A new IPO company's opening pricing on the US stock market, along with a weekend hunger for trading activity after the market closure, has led Hyperliquid to experience an epic price discovery. The all-time high of HYPE has caught the attention of global traders to this 24/7 platform and a team named TradeXYZ.

Hyperliquid is a high-performance blockchain designed for derivatives, with a fully on-chain order book. HIP-3 is its third improvement proposal: anyone can open their own perpetual contract market on this chain by staking about 500,000 HYPE as collateral, allowing trading of US stocks, indices, commodities, and even companies without an IPO. Hyperliquid provides matching, margin, and on-chain settlement, allowing deployers to define which trading pairs to list, which oracle to use, and how much leverage to offer.

TradeXYZ is the first trading platform deployed according to the HIP-3 framework. Through weekend market pricing and pre-IPO contract trading, TradeXYZ attracted Wall Street's attention in less than a year since its launch.

In addition to TradeXYZ, several other HIP-3 trading platforms have been deployed successively, attempting to replicate the success of HIP-3 through their respective advantages.

However, the results have been disappointing.

Recently, the Hyperliquid ecosystem project Felix announced that its HIP-3 trading platform will start to shut down on June 19th, with all markets being liquidated one by one.

Felix is the first HIP-3 trading platform deployed on Hyperliquid for silver and oil trading pairs. The OIL, GOLD, and SILVER three trading pairs brought it considerable transaction fees and around $3 billion in trading volume from December last year to January this year. Now, it has become the first HIP-3 deployer to officially exit.

Why would a once-leading player be the earliest to close its doors?

「We are not TradeXYZ」

Felix's founder, 0xBroze, reviewed this failed attempt.

Firstly, the choice of quote assets was wrong. For HIP-3 trading platforms to provide perpetual contracts, a stablecoin must be selected. TradeXYZ, the earliest platform to go live, chose USDC. At that time, this was not a well-thought-out decision as Hyperliquid had not yet launched a stablecoin bidding process. In contrast, Felix launched later and chose USDH, a natural decision to secure fee discounts by using USDH.

However, what they didn't expect was that later on, Hyperliquid entered Growth Mode, significantly reducing transaction fees. The advantage of USDH almost disappeared, instead becoming a "burden of liquidity fragmentation." Users holding USDC had to convert to USDH in order to use Felix, but liquidity providers were reluctant to support USDH-related markets. In hindsight, 0xBroze viewed USDH as more of a pawn that Hyperliquid used to pressure Circle for profit sharing.

Secondly, TradeXYZ was the earliest player. It opened on the same day as HIP-3, about a month before Felix. This one-month gap was not just a difference in timing; the early arrival of the brand captured the users' mind share and had ample time to onboard the next wave of markets.

Furthermore, TradeXYZ had more trading pairs. As the only deployer using USDC, TradeXYZ quickly established a moat with its number of trading pairs. 0xBroze believed that this was mostly due to an advantage in the balance sheet. TradeXYZ could afford the auction fees for Tickers and liquidity costs. On the other hand, Felix's funds were limited, so they had to be more selective in opening trading pairs.

Lastly, there was the "airdrop hint." Early TradeXYZ users speculated that they would receive a token airdrop because the team behind TradeXYZ had previously won the on-chain Ticker UNIT auction on Hyperliquid. The expectation of an airdrop gradually boosted TradeXYZ's early user base, trading volume, open interest, and liquidity, creating a flywheel that Felix could never catch up to.

In summary: we failed because we were not TradeXYZ.

Matthew Effect

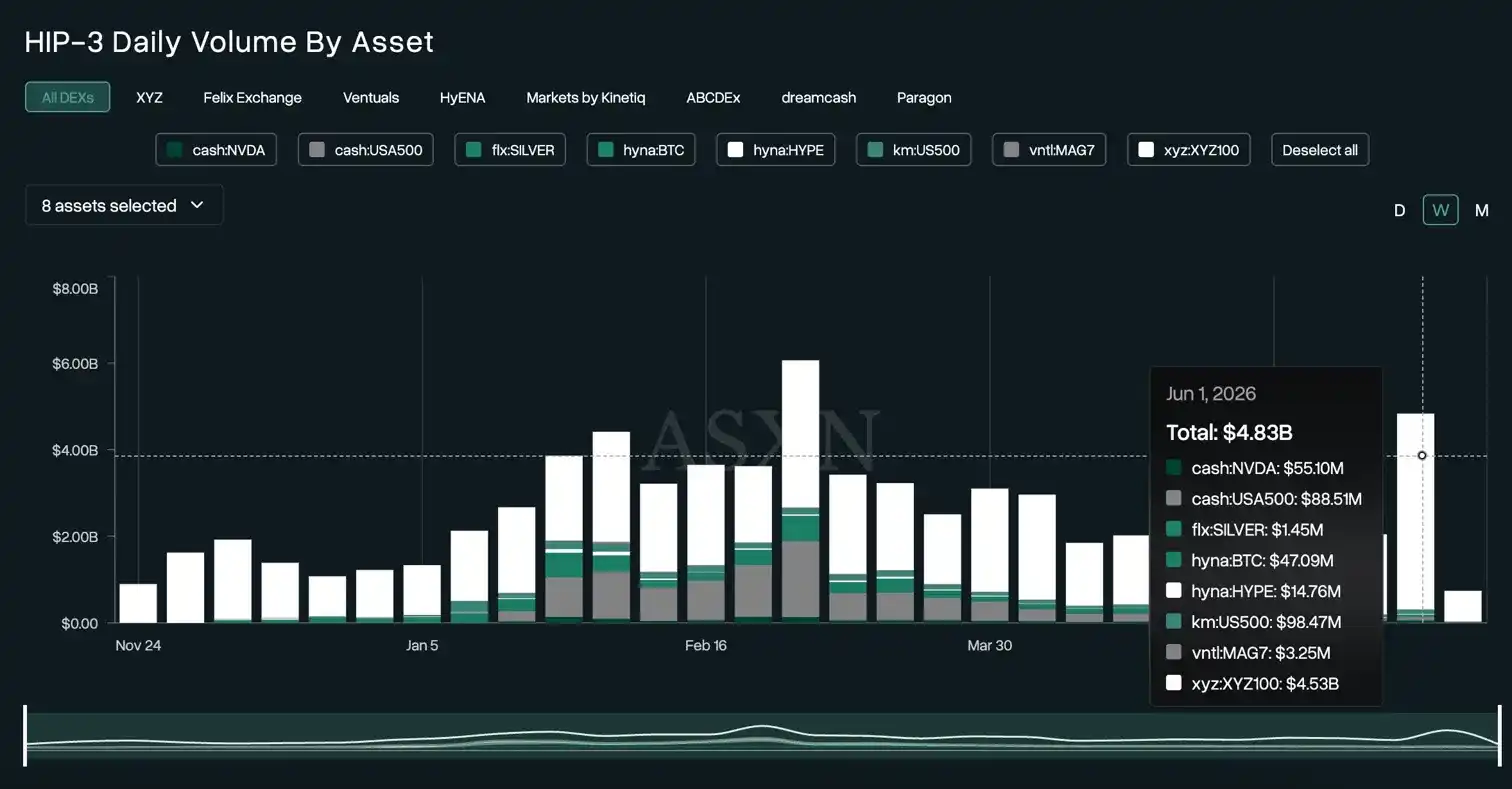

First, look at the trading volume. In the first week of June, TradeXYZ monopolized 95.85% of HIP-3's trading volume. The remaining 7 projects together accounted for less than 5%, with the second-place dreamcash at only 2.75%, the third-place Kinetiq Markets at 0.64%, and HyENA at 0.49%.

The concentration of open interest contracts is even higher, with TradeXYZ holding 96.81%.

This monopolistic situation has been persistent. From the launch of the HIP-3 proposal last October to this May, TradeXYZ's trading volume has never been below 60%.

In the first week of June, the total trading volume of HIP-3 was $4.8 billion, with TradeXYZ's XYZ100/USDC pair contributing $45.3 billion.

High Costs, Low Returns

To understand why other deployers are struggling, one must break down the costs of running a HIP-3 trading platform.

There are two clearly itemized costs. Deploying a HIP-3 trading platform requires a deposit of 500,000 HYPE tokens, equivalent to around $30 million (calculated based on a $60 HYPE price).

The second cost is the Ticker auction. For each new trading pair listed, a Ticker must be acquired through auction, with an average auction price of around 500 HYPE, approximately $3,000. Currently, this auction market is also monopolized by TradeXYZ, and since February, non-TradeXYZ players' enthusiasm for participating in the auction has waned.

Running a HIP-3 trading platform is not only costly but also yields slim profits.

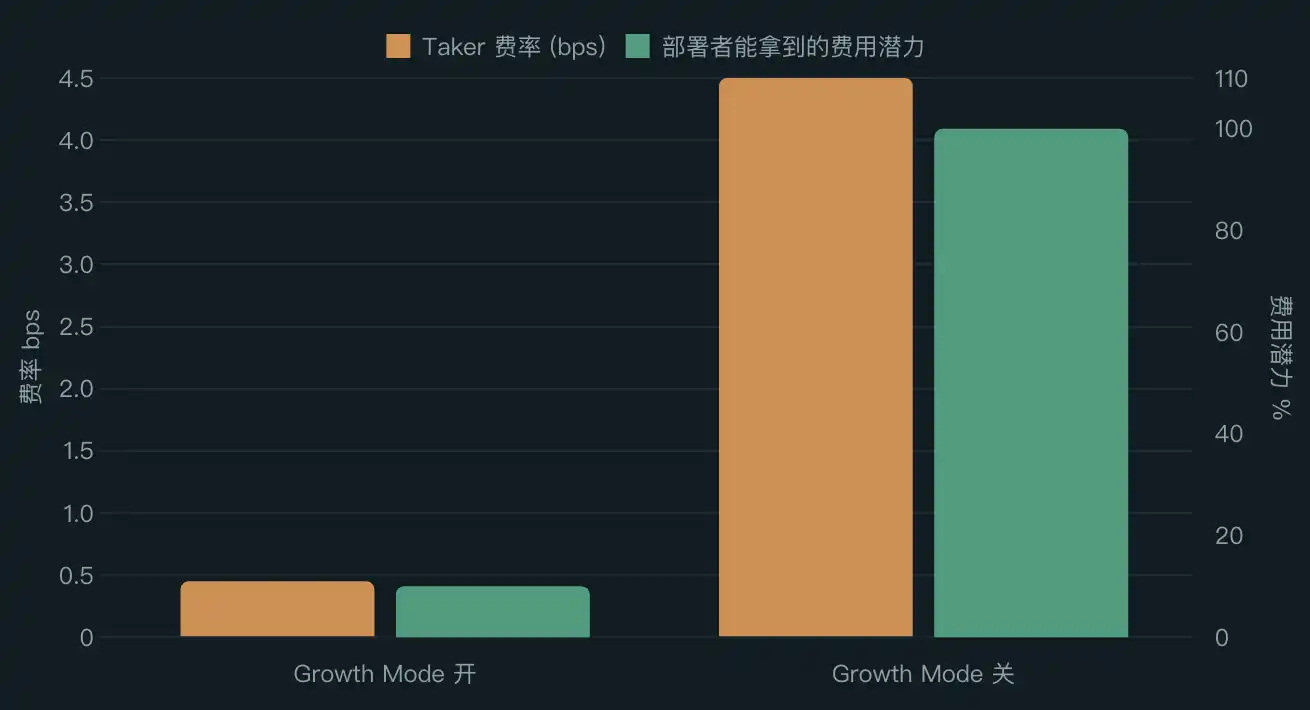

In order to align their perpetual contract fees with traditional brokerages, Hyperliquid introduced the Growth Mode. When Growth Mode is activated, the Taker fee is slashed significantly, making it cheaper for users to open an NVDA position here than at Interactive Brokers. The trade-off is that deployers only receive about 10% of the potential fee revenue.

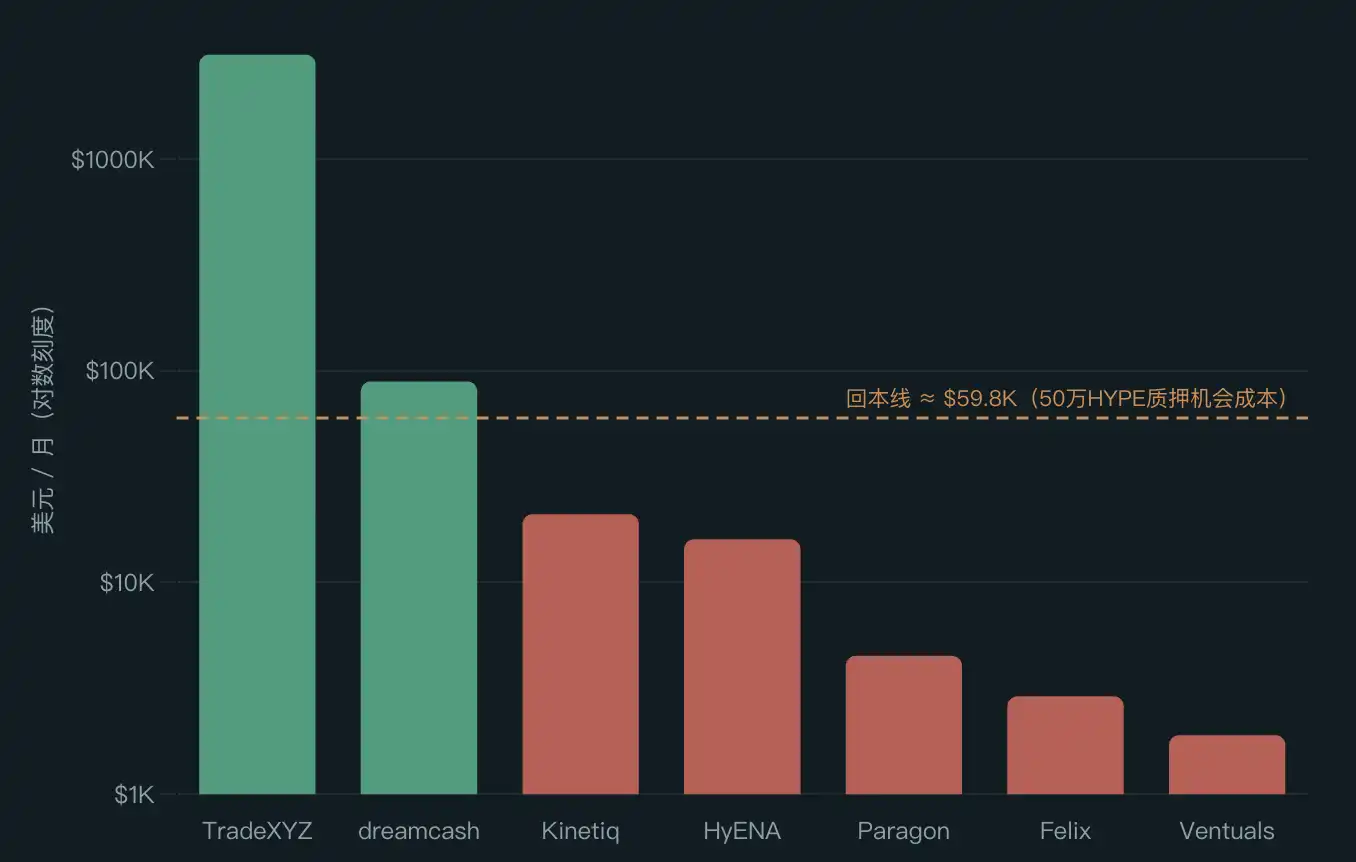

If a deployer chooses not to launch a trading platform and instead stakes 500,000 HYPE, earning approximately a 2.3% annualized staking reward, they would receive about $60,000 per month. In other words, the opportunity cost of launching a trading platform, just to break even with doing nothing, would require a monthly fee revenue of over $60,000.

Here is the revenue situation for various trading platforms in May: TradeXYZ generated around $3.1 million, dreamcash around $89,000, Kinetiq around $21,000, and HyENA around $16,000. The following platforms each generated less than $5,000.

Except for TradeXYZ, only dreamcash barely reached the break-even point. All other deployers did not even cover the opportunity cost of the 500,000 HYPE. This calculation does not even include expenses such as providing liquidity, oracle services, team salaries, and liquidity incentives, which are more challenging to quantify.

Realities

The remaining trading platforms each have their own way of surviving.

The quoted asset of dreamcash is USDT0, backed by Tether. Tether provides approximately $200,000 in weekly trading incentives, translating to around $867,000 per month, far exceeding the platform's fee revenue. Coupled with the expectation of airdrops, dreamcash firmly holds the second position in trading volume.

Kinetiq Markets has an innovative "crowdfunding mechanism." Kinetiq has developed a platform called Launch. Founder Omnia describes it as a combination of "Shopify + Kickstarter," allowing others to deploy their own custom HIP-3 trading platform using crowdfunding to obtain 500,000 HYPE. Markets itself serves as a template for this model, demonstrating that the Launch model can work, instead of competing directly with TradeXYZ for trading volume.

The Road Ahead

Felix will certainly not be the last HIP-3 trading platform to shut down. This is because there is not much room for adjustment left for other players.

Perhaps one could explore a niche or emerging market that TradeXYZ is not willing to touch. However, Felix has already validated for everyone that this path leads to a scenario where "once volume is generated, TradeXYZ will replicate and extract value."

Alternatively, one could seek a different distribution channel, establish their own user base in untapped markets, bypassing the Hyperliquid-native traders' saturated market. Kinetiq's Launch is an attempt in this direction, but it has not gained traction yet.

If the cost barrier remains rigid, the current market monopoly is likely to persist.

There have been suggestions within the community to reduce the 500,000 HYPE staking threshold and set an auction price that fluctuates with the HYPE price but at a lower rate. From this perspective, a decrease in the HYPE price may not necessarily be a bad thing, as it would enable more projects to build on Hyperliquid at a lower cost.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia