing D". (This sentence is crucial; read it repeatedly until you understand it.)

If you were to separately buy YES contracts for B, C, and D on the market, you would encounter a major issue: extremely low capital efficiency. Because you would need to front three separate amounts of money, and if the prices of these three individuals add up to more than $1.00, you might even end up losing money.

6.2 The Magic of the Negative Risk Adapter

Polymarket has deployed a dedicated smart contract called the NegRiskAdapter to address this issue. It provides a function called convertPositions.

The function of this function is: to instantly convert your NO contract for a specific candidate into YES contracts for all other candidates, and refund you with some cash.

Let's use hardcore math to prove why this conversion is value-preserving.

Scenario: There are n candidates.

· You have A NO contracts for candidate 1, and A NO contracts for candidate 2 (you are shorting both 1 and 2) in your hand.

· You hold a total of m different NO contracts (here m=2).

Before the conversion, the true value of your position (across all possible timelines):

· If candidate 1 wins: NO_1 becomes worthless, NO_2 is worth $1. Total value = A.

· If candidate 2 wins: NO_1 is worth $1, NO_2 becomes worthless. Total value = A.

· If candidate 3 wins (the candidate you did not short): NO_1 is worth $1, NO_2 is worth $1. Total value = 2A.

After calling convertPositions, what did the contract give you?

· The formula is: refund you with A × (m-1) in cash, plus A YES contracts for candidates 3, 4, … n.

· In this example, you are refunded: A × (2-1) = A in cash! Plus A YES for candidate 3, A YES for candidate 4…

After the conversion, the true value of your position (across all possible timelines):

1. If candidate 1 wins: Your YES_3, YES_4 contracts all become worthless. You only have cash A left. Total value = A. (Same as before the conversion!)

2. If Candidate 2 Wins: Your YES_3, YES_4 positions become worthless. You are left with only cash A. Total Value = A. (Same as before the conversion!)

3. If Candidate 3 Wins: Your YES_3 position is worth $1, the rest become worthless. You add this to cash A. Total Value = A + A = 2A. (Same as before the conversion!)

Q.E.D. No matter how the world changes, the value remains exactly the same before and after the conversion.

6.3 Why Is This a "One-Way Irreversible" Entropy-Increasing Process?

This conversion mechanism has an incredibly fascinating physical property: It is one-way irreversible.

You can convert NO to YES + cash. But you can never convert YES + cash back to NO.

· Why? Because at the smart contract level, when you convert NO to YES, the contract effectively sends your NO contract to a black hole address (Burn Destroy), and then uses the released collateral space to "mint" a new YES contract. This does not require injecting new external funds.

· However, if you want to reverse it, turning YES into NO, you would need to create new collateral out of thin air (since the NO contract has a much broader coverage than YES). The adapter does not have the authority to tap into the treasury funds.

· It's like breaking an egg. NO is the intact egg, containing all possibilities. The conversion process breaks the egg into yolk (YES) and egg white (cash). The value is conserved throughout the process, but you can never put them back together into a whole egg.

There is a huge arbitrage opportunity here: If you find that the NO price of a certain candidate in the market is greater than the sum of all other candidates' YES prices, you can buy this NO, call convertPositions to receive cash and a bunch of YES, and then immediately sell these YES. This is the most advanced risk-free arbitrage strategy in a multi-outcome market.

Chapter 7: The Physical Limit of Speed

Finally, let's talk about the most brutal dimension of transactions: time.

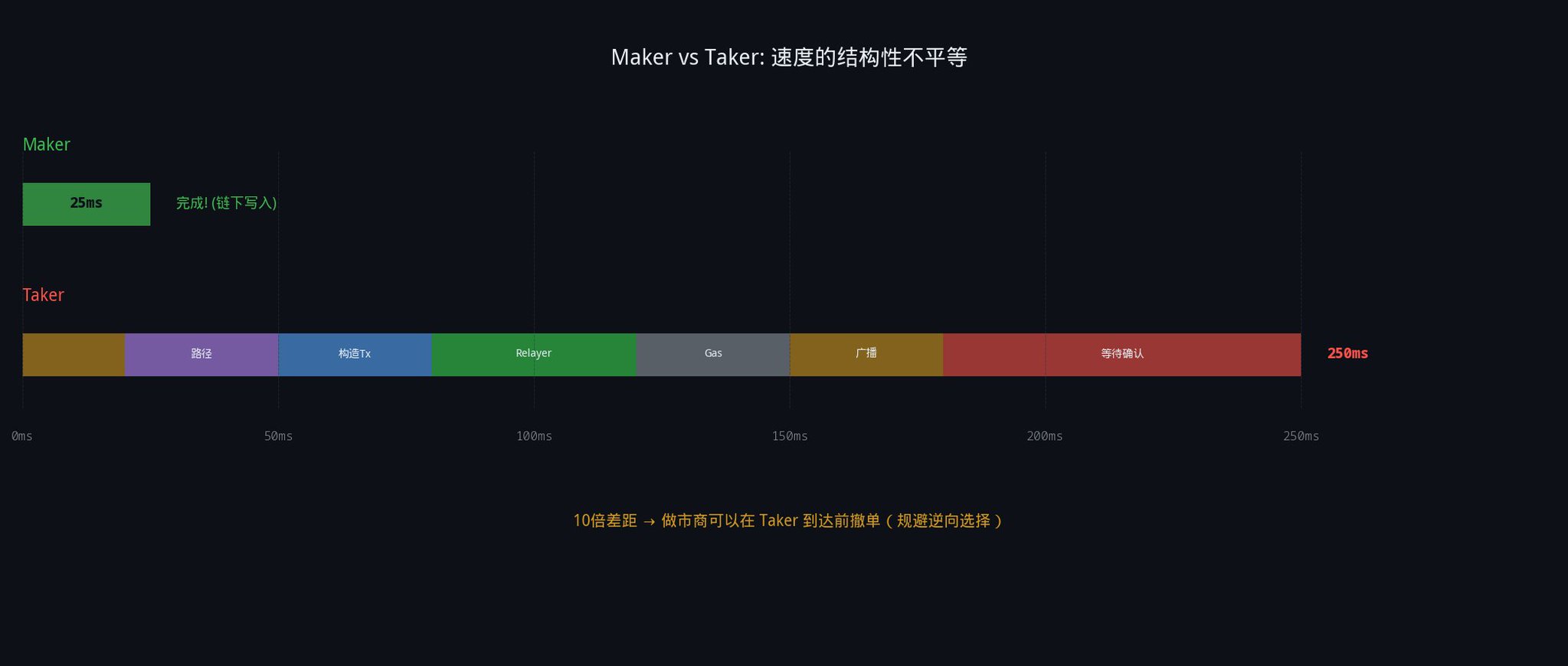

In traditional high-frequency trading, we are talking about microseconds (one millionth of a second). At Polymarket, we are talking about milliseconds. But here lies a huge, structural inequality.

If you've ever frequented Reddit's algorithmic trading forums, you'll find that all programmers developing Polymarket bots have complained about the same thing: "Why do I always have to wait 300 milliseconds to place a Taker order, while a Maker order only takes 25 milliseconds?"

7.1 Why is Maker Fast and Taker Slow?

When you place a Maker (Limit) order: Your order (signed data) is sent to Polymarket's server. The server quickly checks the validity of the signature, directly inserts this record into the in-memory Central Limit Order Book (CLOB) database, and promptly returns you an ACK (acknowledgment). The entire process occurs completely off-chain, requiring just one database write. Time taken: ~25 milliseconds.

When you place a Taker (Market) order: Your order is sent to the server. The matching engine finds that your order can match with a Maker order in the order book. At this point, the Operator must initiate a complex settlement pipeline:

1. Decide on which matching path to use (COMPLEMENTARY, MINT, or MERGE).

2. Construct on-chain transaction data containing signatures from both parties.

3. Send the transaction to the Relayer.

4. Relayer estimates Gas, assigns Nonce.

5. Broadcast the transaction to Polygon nodes.

6. Wait for node confirmation that this transaction will not Revert due to reasons like insufficient balance.

This entire process spans across multiple microservices, even touching the edges of the blockchain. Time taken: ~250 to 300 milliseconds.

7.2 What Does This 250 Milliseconds Mean?

This 250-millisecond physical chasm has profoundly shaped the Polymarket ecosystem.

First, Front-running on Polymarket is Hard. Because all Taker orders must queue up for the Operator to process, you cannot skip the line by raising the Gas fee. Mempool front-running is currently a moot point here.

Second, Maker Strategy's Absolute Edge. Because cancellation, like Maker orders, is an off-chain operation, it only takes 25 milliseconds. When breaking news occurs, savvy market makers can take advantage of this 250-millisecond time gap to cancel their orders before the Taker's order is settled (this is called Adverse Selection avoidance).

7.3 The 90-Second Downtime Every Tuesday Morning

Speaking of time, there is another little-known detail. According to the official documentation, every Tuesday at 7:00 am Eastern Time, Polymarket's matching engine undergoes a restart. During this approximately 90-second period, the system stops processing any matches, and the API returns an HTTP 425 (Too Early) error.

What's more brutal is that V2 introduced a Heartbeat mechanism. If the server does not receive a heartbeat from the client within 10 seconds, all of that user's open orders will be automatically canceled. During this 90-second restart, market makers' heartbeats are forcibly interrupted, and their orders are collectively cleared by the system.

This 90 seconds represents a true "liquidity vacuum" in the system. For options pricing models, how to value the Theta (time decay) of these 90 seconds and how to preempt the order book as soon as the engine resumes in the 91st second pose the ultimate puzzle left to top-tier platforms and quant shops.

Chapter 8: V2's Large-Scale Refactoring and the Ultimate Battle of "Ghost Fills"

If you've read this far, you've already grasped the core framework of Polymarket. But if you want to continue making money on this market in 2026, you must understand the recent earthquake that just occurred.

During the period from February to May 2026, Polymarket quietly underwent an epic V2 architecture upgrade. This upgrade not only refactored the collateral and fee formulas, but more importantly, it launched a decisive battle to solve the most notorious bug in the prediction market, known as Ghost Fill.

8.1 What is Ghost Fill? On-chain vs. off-chain state divergence

Prior to the Polymarket V2 upgrade, countless market makers and quant bots were tormented by a phenomenon: your bot identified a perfect opportunity in a 5-minute candle level market (such as BTC Up/Down 5m), immediately sent a market order (Taker).

Polymarket's API instantly responded: "Matched! Success!" Your Telegram alert also popped up with a "FILLED" celebration. However, when you checked Polygonscan on the blockchain browser, you found that the transaction was labeled as REVERTED (failed), wasting gas fees. And your position remained unchanged.

Although the order book showed a fill, the blockchain claimed otherwise. This is what Ghost Fill is all about.

To understand the essence of this bug, we need to revisit the underlying architecture mentioned in the first chapter: Off-chain Matching + On-chain Settlement.

When Alice's buy order and Bob's sell order match in the off-chain central limit order book (CLOB), the system merely equates these two orders in the database. The actual asset transfer requires the Operator to bundle both parties' signatures, submit them to the Polygon chain, and execute a TransferFrom.

This creates a fatal time discrepancy. During this time gap, the user's wallet state may change.

8.2 Two Attack Paths of Flashbots

During the early days of V1 and V2, hackers and malicious actors took advantage of this time differential and invented two highly destructive attack methods:

First Attack: Low-cost incrementNonce Attack (V1 Era) In the V1 architecture, order state was managed by a global nonce (random number). Malicious actors could aggressively place highly attractive fake orders off-chain (Spoofing). When a real buyer took the bait and the order was displayed as matched off-chain, the malicious actor would preemptively call the incrementNonce function on-chain before the Operator submitted it.

This operation cost was extremely low (a few cents Gas), yet it instantaneously invalidated all old nonce orders under that address. When the Operator submitted the matched transaction on-chain, the smart contract realized the nonce was incorrect and directly Reverted. The attacker escaped unscathed, while the real buyer not only missed the trading opportunity but could also be misled by false order books.

Second Attack: Empty-wallet "Zombie Orders" (Early V2) The V2 upgrade removed the global nonce and used a single order Hash to manage the cancellation state, blocking the first attack path. However, hackers quickly discovered a more fundamental loophole: Balance Deception. A malicious user could deposit $1000 into a wallet, sign a bunch of $10,000-worth orders placed on the order book, and then immediately transfer out all the money in the wallet.

Since Polymarket's orders are offline signed, as long as the signature is valid and the token approval is not revoked, these orders appear "legitimate" to the off-chain matching engine. However, in reality, this wallet has a balance of $0.

When your bot takes these "zombie orders," and the Operator submits them on-chain, the underlying Solady library function TransferFrom will error out due to insufficient balance on the other side (error code 0x7939f424). Your transaction will Revert once again.

8.3 Why Don't Traditional Trading Platforms Have This Issue?

You might ask: Why don't Binance or traditional decentralized exchanges (such as Uniswap) have this problem?

Because Binance is fully centralized, your funds are stored in its database, giving it absolute control. Matching and deductions occur atomically at the same time. In contrast, Uniswap is fully on-chain, where matching and deductions happen in the same transaction within a smart contract, also atomically.

Polymarket, however, has opted for a hybrid approach: off-chain matching for speed and on-chain settlement for transparency. Users' funds are held in fully self-custodial wallets (such as EOA or Gnosis Safe), where users have absolute control and can withdraw their funds anytime, anywhere.

As long as the fund status of both matching parties is tied to the user's truly free self-custodial wallet, "state separation" will always exist.

8.4 Ultimate Solution: Deposit Wallet

On May 4, 2026, Polymarket officially announced a major protocol-level update, significantly reducing the occurrence of front-running from its peak of 30% to 0.17%, approaching zero.

How did they achieve this?

The answer lies in the introduction of Deposit Wallet.

Polymarket finally realized that the fundamental solution to front-running is to restrict the "absolute freedom" of user funds. In the new architecture, users can no longer directly participate in off-chain matching with their native wallets (EOA). You must first deposit your funds into a Deposit Wallet controlled by a smart contract.

In this vault:

1. You have ownership but not absolute immediate control.

2. When you place an off-chain order, the vault logically locks the corresponding available balance.

3. If you wish to withdraw funds from the vault, this withdrawal operation (State Revocation) itself incurs a physical time cost. It must pass the smart contract verification to ensure you have no pending orders being matched.

By introducing this buffer layer, Polymarket forcefully binds the off-chain matching state with the on-chain fund state, completely eliminating the possibility of "empty wallet orders." This is not only an engineering triumph but also a profound compromise and restructuring of the contradiction between "self-custody" and "transaction efficiency" in decentralized finance.

8.5 V2 Other Hardcore Upgrades

In addition to the ultimate solution of Ghost Fill, the V2 architecture also includes several upgrades that have profoundly reshaped the market:

· pUSD Power Handoff On April 28, the underlying collateral fully transitioned from USDC.e to pUSD. This gave Polymarket control over the underlying asset's interest, allowing them to offer users up to a 4.00% APY holding reward. pUSD has become the new capital-efficient infrastructure.

· Implementation of the Perfect p(1-p) Formula Abandoning the rough min(p, 1-p) approximation from the V1 era, the fee formula was directly modified to the perfect Bernoulli variance formula p × (1-p). Mathematically smooth, this has made arbitrage pricing models more precise.

· Removal of Artificial Speed Bump In the early days, a hardcoded Taker delay of up to 500 milliseconds protected liquidity providers from API bot attacks. With the performance boost of the V2 engine and the introduction of the Heartbeat mechanism (orders cleared after 10 seconds of disconnection), the team completely removed this artificial speed bump at the end of February, officially ushering Polymarket into the realm of microsecond HFT (High-Frequency Trading) battles. (This is also why our insiders.bot is preparing to open-source its API in the near future to join this battle.)

Conclusion: Understanding the Machine from Ground Zero

From the moment you clicked to place your order:

· Your signature was sent to the off-chain order book.

· The Relayer burned its Gas to pave the way for you.

· The Operator searched for the optimal matching path for you in COMPLEMENTARY, MINT, and MERGE.

· The Fee Curve elegantly siphoned off tiny friction costs using the p(1-p) formula.

· If your operation is complex, NegRiskAdapter may even perform alchemy for you following the principles of conservation of matter.

· In the end, everything is settled within those 250 milliseconds that determine life or death. (This is why insiders.bot considers transparency and speed in mirroring orders crucial)

Your money has not disappeared. It is simply following the physical laws of the precise machine named ctf-exchange-v2, flowing to where it needs to be.

Next time you see an outrageous odds on Polymarket or a tempting arbitrage opportunity, don't rush to click Buy. First, visualize the gears of this machine in your mind.

With a grasp of these foundational "laws," coupled with the right "way," you will surely be invincible.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia