What is the hourly rental price of an Nvidia B200 GPU at the end of this year?

The prediction market has split this question into a series of binary contracts. Traders speculate on whether the rental price of the B200 will exceed a certain price, combining contracts for different prices and dates to form a GPU rental curve created by market betting.

Previously, Polymarket had launched GPU rental contracts, but with low trading volume. This time, Kalshi co-founder Tarek Mansour announced that the platform has extracted forward curves from the prediction market prices of B200, H200, and A100.

The prediction market is no longer just answering election results, interest rate cuts, and corporate events; it is beginning to establish financial markets for an industry that has never had a publicly traded market.

This curve is still far from the forward curves in traditional commodity markets, and the prediction market cannot deliver a set of GPUs to the buyer upon expiration. However, it has captured what the GPU trading market lacks the most: a price benchmark visible to everyone.

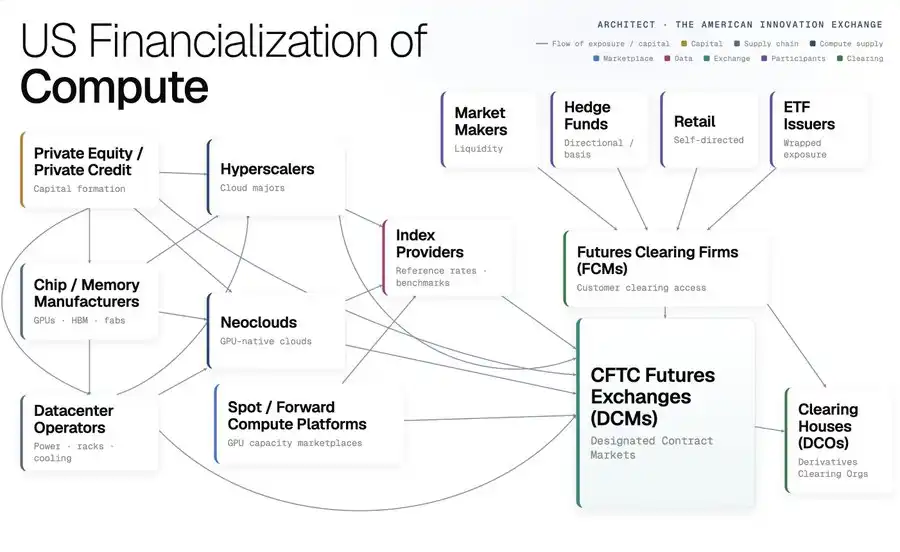

Over the past few years, capital has continuously flowed into chips, data centers, and power, where computing power has become one of the largest costs in the AI industry, yet procurement methods still remain in phone bookings, personal connections, and offline contracts.

The financialization of computing power is now in full swing.

Contracts First, Markets Later

Prior to the emergence of large models, enterprises primarily accessed computing power through two main methods: purchasing servers on their own or paying relatively stable monthly fees to cloud providers. AI has disrupted this procurement logic. Training and inference tasks require a significant amount of GPUs, causing price differentiation based on different chips, regions, and contract lengths, with cloud provider quotes rapidly changing based on supply and demand.

Today's computing power market is not devoid of forward transactions.

Large labs lock in future capacity, neocloud pre-purchases GPUs from cloud providers and brokers, and large-scale cloud providers reserve resources with each other. Contracts can range from hourly rentals for short periods to coverage over several years. They bear a resemblance to long-term oil off-take agreements, except that prices are negotiated in private.

A major inference service provider once described procuring computing power as finding a familiar "middleman" of supply. You tell them what chip you need, how many cards, and where you will be using them, and they search for inventory in their network of relationships for you. Brokers profit from information asymmetry, and major holders allocate capacity based on relationships, with the actual transaction prices rarely appearing on public screens.

This market can fulfill deliveries but cannot establish continuous expectations. The AI lab doesn't know the cost of inference six months ahead, data centers cannot precommit to rental pricing, lenders lack real-time updated data, and mortgage GPU is depreciating at a rapid pace.

The scale of funds no longer allows this pricing mechanism to remain as is.

The figure provided by Tarek is that mega-scale cloud providers will invest over $700 billion in computing power this year, with a projected market size of $70 trillion to $100 trillion by 2030. More conservative institutions forecast similarly vast figures. Morgan Stanley estimates that by 2028, global data center capital expenditure will be around $2.9 trillion, with approximately $2.5 trillion serving AI. McKinsey's estimate for data center capital expenditure by 2030 is $6.7 trillion. Goldman Sachs, on the other hand, pegs AI infrastructure investment from 2026 to 2031 at $7.6 trillion.

These figures adopt different years and statistical approaches, some encompassing data centers, others calculating both computing power and electricity. The common thread is that computation and hardware represent 55% to 67% of each estimation, making it the largest portion of this round of infrastructure investment.

Chips are another asset with highly volatile pricing. Market estimates for the lifespan of GPUs range from three to seven years, with new-generation products enhancing performance annually. Supply shortages allow old chips to retain leasing value. Data centers need to allocate significant funds to a batch of equipment with no consensus on depreciation rates.

The heavier the burden of capital, the more crucial forward prices become.

Exploring the GPU Trading Market

The first stage of the GPU trading market has been the years-long practice of "private matching."

Buyers pre-book capacity, sellers lock in future income, and brokers undertake the task of finding supply and matching trades. Real demand and forward commitments already exist; there are just no standardized contracts or public quotes.

This group of buyers and sellers also forms the underlying layer of the computing power financial market.

Mega-scale cloud providers, large data centers, and GPU holders hold inventory, concerned about future rent declines; AI labs, inference platforms, application companies, and neoclouds that have already committed capacity downstream need to make continuous purchases, fearing future price increases. One side wants to protect equipment revenue, while the other wants to control computing costs, thus initially driving trading demand in the market.

The second phase is to establish a standardized price index. Ornn's Compute Price Index extracts prices from real GPU rental transactions, covering a variety of mainstream chips. Silicon Data publishes daily on-demand rental indices for H100, A100, and B200, feeding data into the Bloomberg Terminal. Compute Desk is also building a similar product.

What the index sponsor defines is not just a string of numbers. Which chips, regions, network configurations, and contract types will be included, how to handle abnormal transactions, how the old index will phase out after chip upgrades – all of these will ultimately change the market's perception of "GPU prices." Exchanges provide the trading venue, while the index sponsor defines what people are actually trading.

Ornn recently received a $33 million investment from a16z. Whoever can organize scattered trading data into an accepted market benchmark has the opportunity to become a price gateway in the computing power market.

The third phase is to embed the index into tradable contracts. CME has selected Silicon Data as a data provider and plans to launch computing power futures settled against the daily GPU rental benchmark. ICE, the parent company of the NYSE, has chosen Ornn and is preparing to launch another set of GPU futures. Both traditional exchanges position the products as risk management tools for AI labs, cloud providers, data centers, and financial institutions, but the products are still awaiting regulatory approval.

The prediction market has taken a different path. It continuously asks traders the same question: "Will a certain chip be priced higher than a certain rental price on a specific date?" By calculating the price difference between adjacent thresholds, one can roughly reflect the market's assessment of that price range; repeating the calculation for different dates creates a term structure.

Traditional commodity markets usually define deliverable contracts first, followed by futures trading forming a curve. The prediction market first forms a public expectation with event contracts, then considers using this expectation to serve OTC trading, futures, and perpetual contracts.

While traditional computing power futures are still awaiting regulatory approval, the prediction market has already provided a term structure.

What Issue Can a Curve Solve

Despite the market's efforts to establish indices, futures, and forward curves, what problems can they actually solve for a typical AI company?

Let's say an inference platform has promised to provide services to a customer in six months. It knows it will need a batch of GPUs by then but is unsure of how much the rent will increase. If the rent suddenly rises, the agreed customer price remains unchanged, and the platform must absorb the increased cost. By buying a contract that appreciates with GPU rent increases, although the cloud bill becomes more expensive, the contract's profit can help offset some of the difference. Data centers face the opposite problem: once the equipment is purchased, if future rents decline, revenue will shrink. Selling a forward contract can allow them to lock in some equipment revenue in advance.

This contract does not need to match every card the enterprise actually procures. The enterprise may use an H200 in the New York area, but what trades on the market is an H200 index that covers multiple suppliers. As long as the two prices move roughly in sync, this contract can function. Analysts estimate that when the correlation between the two prices reaches 0.7, a properly allocated hedge can eliminate close to half of the volatility. Airlines cannot buy a contract that perfectly matches each of their jet fuel expenses and will still use crude oil futures to manage costs, and the same principle applies here.

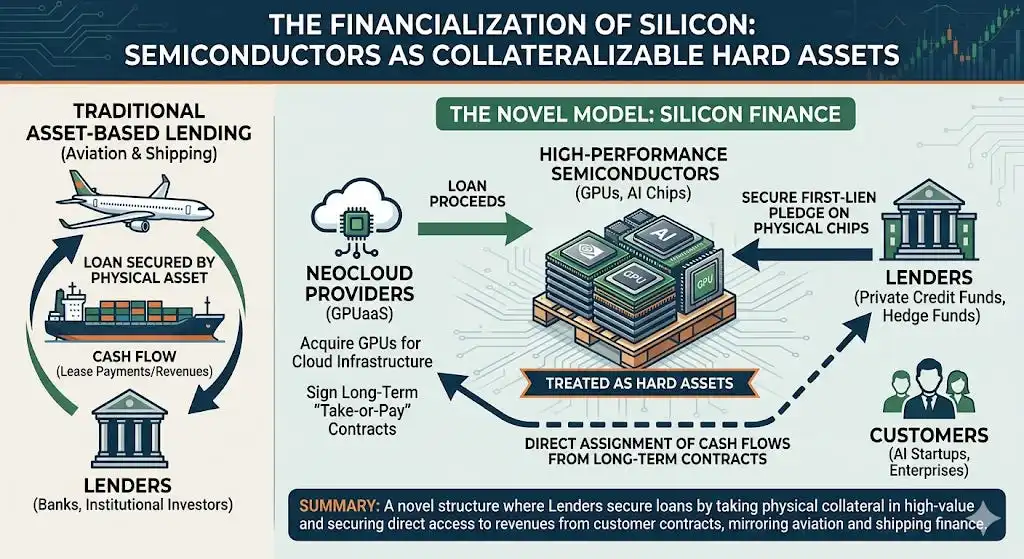

Lenders also need this curve. When a data center applies for a loan with GPUs, the bank needs to assess how much rent these chips can still bring in two years. In the past, they could only rely on manufacturer quotes, scattered trades, and their own assumptions; with a public curve, lenders can adjust collateral valuation as the market changes, and data centers can more easily demonstrate future income.

Prices may even influence which chip enterprises choose. If Nvidia GPU leases see more transactions, have a more reliable index, and more active hedging tools, banks will be more willing to accept it as collateral, and holders will find it easier to rent out or sell when needed. Devices are therefore easier to finance, more buyers will continue to choose them. The liquidity surrounding Nvidia in these transactions may become a competitive advantage that rivals find difficult to replicate.

Thus, a price curve serves not only traders. It allows users to know costs earlier, enables holders to determine income sooner, and gives lenders the confidence to price equipment and data centers.

Bottlenecks & Challenges

The first issue is the index.

Ornn emphasizes real transactions, Silicon Data focuses on on-demand leasing prices, and other solutions standardize energy costs. Each approach retains some information while discarding others. No index covers chips, regions, terms, networks, and counterparties simultaneously.

At the same time, chips evolve rapidly.

The metric for oil can be used continuously, but the GPU market has upgraded from H100 to H200, B200, GB200, and Rubin. AMD, Google TPU, Amazon Trainium, and dedicated chips continue to divert computing demand. The exit of old indexes, how old and new chips interface, will continue to change the underlying asset of contracts.

The second issue is settlement.

After cash-settled contracts expire, only money is exchanged, not GPUs. Companies that need to control costs can use contract returns to offset rent increases, but neocloud, which has already committed capacity to customers, still has to source cards on the market.

Another risk comes from the trading volume.

The publicly recorded real trading volume in the GPU rental market may be minimal, with the supply concentrated in the hands of a few sellers. As a result, a single transaction could significantly move the index, and the party controlling the supply could more easily influence the final settlement price.

This is also a problem with the curve drawn by the prediction market.

Traditional forward curves rely on delivery or spot exchange mechanisms to pull the futures price back to real supply and demand. Prediction markets' binary contracts lack this channel, and the curve represents participants' expectations, which have not yet become deliverable, arbitrable spot prices.

The third issue is liquidity.

Sellers prefer long-term contracts because data centers want to lock in revenue in advance; buyers prefer short-term contracts because AI companies need the flexibility to switch chips and suppliers. The two parties' demands on the term are naturally misaligned. Brokers and large holders also profit from the opaque market, lacking the incentive to actively conduct all transactions in the open market.

Despite numerous obstacles, the demand for public prices in the hash rate market will not regress. Perhaps before long, we will see reports of a savvy investor "leveraging five times long on hash rate" on-chain.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia