The sharp decline in chip stocks this time was not caused by South Korea's "small composition," but rather the inevitable liquidation in the AI sector due to extreme overcrowding and fragile leverage. Analysts from Goldman Sachs and others believe that the AI narrative has not changed, and the sell-off is concentrated among crowded longs, more resembling a "technical pullback." However, with rising rate hike expectations and 65% of companies in a buyback blackout period, multiple pressures have been accumulating, and there is no clear boundary between the correction and mid-term risks.

On Tuesday, June 23, global chip stocks were caught off guard by South Korea. A Wall Street strategist referred to this sudden drop as a "chip-wreck."

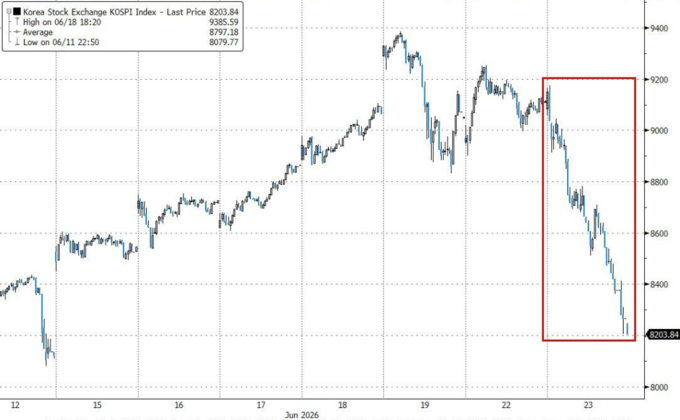

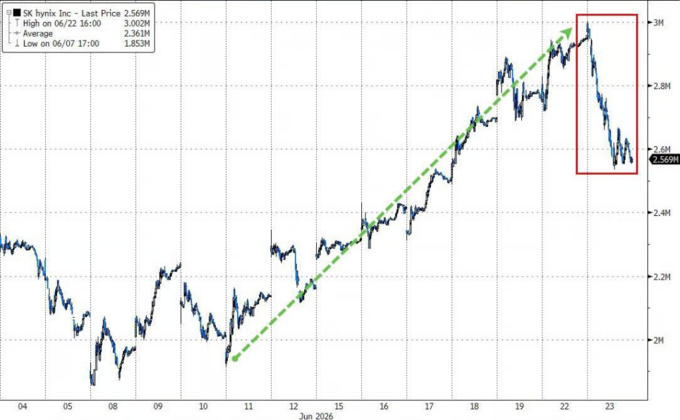

The first to collapse was this year's "world's hottest stock market" - South Korea. The KOSPI index in South Korea plummeted 10% in a single day, triggering multiple circuit breakers, with SK Hynix and Samsung Electronics both falling more than 10%.

Several catalysts ignited this storm: Korean media reported that NVIDIA's Rubin expected production cuts, SK Hynix was slowing down the expansion of storage chips (HBM4) and shifting to cheaper regular DRAM; secondly, the Korean news agency reported that bipartisan lawmakers in Korea are discussing taxing unrealized gains on assets such as stocks and real estate - that is, even if the paper gains have not been realized, they would still be taxed.

This "chip earthquake" quickly spread to the U.S. stock market.

Overnight, the Philadelphia Semiconductor Index (SOX) fell 7.9% in a single day, with all 30 component stocks falling across the board. Micron Technology fell 13% - prior to Tuesday, it had already risen over 300% this year, making it the strongest component stock in the Philadelphia Semiconductor Index for the year. Micron, NVIDIA, and AMD, the three stocks, contributed to about 50% of the S&P 500's decline. The Nasdaq fell 3.3%, the Dow only fell 0.1%, and the S&P 500 fell 1.4%.

Jonathan Krinsky, Chief Market Technician at BTIG LLC, stated: "Regardless of whether there is a short-term rebound, we still believe that there is mid-term downside risk in the technology/artificial intelligence sector." He believes that the semiconductor sector still has 10% to 15% downside potential, and described Tuesday's market as a "Chip-Wreck."

However, Goldman Sachs Global Banking & Markets TMT sector expert Peter Callahan wrote in a flash note on June 24: "Today's discussions with investors mainly revolve around 'what are you seeing on your end,' rather than signs of a broader narrative shift." This statement is key. It sets a boundary for this round of sell-off: the tape is ugly, but at least for the day, there hasn't been a full-scale abandonment of AI trading.

So the issue is not as simple as "a Korean essay triggering a global AI bull market crash." It's more like a sector that was already overextended, heavily crowded with trades, and not low on leverage, collectively de-risking after a trigger. In the short term, there are indeed characteristics of a "technical correction"; in the medium term, the vulnerability of AI trading has not disappeared.

This is a contagion, not an accident

While Korea's plunge may seem sudden, the logic behind it is not complex.

The news of SK Hynix's slowed expansion of HBM4 production triggered the collapse of SK Hynix, a stock whose weight in the Korean stock market is similar to Apple's weight in the Nasdaq—too big in size that once it falters, the entire index cannot withstand it. More importantly, Korean retail investors extensively use leverage ETFs to participate in AI/semiconductor trading. These products are automatically sold off in a market decline to maintain leverage ratios, leading to mechanical selling.

The news itself was the trigger, but the leverage structure was the explosive. At the same time, some market observers are asking, "Will Korean leveraged retail investors be the terminator of the U.S. tech bull market?"

Of course, this question is somewhat exaggerated, but it points to a real vulnerability: AI/semiconductor trading is highly concentrated, global investor positions are highly similar, and any sell-off at a single node could potentially transmit along this chain.

According to Goldman's after-hours data, both long and short sides were selling on that day: Long-only funds (LO) sold with a skew of -18%, hedge funds (HF) similarly continued selling throughout the day, with shorts accounting for 60% of sales volume (recent average around 50%). The selling scale of both types of institutions exceeded $1 billion in notional exposure.

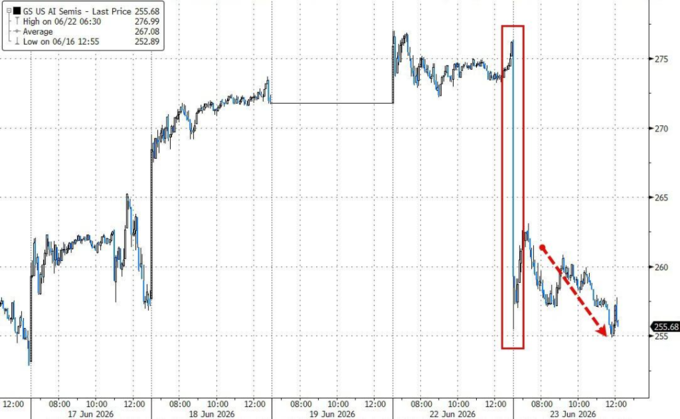

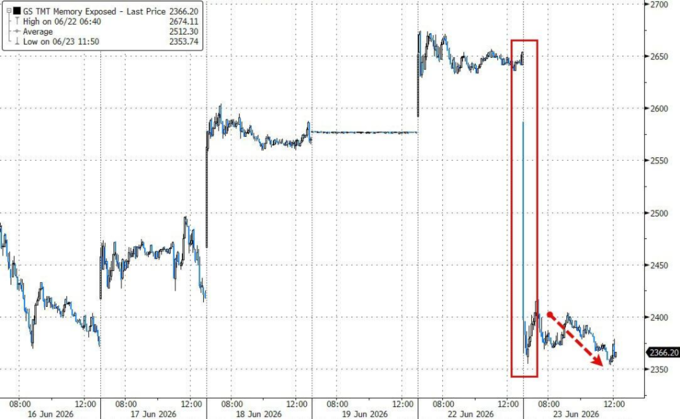

The hardest-hit in the U.S. stock market were those "crowded longs," the batch of stocks that "made the most money this year": the Goldman storage stock basket (GSTMTMEM) fell 10%, the AI semiconductor basket (GSCBSMHX) fell 620 basis points, the AI stock basket (GSTMTAIP) fell 440 basis points, and the high flyer basket in the past 12 months (GSXHUHMOM) fell 420 basis points.

Technical Adjustment? Goldman Sachs: The Narrative Has Not Changed

After such a steep decline, how is the market interpreting the situation? If we only consider the magnitude of the drop, Tuesday seemed like a repricing of AI trades. However, when we look at the trading volume and fund flows, the conclusion is not so absolute.

Goldman Sachs' TMT trading desk expert Peter Callahan wrote in the after-hours note that the feeling of the day can be summed up in one word: "orderly" — despite the significant drop, the overall Nasdaq trading volume was essentially in line with the 20-day average, and the cash and volatility trading desks were operating normally.

More importantly, he described the conversations with investors that day: "Today's exchanges with investors largely revolved around 'how are things on your end,' with no signs of a broader narrative logic shift and no increase in inquiries about 'new targets' or 'laggards.'

In other words, no one is reallocating their holdings, no one is seeking new investment directions. Everyone is just exchanging information."

Goldman's another market strategist, Chris Hussey, provided specific data support: of the 12 tech stocks that fell more than 8% today, all except one are still up by double digits for the year, with most having already more than doubled. His assessment is:

"Today's sell-off is more akin to 'popping the bubble' on a period of frenzied stock price appreciation rather than a fundamental reassessment of AI infrastructure trades. Investors are not selling off the index as a whole but are reevaluating: for those stocks that have doubled in the last six months, how much should they really be worth?"

Natixis Advisors Fund Manager Jack Janasiewicz's assessment is similar:

"It appears more like a technical sell-off rather than anything else. The market breadth was decent after the opening, despite many large red figures — a sign of a narrow sell-off." He also cautioned, "When we see such significant crowding in beta and momentum, it can easily lead to an unsightly deleveraging event."

The Other Side of "Technical Adjustment": Structural Risks That Cannot Be Ignored

The term "technical adjustment" may sound reassuring, as it can explain everything, but it may also mask the real risks. The market indeed displayed technical characteristics that day: the decline was concentrated in the winners, trading did not spiral out of control, and investor communication did not immediately shift the AI narrative. However, there is no clear barrier between a technical adjustment and structural risk — if the former is severe enough, it could easily evolve into the latter.

There are several key background numbers worth looking at together.

First, Too Rapid a Rise. The Nasdaq has surged over 30% from the end of March to the present. In just June, the Philadelphia Semiconductor Index had 8 trading days (out of 16 trading days) with a single-day volatility exceeding ±5%—meaning that on half of June's trading days, semiconductor stocks experienced significant fluctuations. Even after Tuesday's drop, the Philadelphia Semiconductor Index is still up around 5% for the month, outperforming the Nasdaq and S&P by about 8 percentage points. At this juncture, the pullback has reasons for both technical correction and the fragility of being at such heights.

Second, Overcrowded Positions and Temporary Absence of "Flooring" Support. Julian Emmanuel, Chief Equity and Quantitative Strategist at Evercore ISI, said in an interview with Bloomberg TV, "People are looking for reasons to hedge while wanting to stay invested." This statement aptly describes the current market's conflicting sentiment. Meanwhile, 65% of listed companies are currently in a buyback blackout period. In past downturns, corporate buybacks have been a crucial "flooring" force, but this time, that card cannot be played.

Third, Macro Background Changing. Expectations of Fed Rate Hikes are heating up rapidly—Bank of America projects three more rate hikes this year, and the market's pricing probability of a July rate hike has risen from almost zero to about 50%. The valuation logic of high-growth tech stocks is built on low-interest rate discounting. Once rates rise, the present value of future earnings naturally shrinks, hitting the stocks that rely on expectations to support their high valuations first.

Michael O'Rourke, Chief Market Strategist for JonesTrading Institutional Services, wrote, "Mega-cap cloud computing companies are the new software stocks. This sector is dragging down the 'Magnificent Seven' while unable to extricate itself from the dilemma."

Apollo's Chief Economist, Torsten Slok, has outlined the three core questions the current market faces: What would happen if AI companies started cutting computational budget due to insufficient ROI? What would be the market and credit market impacts if the Fed raised rates in September and December? These questions have no simple answers, but the market is transitioning from 'willing to overlook these risks' to seriously addressing them.

The reason why a technical adjustment deserves serious attention is not because of the magnitude of the decline itself, but because it is occurring when valuations, positions, interest rates, and sentiment are all at extreme levels.

In History, South Korea Crashes Have Been Brief—The Next Stress Test Is Micron

Historical data shows that sharp drops in the South Korean stock market are often intense but short-lived. This is a "silver lining" that bulls are willing to cite.

But this time, the backdrop is different from past purely domestic South Korean events: it touches on the global AI trading core nerve—Is the demand for memory chips truly as robust as expected? Has the fervor of data center construction already exhausted the future?

These questions will be partially answered after Micron's earnings report on Wednesday. Micron is the strongest component of the Philadelphia Semiconductor Index this year, with gains of over 300% before Tuesday. Wednesday's earnings report will be a true stress test.

What BTIG's Krinsky said may be the most direct: "Regardless of any short-term rebound, the mid-term downside risk for semiconductors remains."

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia