TL;DR

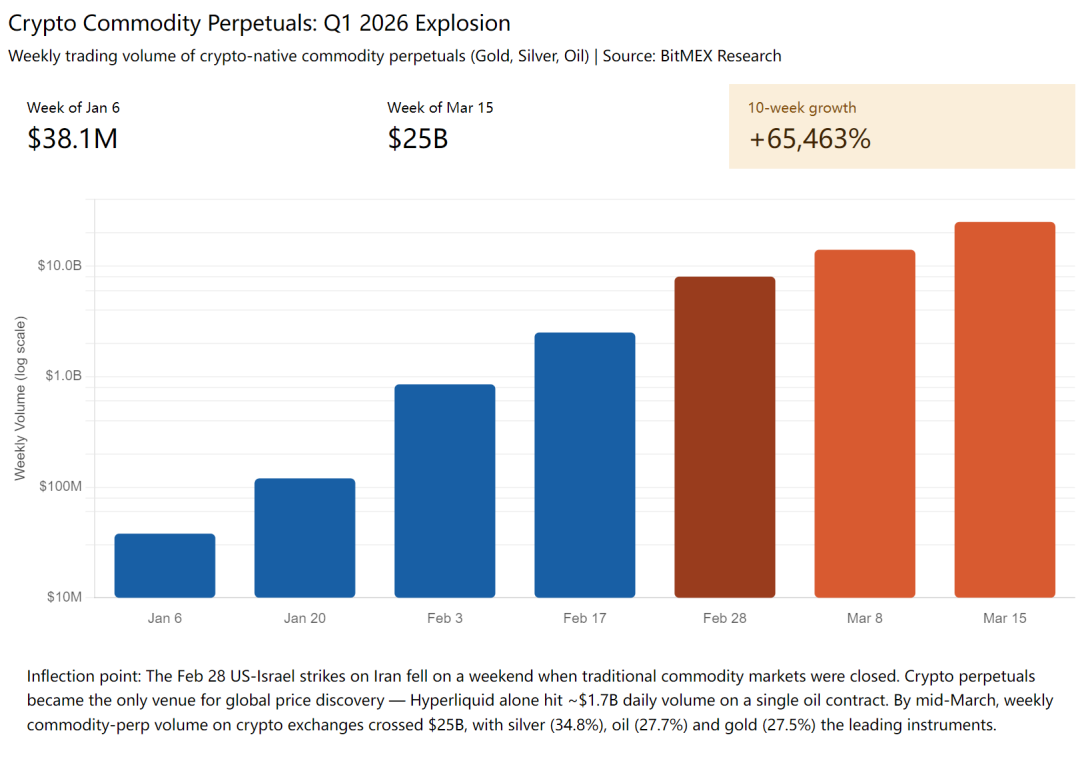

In Q1 2026, the weekly trading volume of commodity perpetual contracts (gold, silver, oil) on crypto exchanges surged from $38.1 million to $25 billion, a growth of 65,463%. Traditional asset tokenization will be the main theme in the next 5-10 years of the crypto space, and Pre-IPO tokenization is just the latest addition to this wave.

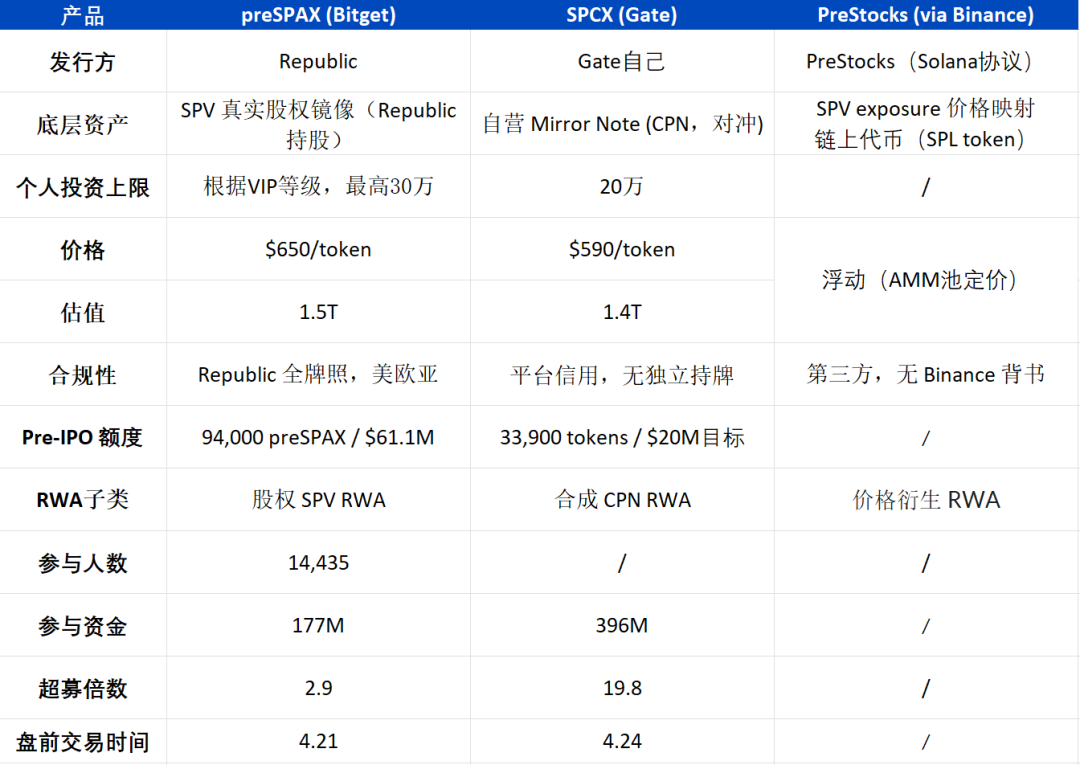

In April, three top exchanges—Bitget, Gate, and Binance (PreStocks)—almost simultaneously launched tokenized products related to SpaceX. Although their compliance methods differ, they all essentially break down the previously exclusive pre-IPO market share held by ultra-high-net-worth clients into fragments for retail investors to buy.

This article aims to clarify two main points: what exactly is traditional Pre-IPO, and how exactly can retail investors participate

Traditional asset tokenization will be the main theme in the next 5-10 years of the Crypto space

According to statistics, in Q1 2026, the weekly trading volume of commodity perpetual contracts (gold, silver, oil) on crypto exchanges surged from $38.1 million to $25 billion, a growth of 65,463%. After Binance launched the TradFi Perpetual section in January, the cumulative trading volume in three months exceeded $153 billion, with over 114 million trades; the XAG (silver) contract's daily average trading volume reached $1.31 billion, and its global market share soared from 0.2% to 4.9% (a 23.5x increase).

Most notably, the end-of-February Iran war, during which the US and Israel's strike on Iran occurred over the weekend, causing traditional futures, stocks, and Forex markets to close, while only the crypto market remained open for trading. At that time, Hyperliquid's oil perpetual instantly surged by 5%, Tether Gold XAUT's daily trading volume exceeded $300 million, and Bitwise CIO referred to it as "the weekend that changed finance".

Assets such as US stocks, precious metals, crude oil, and forex, which used to only trade during office hours on weekdays, are now being tokenized, put on-chain, and providing 24/7 global liquidity. Pre-IPO tokenization is just the latest addition to this wave.

What Is Pre-IPO

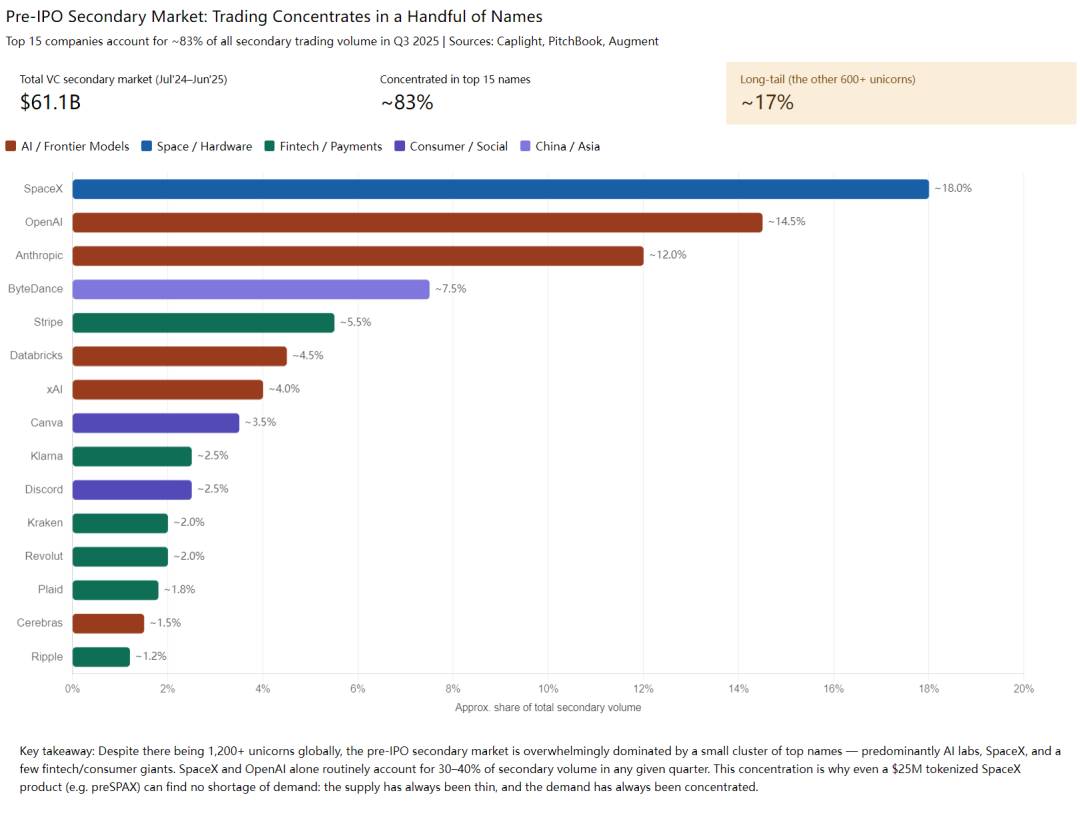

The Pre-IPO secondary market (late-stage trading) has been around for over a decade, with global trading volume reaching $160 billion in 2024, of which the US direct secondary market alone accounts for $61.1 billion. Buyers mainly consist of family offices, sovereign wealth funds, institutional investors, and high-net-worth individuals, with individual transactions typically starting from $10 million, leaving retail investors mostly out of the equation.

The majority of trades are facilitated through Special Purpose Vehicles (SPVs): existing shareholders place their shares into a specially created shell company, which then sells its shares to new buyers. Buyers receive shares in the SPV, indirectly holding equity in the underlying company.

This is because rare are the occasions when strangers are directly added to the cap table in late-stage trading transactions, as this would trigger other shareholders' Right of First Refusal (ROFR), leading to complexities in the process and potential hindrances from existing shareholders. Hence, buyers ultimately acquire LP interests or Units of the SPV, representing an indirect ownership of the pre-IPO shares.

Due to the high concentration of trades in a few select targets in the secondary market, with major US AI/space industry giants such as SpaceX, OpenAI, and Anthropic accounting for 30-40% of the trading volume over the long term, along with unicorns like ByteDance, Stripe, Databricks, xAI, the top 15 companies capture approximately 83% of the entire market's trading volume.

(This level of concentration is also why even in offerings like the recent one by Bitget/Gate, where only SpaceX tokens were issued, easily raising over a billion, the scarcity of marquee Pre-IPO opportunities and concentrated demand are evident.)

The majority of these targets are US-based, hence the most significant regulatory hurdle is CFIUS (Committee on Foreign Investment in the United States). It restricts foreign capital from investing in sensitive US industries (AI, semiconductors, defense), and investments from certain countries in SpaceX/Anthropic undergo strict scrutiny.

So before the transaction, sellers generally specify that purchases by UBOs from certain countries are not allowed—the GP will penetrate the SPV to check whether the ultimate beneficial owner of the buyer is from a restricted nationality such as China, Russia, or Iran. The deeper the hierarchy, the harder it is to investigate, but it is not foolproof. We had a case before where a Chinese UBO was found in a two-layer SPV, and the entire deal fell through.

After a U.S. company's IPO, there is also a standard Lock-up Period: SEC Rule 144 and the underwriting agreement stipulate that early shareholders and employee shares can only be sold on the open market 6 months after the company's IPO. This rule applies to almost all U.S. companies (Facebook, Coinbase, Reddit, Cerebras all have a 6-month lock-up).

This is why Bitget/Gate's Pre-IPO this time requires the "tokens to wait for 6 months before redemption," but it does not affect pre-market trading.

Pre-IPO Real Trading Details Sharing

Extremely High Ticket Size

The traditional Pre-IPO ticket size starts at around $10 million, and hardly anyone participates if it is below $1 million—not because they don't want to, but because the fixed costs per transaction (legal fees, KYC, SPV establishment, channel fees) are too high. Therefore, this wave of operations on the trading platform is a disruptive attempt that breaks down class barriers.

In the past, retail investors (and they had to be sophisticated players with conditions such as a U.S. stock account) could only participate in trading after the IPO. Now, although the trading platform is more expensive, at least it gives ordinary people the opportunity to participate.

Broker/FA Chaos

A cross-border Pre-IPO deal usually goes through multiple layers:

Bottom GP - Rep (Seller's Representative) - Tier 1 broker - Tier 2 broker - … - FA - Client

Each layer incurs a 1-5% fee. For a base-layer deal with a $500 billion valuation, the price by the time it reaches the actual buyer could easily be above $600 billion.

Take SpaceX, for example, with a true market price of around $1.25 trillion and a 3-11% access fee (varying by channel and level), the final price would be approximately $1.375 trillion, and this is without factoring in the costs of Tokenization compliance. Overall, considering these estimates, the price offered by the trading platform seems reasonable, most likely driven by a customer acquisition motive.

Furthermore, most of the Block supply in the market is misleading—the same batch of shares is listed by multiple brokers, with less than 10% actually available for trading. For instance, in the case of SpaceX, a platform may list a valuation of $1.2 trillion, but upon further investigation, all orders are fake, even major platforms and intermediaries are plagued with such situations.

If the transaction involves an LP Interest Swap, you also need to obtain GP Consent, which is the General Partner's right to approve the transfer of LP shares within the underlying SPV. The GP has the authority to reject this. The reality in the industry is that GPs are not very receptive to such transfers—conducting due diligence on new LPs, ensuring compliance, and introducing strangers are all troublesome tasks. Therefore, in many cases, you might need to pay the GP to get things done, thereby incurring an additional layer of fees.

Liquidity Illiquidity is the Biggest Pain Point for Pre-IPO Shares

Exiting midway is extremely challenging. You either wait for the company to IPO (usually 3-7 years), and even post-IPO, you often have to wait for a 6-month lock-up period. Or you start all over again to find a buyer and go through the structured process—two to three weeks (at best) plus an FA fee.

Each transfer is a standalone OTC transaction, requiring a redo of legal documents, KYC/AML/UBO checks, and GP approvals. This is why Pre-IPO shares have always been classified as "illiquid assets."

How Can Regular Individuals Participate in this Round of Pre-IPOs

It is foreseeable that the market will witness a series of old-stock tokenization products, all essentially the same: platforms acquiring genuine pre-IPO shares from the traditional market and then fractionalizing them into tokens to sell to retail investors.

For the average person, having the opportunity to enter rounds before a company's IPO, following the valuation as it naturally rises round by round.

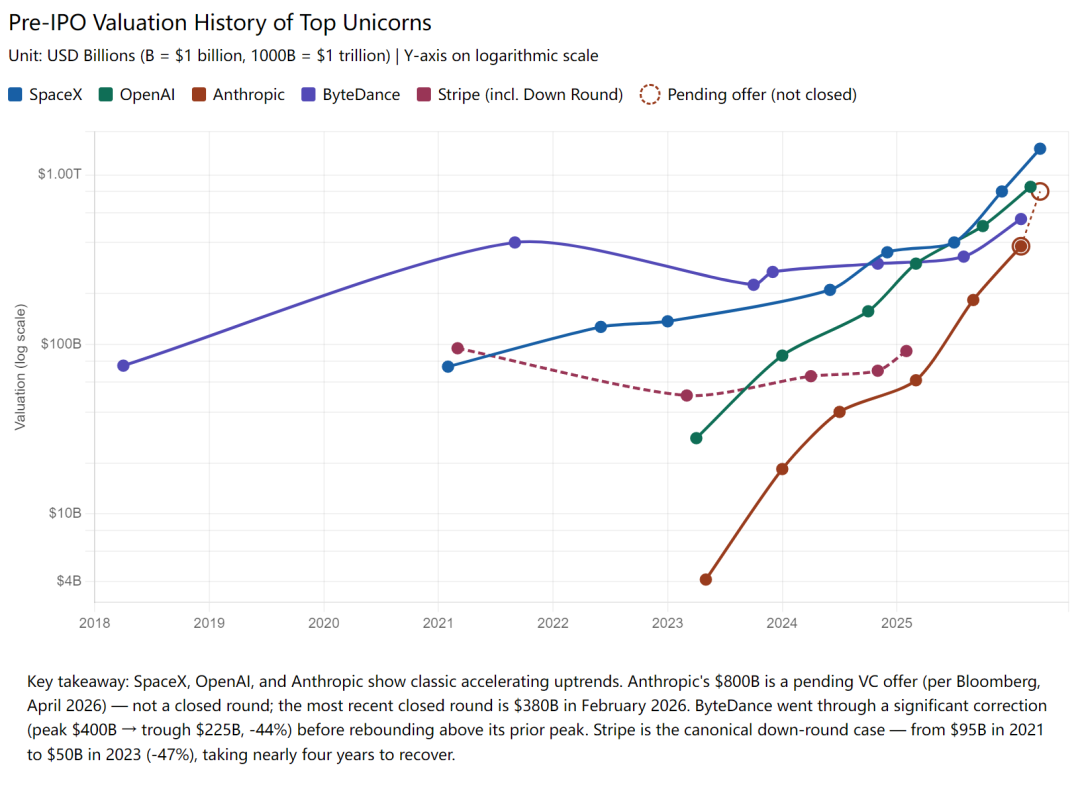

The financing valuation of top-quality targets usually shows a monotonically increasing trend. SpaceX has risen from $74 billion in 2021 to over $1.4 trillion now, OpenAI from $29 billion to over $852 billion, Anthropic from $4 billion to over $800 billion, and ByteDance from $75 billion to over $600 billion. Each new round of financing raises the valuation, lifting existing shareholders with it.

But one must be clear about one thing: this is not a guaranteed win. In history, Stripe experienced a down round where the valuation was halved from $95 billion to $50 billion, TrueLayer saw a 30% drop, Cybereason experienced a 90% drop, and WeWork went from a $49 billion valuation to bankruptcy. In 2023, 128 global unicorns saw a valuation drop, with 42 directly falling out of the unicorn ranks.

So the key to participating in Pre-IPO is choosing the target, not timing the market, following the natural rise in the company's valuation to earn long-term returns—instead of rushing to buy at the listing and trying to speculate on short-term price swings. Many crypto users treat Pre-IPO like a coin IDO in the crypto world, which is a completely different logic.

In summary, the logic of participation is:

1. Do you believe in the long-term potential of this target? Is SpaceX/OpenAI/Anthropic worth the valuation level post-IPO? Are you willing to hold until the next round of fundraising or after the IPO?

2. Is the product you have chosen safe? Who is the issuer? Where is the backstop? Who is liable in case of failure?

Future Shape of RWA in the Next 3 Years

The RWA transformation of Pre-IPO is still in a very early stage, with scarce supply of top targets, highly concentrated demand, and a long-term upward valuation trend. Over the next few months, tokenized products of top targets such as OpenAI, Anthropic, xAI, Stripe, ByteDance, Kimi, etc., will continue to emerge.

And this is just a small branch of the entire Tokenization, with the main line's four-layer structure foreseeable as:

· Stablecoin Issuer: Provides on-chain dollarization and off-ramp

· Public Blockchain Network: Facilitates asset issuance and circulation

· Trading and Distribution Platforms: CEX, DEX. Additionally, we believe there is another potential player, LaunchPad/IDO Platform (such as Buidlpad), which already has the full capabilities for new asset KYC, issuance, subscription, and distribution. In the past, they issued crypto tokens, and today they can fully launch Pre-IPO tokens

· Asset Issuance Service Provider: Companies that provide services for on-chain assetization

It is foreseeable that the Tokenization trend will not only give birth to a group of unicorns but also has the potential to nurture new trillion-dollar-level infrastructure and a group of hundred-billion-dollar-level platform players.

Everything is just beginning.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia