On April 28, the United Arab Emirates announced its withdrawal from OPEC and OPEC+, effective May 1, ending its nearly 60-year membership. On that day, Brent June futures surged by $1.11 to $109.34 per barrel. This is the story currently seen in financial media. However, Brent July futures only increased by $1.08 to $102.77, $6.57 cheaper than June. Putting these two numbers together tells another story.

The UAE is OPEC's third-largest oil producer, after Saudi Arabia and Iraq. Its position within OPEC has always been awkward, with its production capacity expanding faster than quota updates. In 2023, due to dissatisfaction with low quotas, it delayed the entire OPEC+ production increase agreement for several months. This direct exit is interpreted by various media outlets as the biggest challenge to Saudi Arabia's leadership.

After the UAE's announcement, the market's oil price outlook was split into two sets: spot prices surged, while longer-dated futures remained unchanged. The price difference between these two sets of pricing is the market's real response to the "UAE exit" event.

Actual Capacity is 1.5 Times OPEC Quota

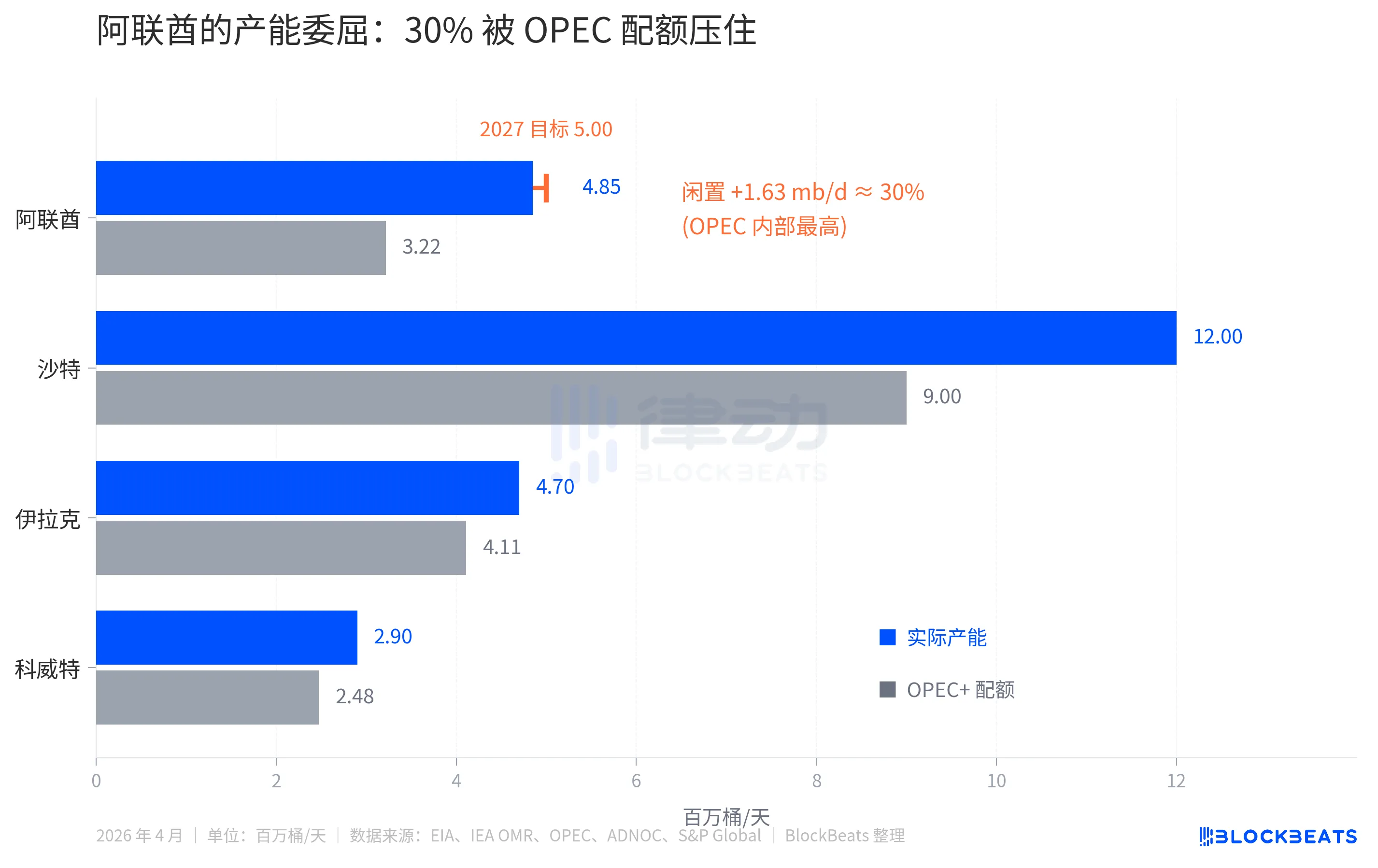

According to EIA data, the UAE's current actual capacity is 4.85 million barrels per day (mb/d), but its OPEC+ quota for 2025 has recently been kept around 3.22 mb/d. The difference is 1.63 mb/d, equivalent to about 30% of its capacity being artificially idle.

A similar gap in Saudi Arabia is about 25% (actual capacity of 12 mb/d versus quota of 9 mb/d), while in Iraq and Kuwait, it is only 10-15%. Among the 13 OPEC countries, the UAE is the most severely suppressed member.

There is another layer of dissatisfaction. The UAE's national oil company, ADNOC, is accelerating its investments. According to an ADNOC announcement, the capital expenditure budget for 2023-2027 is $150 billion, and the 5.0 mb/d production target has been brought forward from 2030 to 2027. While investing heavily to expand capacity, they are constrained by OPEC quotas from selling more, resulting in daily losses in revenue per million barrels.

This is the financial reason why the UAE had to leave. However, looking solely at this reason, based on economic logic, a member country with 30% idle capacity breaking free from quota constraints would mean it will produce more oil. Increased oil production translates to a supply increase. A supply increase is bearish for oil prices.

Crude Oil Contango

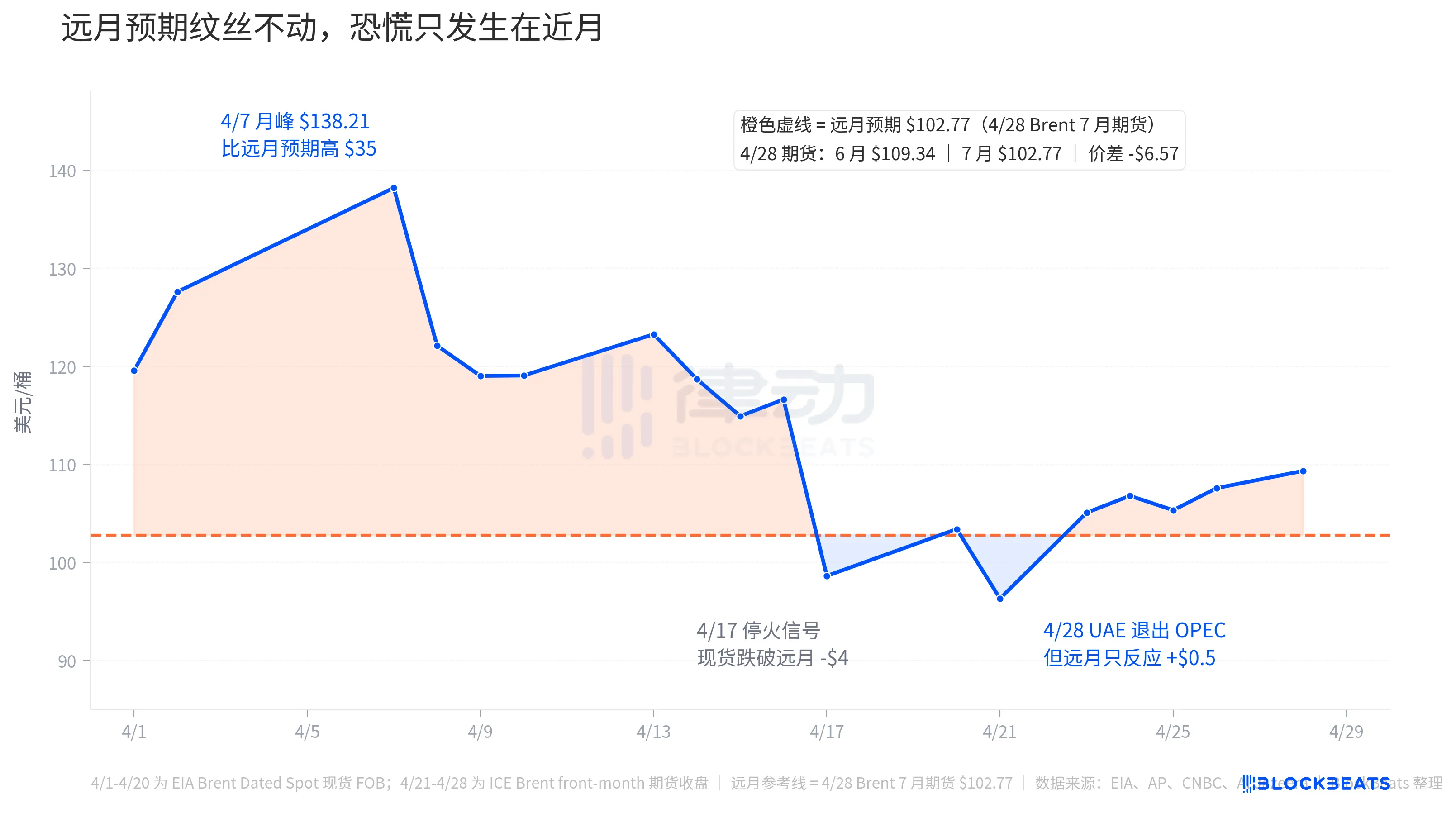

On April 28, the headline in the mainstream media was "Brent Surges". However, it was only the prompt contract that surged. The far-month expectations, represented by the orange dashed line, remained almost unchanged throughout April.

On April 28, Brent futures closed with the June contract (front-month, equivalent to the price of "getting oil immediately") at $109.34, and the July contract at $102.77, with a price difference of $6.57. This futures curve exhibited deep backwardation, with the prompt month being driven up and the far month relatively cheaper.

The futures curve is not a guess; it is the true price of the contract. It tells you that the market is willing to pay more for oil now, and less in a few months. The logic behind this is simple: the market expects the resolution of the Hormuz crisis, OPEC's supply coordination to loosen, and the UAE's 30% idle capacity to enter the market.

To better understand this story throughout April, let's rewind. According to EIA Brent Dated spot data, on April 7, the spot price surged to $138.21 per barrel, the peak within the month, $35 higher than the far-month expectation of $102.77 on 4/28. This $35 is the market's panic premium willing to be paid for "getting oil immediately." At that time, the US-Iran conflict entered the ninth week, the passage through the Hormuz Strait was nearly completely blocked, and the daily transportation of about 20 million barrels of Middle Eastern crude oil was almost reduced to zero.

Then, on April 17, a ceasefire signal emerged, and the Brent spot price plummeted to $98.63 on the same day, dropping below the far-month expectation by approximately $4. The market briefly believed the conflict was about to end, so the "future oil price" became more expensive than the "current oil price." This abnormal state lasted only a few days, with Brent falling to a monthly low of $96.32 on April 21, before rebounding on April 23.

On April 28, the UAE announced its withdrawal, causing Brent in June to rise by another $1.11 to $109.34, once again moving above the far-month expectation by $6.57. However, this was only a fraction of the panic premium seen at the beginning of April. In other words, the market's reaction to the "UAE withdrawal" was much smaller than its reaction to the Hormuz crisis.

The far-month line speaks more directly. On the day the UAE announced its withdrawal, the July futures only rose by $1.08 to $102.77, nearly identical to the increase in the June futures. This implies that the market believes the impact of the UAE withdrawal on medium-term oil prices is close to zero, neither bullish nor bearish. The short-term surge is headline noise overlaid with the psychology of Hormuz.

The Largest Exit in OPEC's History

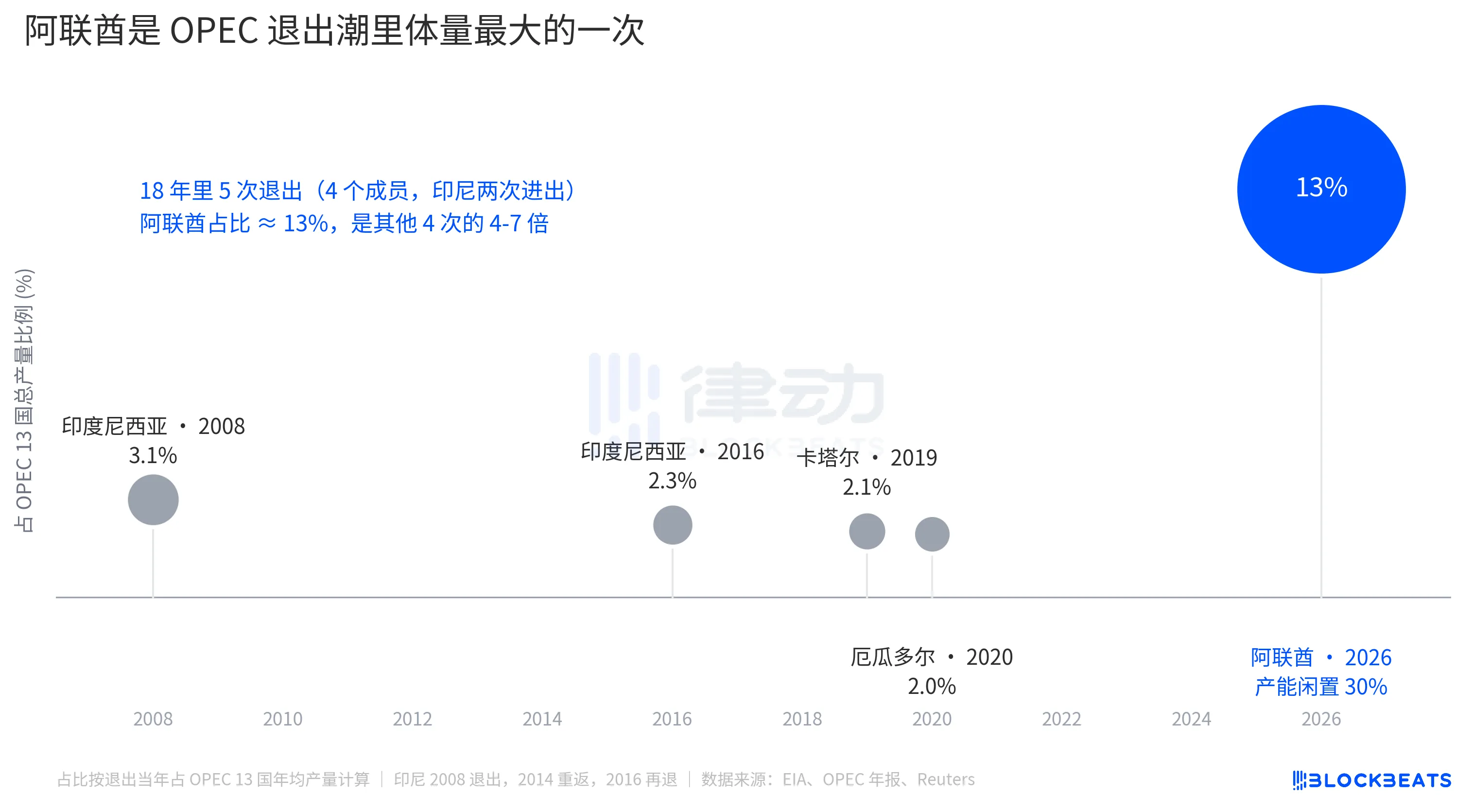

In 2008, Indonesia exited for the first time (returned in 2014 and exited again in 2016), Qatar exited in 2019 to focus on LNG, and Ecuador exited in 2020 due to fiscal pressures. At the time of these 4 exits, the departing members accounted for 2-3.1% of OPEC's total production each. Each exit was seen as an isolated event, and OPEC's market share was not significantly affected.

The UAE's share is 13%. One exit is equivalent to more than 1.5 times all exits in the past 18 years combined.

However, in terms of oil price dynamics, a large volume does not necessarily lead to a large impact. Within the OPEC framework led by Saudi Arabia, the 13% figure needs to be absorbed, as Saudi Arabia still has around 25% of idle capacity that can be brought online to offset this loss, and OPEC+ members' production quotas can be adjusted. The market did not interpret the "13% volume loss by OPEC" as "a significant future increase in oil prices."

The real structural impact lies at another level, further weakening OPEC's role as a "price regulator." According to the IEA, OPEC+ is estimated to have 4-5 mb/d of overall spare capacity in early 2026, with the UAE contributing around 0.85 mb/d. After the UAE's exit, the spare capacity of OPEC's 13 countries will shrink to around 1 mb/d. This is the "ammunition" that the market can use in the future in case of a supply shock, with 1 mb/d only covering about 1% of global demand.

This is why futures contracts for distant months only rose by $1, not because a few extra barrels from the UAE would push oil prices down, but because OPEC's ability to act as a price stability anchor has been further eroded.

Mainstream reports have intertwined the UAE's exit with the rise in the Hormuz Strait tensions, making it appear as if OPEC's disintegration is boosting oil prices. However, the futures curve has separated these two events. In early April, Brent spot prices were once $35 higher than the forward month, reflecting the Hormuz Strait panic premium. On April 28, the near-far month price spread was only $6.57, a sum of the UAE's exit and the headline noise. The market's true pricing of the UAE's exit is hidden in the almost unchanged distant month line.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia