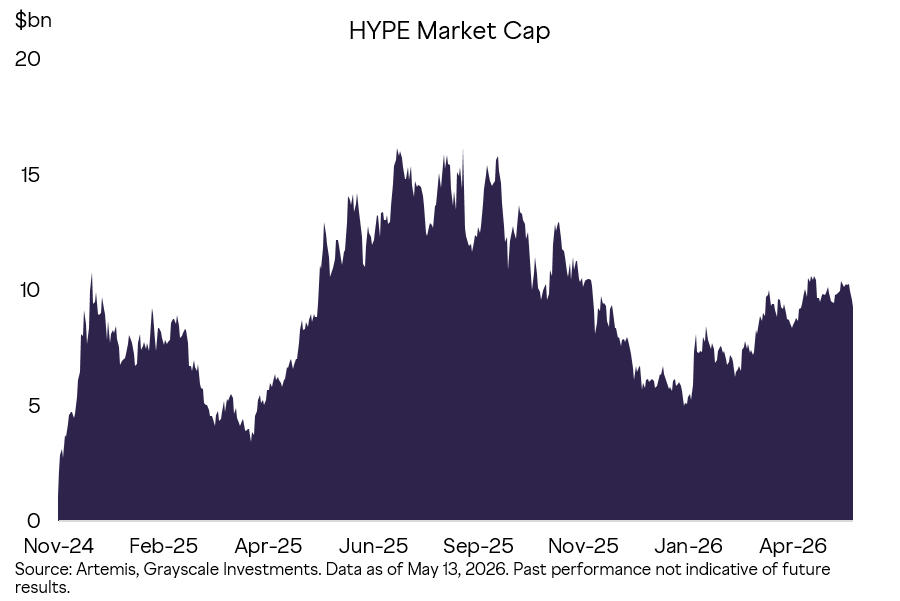

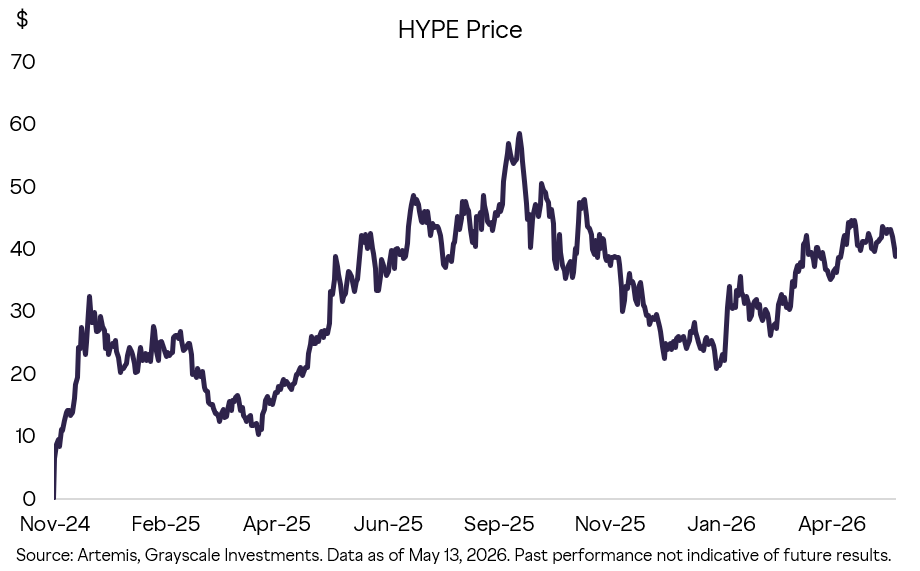

Like other blockchain protocols, Hyperliquid is not a company and does not issue stock. Its token drives the entire network and captures value from transaction activity. The circulating market capitalization of HYPE is around $13 billion, ranking it as the 8th largest cryptocurrency by market cap.

Compared to comparable publicly traded companies, HYPE's valuation multiple is not considered high. Considering the platform's user growth, vast potential market, and upcoming regulatory loosening, we believe Hyperliquid still has significant upside potential.

Perpetual Contract Foundation

While Hyperliquid has a larger vision, what has made it stand out is decentralized perpetual contract trading. This product class originated in the crypto industry, and Grayscale believes it will eventually deeply penetrate traditional finance.

Traditional futures contracts have expiration dates. For example, an oil futures contract is an agreement to deliver a certain quantity of oil on a specific date. Participants holding positions at expiry must either physically deliver or receive the underlying asset. If one only seeks a pure financial exposure, users need to "roll" their positions to a later contract before expiry.

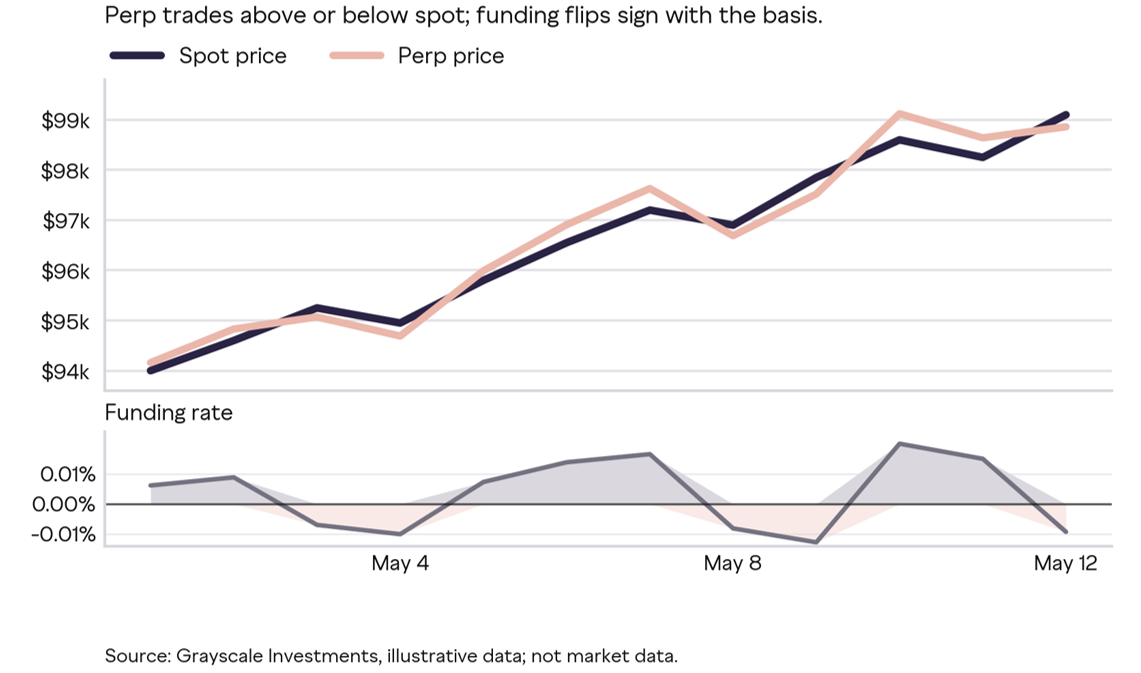

Perpetual contracts have no expiration date and will never settle. Their design purpose is to provide pure financial exposure to the underlying asset for hedgers and speculators, usually trading 24/7.

Traditional futures can anchor the asset price because someone must deliver at expiry. Since perpetual contracts never expire, what keeps their price in line with the underlying? The answer lies in the funding rate mechanism: longs and shorts periodically pay a small fee to each other.

When the perpetual contract price is above the spot price, longs pay shorts; when it is below, the opposite occurs. The greater the deviation, the higher the fee.

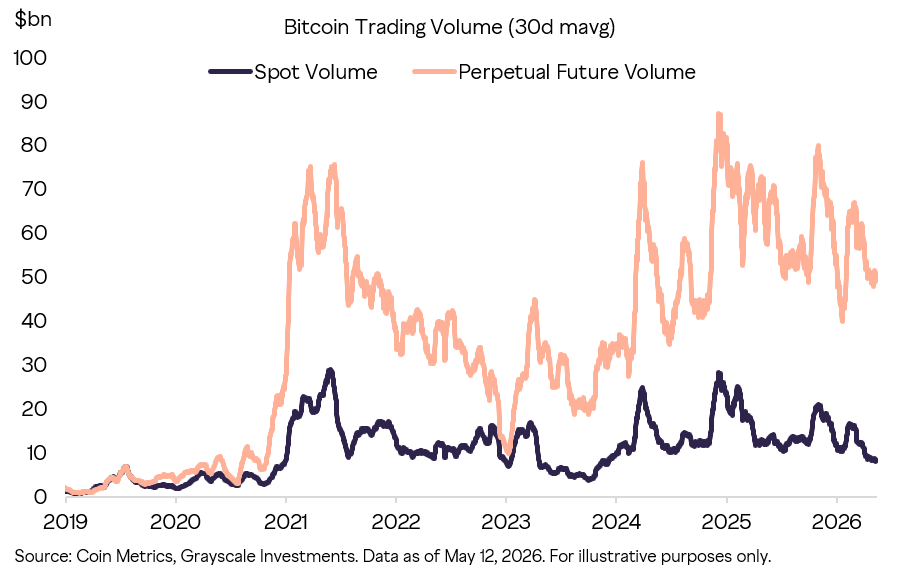

Perpetual Futures Contracts and the Crypto Market are a natural fit. With 24/7 trading of crypto assets, high demand from both retail and professional speculators, and new assets being introduced at a much faster pace than traditional futures exchanges.

Perpetual futures contracts provide traders with a simple way to express directional views, hedge spot exposure, and utilize leverage around the clock. It has now become one of the core markets for crypto price discovery.

Retail traders have many channels to access leverage: traditional broker margin accounts, futures with expiry dates, options, leveraged ETFs. The crypto market experience shows that when all options are available, retail traders tend to prefer perpetual futures contracts, largely because they are straightforward. Once a broader set of traditional market participants can also use perpetual contracts, a similar user migration is expected.

Hyperliquid's Breakthrough

Hyperliquid has achieved a core breakthrough: Centralized Exchange-level performance + Blockchain transparency and self-custody.

From a trader's perspective, Hyperliquid is almost indistinguishable from a centralized exchange: deep order book, quick trades, a familiar position management interface. However, every Hyperliquid trade is recorded on-chain, including settlement, and users always maintain self-custody.

Leveraged trading is the most fiercely competitive segment in the crypto market, with users being extremely demanding. Hyperliquid's success is based on product strength.

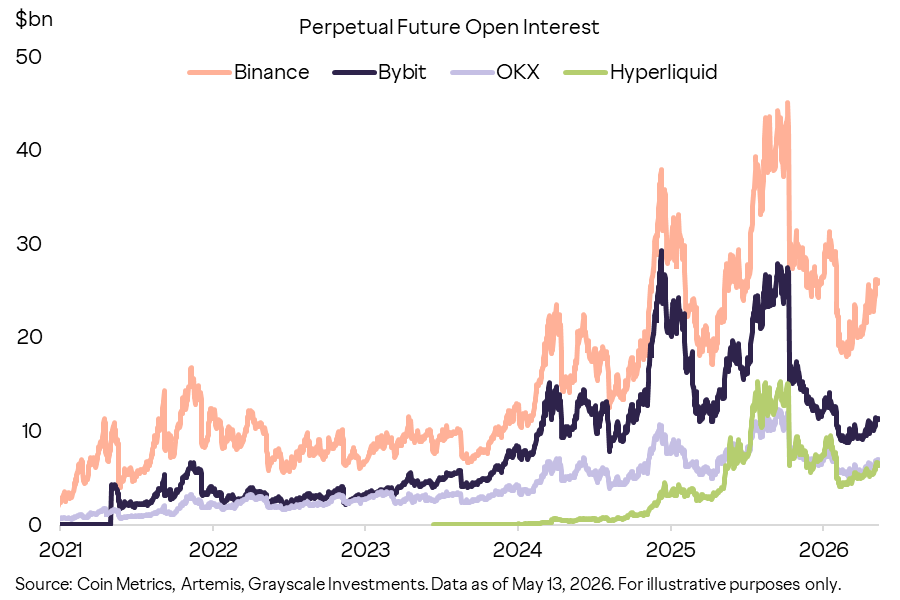

Key Stats: In 2025, perpetual futures trading volume was $2.9 trillion, with the current open interest at around $7 billion, ranking it as the third or fourth largest perpetual futures trading platform in the industry by OI.

Trading volume, open interest, fee revenue, and market attention are all growing in sync, and the platform has already started expanding from a purely crypto market to a broader range of tradable assets.

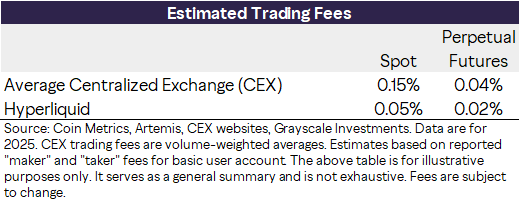

In terms of fees, Hyperliquid has a cost advantage over centralized exchanges.

Based on the 2025 trading data for BTC and ETH, the weighted average fees for CEX are 15 basis points (bp) for spot and 4 bp for futures; for Hyperliquid, they are 5 bp and 2 bp, respectively.

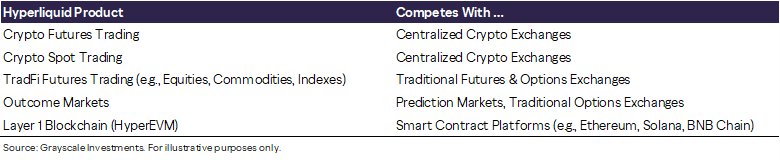

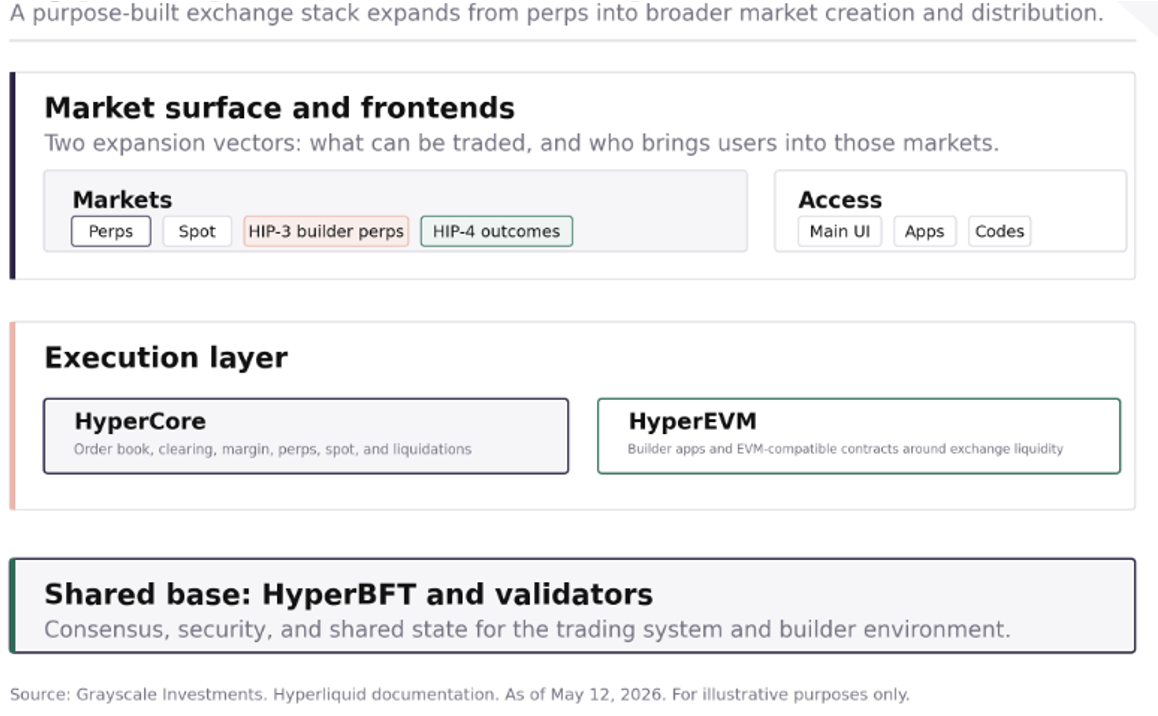

Of particular note, Hyperliquid has extended its product line beyond crypto perpetual futures through an open architecture approach.

New features are typically introduced through Hyperliquid Improvement Proposals (HIPs), where products are deployed by third-party developers rather than the Hyperliquid team itself.

HIP-3 allows developers to deploy new perpetual futures markets, including equities, commodities, indices, and other non-crypto assets. These markets have been well-received by users and are starting to serve as venues for post-close price discovery for traditional trading assets.

Bloomberg directly used this framework to describe Hyperliquid's commodity perpetual futures, stating that the trends in its crude oil, gold, and silver perpetual futures contracts "may provide a signal of how these markets will react post-mainstream trading recovery."

In another report, Bloomberg referred to Hyperliquid as "an all-weather leveraged commodity trading venue."

Trading volume data confirms this positioning. During a silver surge in February, the Silver HIP-3 perpetual futures daily trading volume reportedly exceeded $4 billion.

At one point on February 5, the nominal trading volume of the HIP-3 Silver perpetual futures contract was approximately 1% of COMEX Silver trading volume. During a Middle East oil price fluctuation, the HIP-3 Crude Oil perpetual futures contract recorded over $4 billion in 24-hour trading volume on April 9, surpassing, at times, the trading volume of Bitcoin perpetual futures.

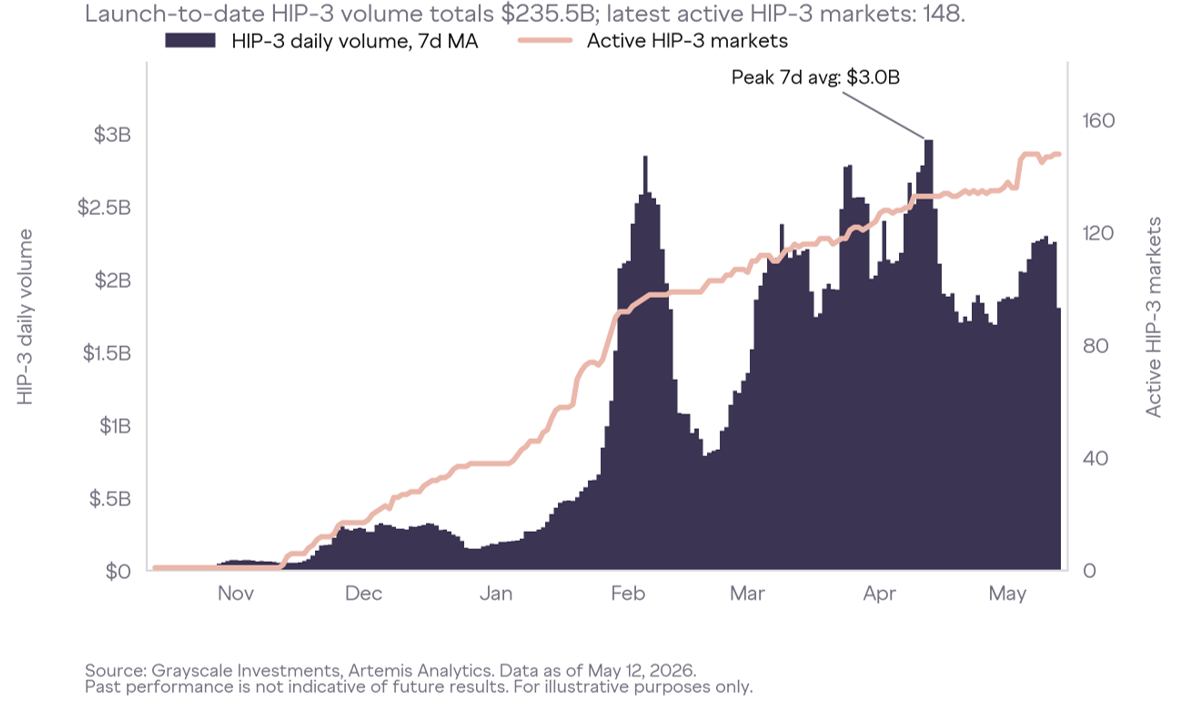

An officially sanctioned S&P 500 contract is now also trading on Hyperliquid through HIP-3, including on weekends. Since its launch, HIP-3 has accumulated a total trading volume of over $230 billion, with currently over 140 active trading pairs.

HIP-4 further extends to outcome markets, similar to binary options in prediction market contracts.

These contracts are also deployed by third-party developers, but the trading activity still generates fee revenue for Hyperliquid.

Hyperliquid's Technical Architecture

The underlying architecture revolves around two core components:

HyperCore is the trading system, encompassing order book, clearing, perpetual contracts, spot, margin, and settlement environments. This is the primary part that traders directly interact with.

HyperEVM is the developer-facing environment that provides an EVM-compatible development interface integrated with the Hyperliquid system. The strategic intent is to have applications build around the liquidity, user, and asset base already created by the trading platform, rather than starting from a cold network without native financial activity.

HyperBFT is the Delegated Proof of Stake consensus layer responsible for network security.

The key design choice is that Hyperliquid is not an application built on a general-purpose public chain, but a purpose-built chain and execution stack optimized for trading platform performance, aiming to make on-chain trading experience competitive with centralized trading infrastructure.

The Five Elements of Success

Hyperliquid opened to the public in August 2023, earlier than the US Bitcoin ETP listing, at a time when the overall DeFi market was experiencing a downturn. Its success was not a product of speculative bubbles, but because it addressed a specific problem better than most crypto infrastructure projects: making on-chain trading truly usable for high-frequency traders.

The five key factors:

Product Focus. Hyperliquid was built around the perpetual contract trading scene, rather than treating trading as one of many applications. This prioritized what the product needed to satisfy active traders' most critical needs: quick order placement, reliable execution, clear position display, and a familiar trading platform interface.

Market Selection. Hyperliquid garnered attention by listing markets that trading participants "most want to trade" at that moment, particularly long-tail high-heat assets beyond BTC and ETH.

Platform Flexibility. HIP-3 enabled developers to directly deploy new perpetual contract markets, shifting the listing model from a centralized gatekeeper to an open market creation system.

Distribution Network. Hyperliquid's builder code and frontend model gave third parties a reason to channel users into a single liquidity pool rather than dispersing them across isolated venues. The economic benefits have been substantial: Phantom has earned approximately $19.7 million through builder code integration of Hyperliquid perpetual contracts, accruing from routing trading fees.

Community. Hyperliquid's token distribution rewarded platform users rather than venture capitalists or pre-selected insiders. This created a different early holder structure—traders, market participants, and developers—who had intrinsic reasons to pay attention to the project. In a trust-scarce race, this is crucial.

Individually, these advantages may not be decisive, but together, they explain why Hyperliquid became one of the few crypto applications that could be measured for success based on actual usage rather than vision.

Hyperliquid can solidify its competitive moat through the interaction of liquidity, distribution, and developer incentives. The larger the trade volume, the better the liquidity and execution quality, attracting more users and third-party frontends. Builder code and HIP-3 give external developers an economic incentive to route activity back to the same liquidity pool.

This has created a potential network effect where newcomers find it challenging to replicate: liquidity attracts distribution, distribution brings more trading volume, and the volume further strengthens the protocol's economic base.

HYPE Token

The HYPE token drives the entire Hyperliquid ecosystem.

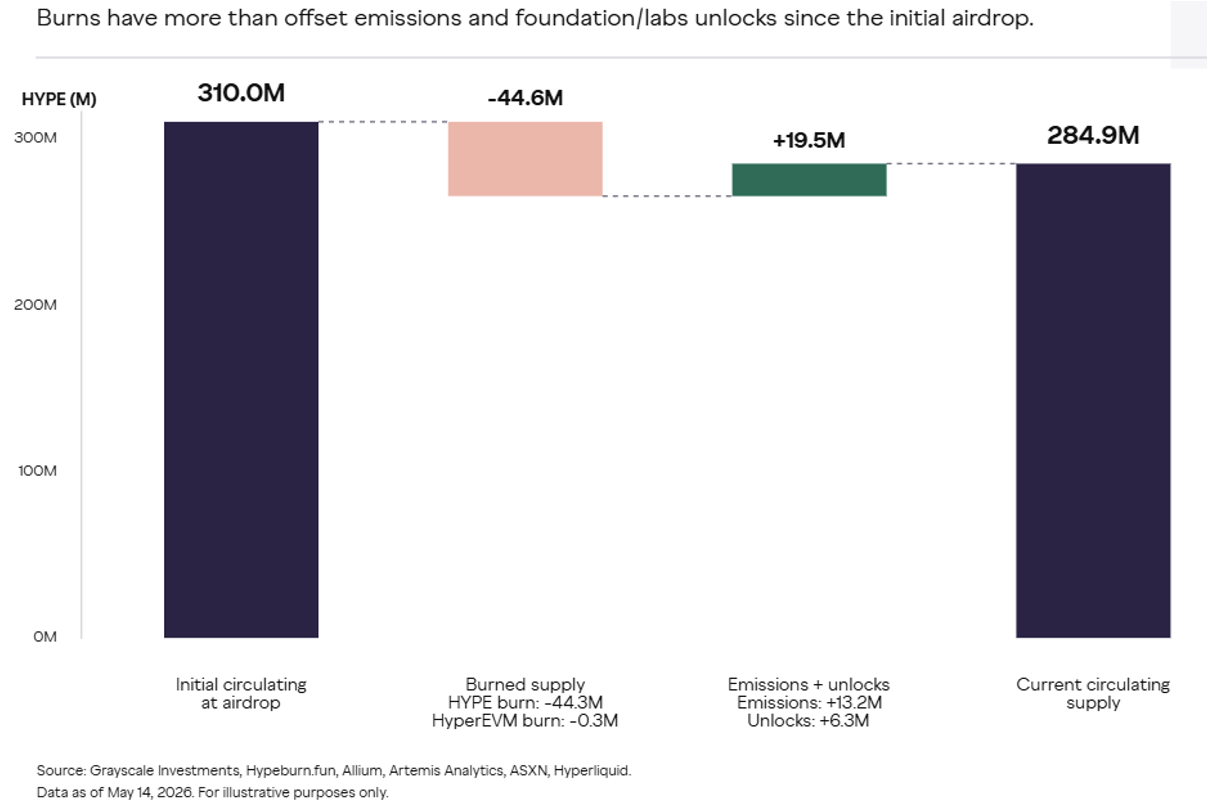

The project did not have traditional venture capital and airdropped about 30% of the token supply to early users. This determined who cared about HYPE: the initial holder base heavily skewed towards users, traders, and community members who already understood the product.

The value of HYPE comes from transaction fees and utility. Hyperliquid Labs confirms that 99% of the fees go into an assistance fund, which converts the fees to HYPE and burns the acquired HYPE. Token burning is similar to stock buybacks in the traditional stock market. As the amount burned exceeds the newly issued amount, the circulating supply of HYPE has been consistently decreasing.

Use cases of HYPE within the ecosystem include:

Staking and Validator Participation: HYPE secures network safety through validator staking.

Gas Fees: It is the native gas token of HyperEVM, where the base fee and priority fee of HyperEVM are both burned.

Fee Discounts: Staking HYPE can reduce transaction fees.

Market Creation Collateral: HIP-3 deployers must maintain a stake of 500,000 HYPE to operate the perpetual contract market deployed by the builder, which serves as both interest-staked capital and security for market quality. The result market of HIP-4 has already launched, and if permissionless deployments adopt a similar model, it could further deepen HYPE's role.

The HYPE token is tied to a venue with existing measurable trading activity, fees, and developer demand. The more transaction volume the venue processes, the more important the fee schedule, staking levels, builder economy, and treasury fund mechanism become. As HyperEVM, HIP-3, and HIP-4 expand the platform boundaries, the utility and potential value accrual of HYPE increase.

Valuation Space

Hyperliquid is a unique platform offering a range of financial services, which poses a challenge in effectively evaluating its upside potential. However, based on reasonable comparables, Grayscale believes both the platform and the token have substantial growth potential.

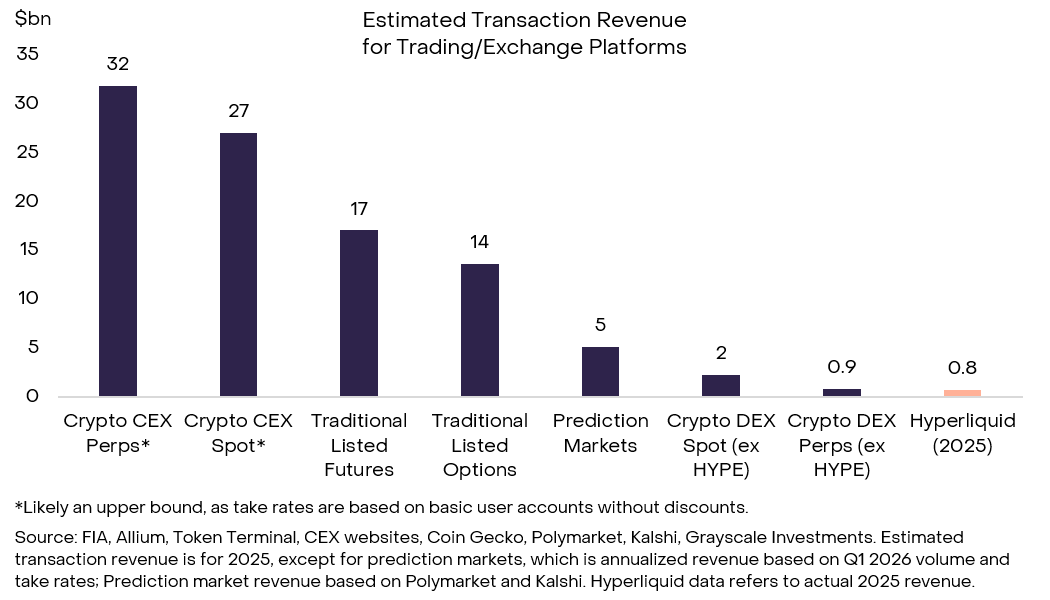

The following chart compares Hyperliquid's revenue to a range of trading platforms, including centralized cryptocurrency exchanges, traditional spot and derivatives trading platforms, and prediction markets. Hyperliquid's projected $800 million revenue in 2025 is significant, but represents only about 2% of the total trading revenue in the crypto perpetual contract space.

If Hyperliquid's non-crypto products continue to gain adoption, it could tap into a broader derivatives trading platform industry's annual revenue pool of around $350-400 billion.

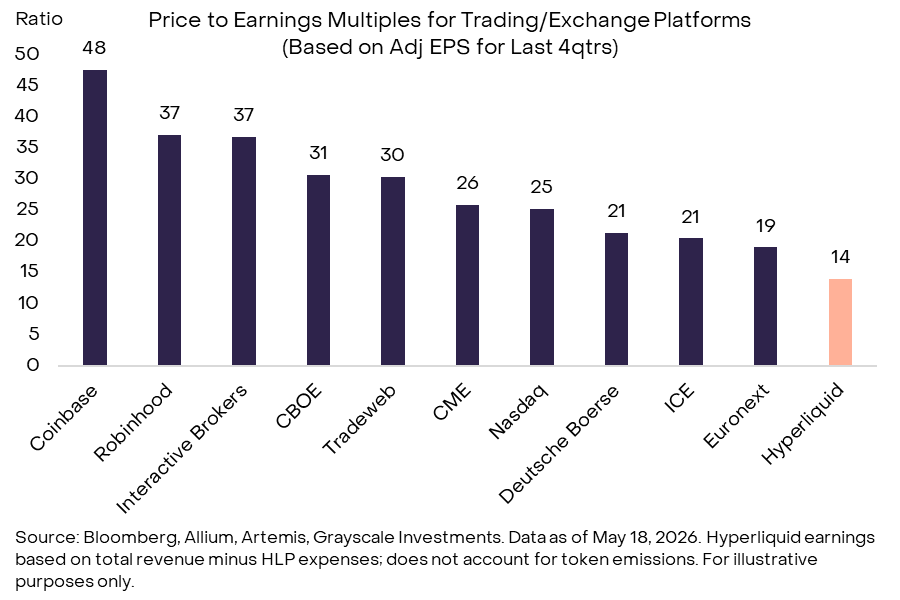

HYPE is not a stock, but can be roughly compared to traditional stocks in related industries. Based on earnings for the four quarters ending Q1 2026, HYPE's current valuation multiple is approximately 14 times.

Valuation multiples for publicly traded trading platform companies vary significantly, but high-growth companies like Interactive Brokers and Robinhood trade at multiples of 35-50 times.

U.S. Regulation: Perpetual Contracts on the Horizon

Hyperliquid sits at the intersection of two regulatory blank spots in the U.S.: perpetual contracts and decentralized trading platforms. Both areas are now moving towards clearer frameworks.

Perpetual futures have never been practically available in the United States. They have not been explicitly prohibited, but they do not cleanly fit within the framework of the Commodity Exchange Act (CEA). The CEA is a federal regulation that governs commodities and derivatives, with explicit requirements for clearing, margin, and registered trading venue enforcement.

This ambiguity has led to enforcement actions against centralized and DeFi platforms and explains why Hyperliquid operates overseas and geofences U.S. users.

However, the situation is rapidly evolving. The recent statements from the CFTC, along with actions by companies like Coinbase, Kraken, Robinhood, and Kalshi, indicate that regulatory agencies are actively pushing to enable quasi-perpetual futures products within a compliant framework.

A key legal issue is the classification question: are perpetual futures considered futures or swaps under the CEA? How regulatory agencies choose to clearly define this classification (through rulemaking, guidance, or non-enforcement relief) will determine the timing and persistence of market access.

In the short term, regulatory progress may prioritize benefiting centralized registered trading venues. But in the medium term, CFTC rulemaking, guidance, or non-enforcement relief could pave the way for Hyperliquid to offer compliant perpetual futures products in the U.S., reducing reliance on purely overseas access.

Simultaneously, the quasi-trading platform features of Hyperliquid directly involve it in the debate over how DeFi protocols are regulated. The U.S. currently lacks a rulebook specifically designed for DEXs. Regulatory agencies apply existing SEC and CFTC frameworks based on functionality, with the core principle being "decentralization does not equal exemption."

For derivative-centric DEXs, this means stricter scrutiny and explicit barriers to institutional participation—current institutional participation is mainly through intermediaries or offshore channels. Pending legislation like the CLARITY Act aims at a more structured, role-based digital asset market framework, with clearer distinctions between protocol layer activities, front-end operators, intermediaries, and registered trading venues.

This distinction is crucial for Hyperliquid: as a non-custodial infrastructure, its core protocol may ultimately receive regulatory treatment different from the interface or entity facilitating user access.

These proposals have not yet created a fully viable regime for on-chain perpetual futures, but they represent a path toward that goal—especially if accompanied by targeted safe harbor provisions, clearer definitions of brokers, and rules tailored for on-chain market structures (such as margin, funding rates, and 24/7 trading). The regulatory direction is to enable innovation within guardrails, and Hyperliquid's positioning—open, global, non-custodial—is aligned with the policy discussions around retaining permissionless access while introducing appropriate market protections.

Risk

HYPE investors should be aware of both general risks and some risks specific to the Hyperliquid platform:

HYPE has an annualized price volatility of around 80%, approximately 40 percentage points higher than Bitcoin. The validator set of Hyperliquid is more centralized than other blockchain networks and operates on closed-source software.

Hyperliquid's growth potential partly depends on changes in U.S. financial services regulation. If regulation does not loosen, the platform may be limited to other jurisdictions, with a growth ceiling.

Conclusion

Hyperliquid has no direct counterpart in either crypto or traditional finance.

It presents a compelling vision for the future of blockchain finance: an open architecture platform, built on permissionless innovation, adhering to DeFi's transparency and self-custody principles.

At the same time, it is built around an optimized core application that has already demonstrated success with real user data. If it can continue to execute, retain and grow its community, and benefit from regulatory changes, Grayscale believes Hyperliquid has the potential to become a financial services giant.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia