According to Nikkei Asia, the Bank of Japan (BoJ) is expected to raise the short-term policy rate from 0.75% to 1.0% at its monetary policy meeting on June 15-16, marking the highest policy rate level since 1995.

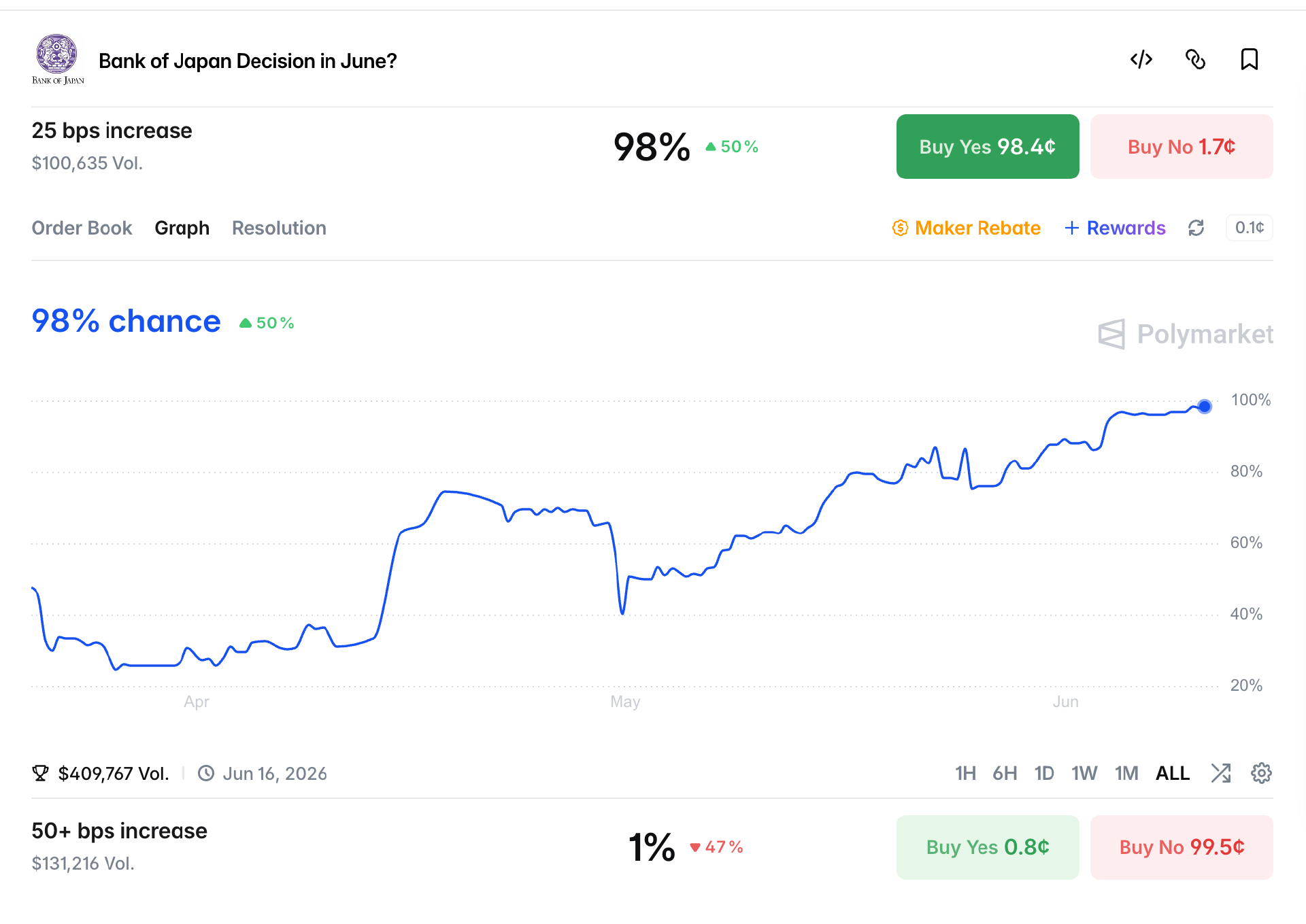

Currently, the market has priced in a high probability of a rate hike, with the probability of a "25 bp (basis point) rate hike" on PolyMarket soaring from 25% in early April to 98%.

With the BoJ rate hike imminent, a large number of investors engaged in yen carry trades may be forced to sell off foreign assets, convert back to yen, and repay loans, triggering a chain reaction that could amplify global risk asset volatility—similar to the flash crash of August 2024, when the yen's sharp surge led to a short-term global stock market slump and a nearly $20,000 single-day drop in Bitcoin, marking a 15% decline.

1. Inflation Risks Drive BOJ Rate Hike

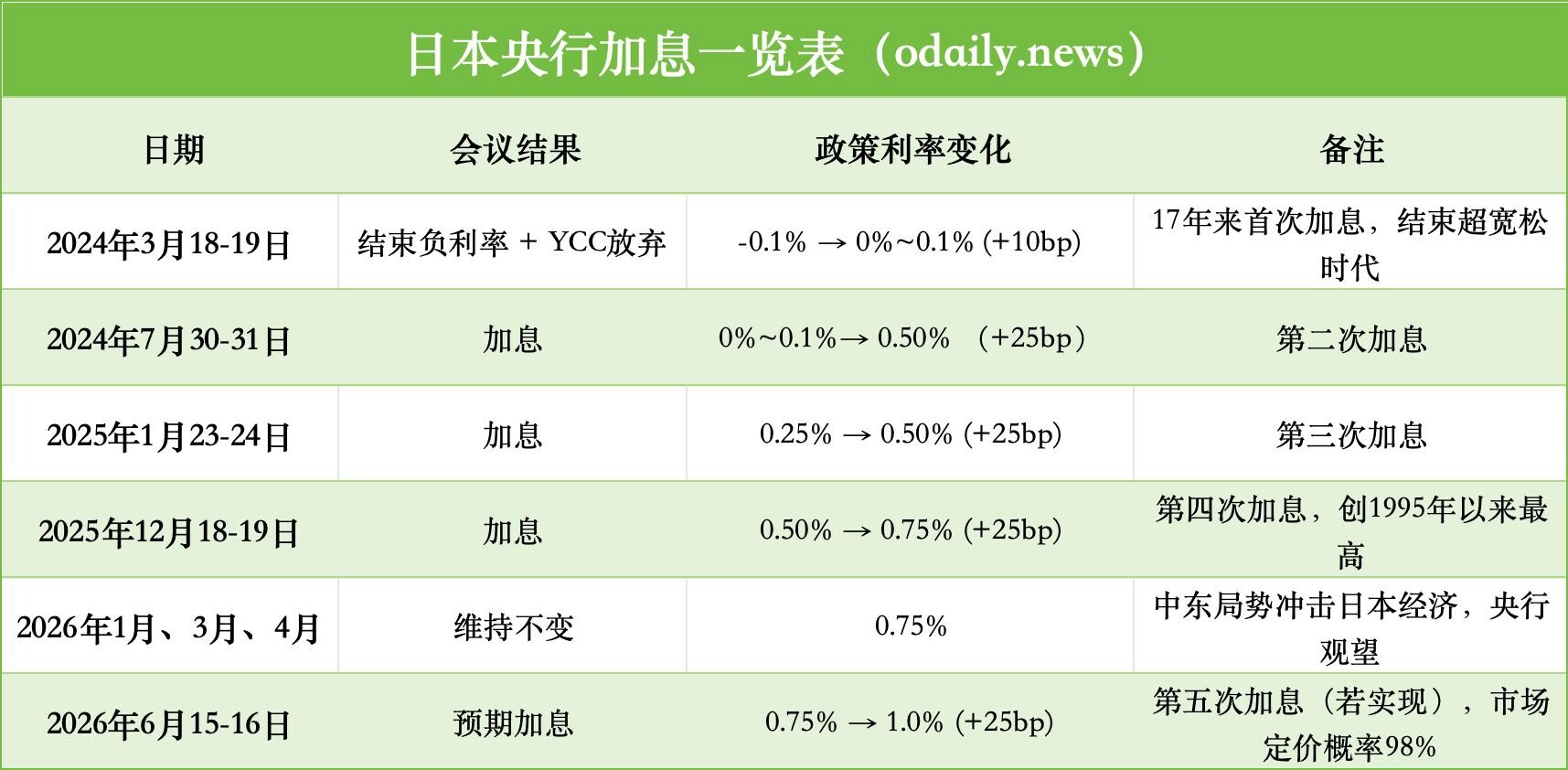

Over the past two years, the hawkish voices within the BoJ have grown stronger, culminating in the end of the 17-year-long negative interest rate policy in March 2024, when the policy rate was raised from -0.1% to a range of 0% to 0.1%, marking the first rate hike in this cycle.

In July 2024, the BoJ hiked rates by another 15 bps to 0.25% and announced a gradual balance sheet reduction; in January and December 2025, rate hikes of 25 bps each raised the rate to 0.75%; and in the first three meetings of 2026, the rates remained unchanged. Below are the rate hike details from several BoJ meetings:

After keeping rates unchanged for half a year, why did the BoJ eagerly embark on a new round of rate hikes? This rate hike is mainly driven by two factors.

First, there is an energy shock and input inflation pressure. With the Middle East conflict causing oil price fluctuations in the first half of the year, Japan, as a country highly dependent on imported energy, has seen a significant rise in import costs. The May Corporate Goods Price Index (CGPI) rose by 6.3% year-on-year, the fastest pace since 2023, with petroleum products up by 9.6% and utilities up by 8.5%. The BoJ expects the core CPI for fiscal year 2026 to rise to 2.5-3.0%, well above the 2% target.

Second, the yen's weakness has intensified import-driven inflation. The current USD/JPY exchange rate continues to hover around 158-160, nearing the historical extreme weakness range. The significant depreciation of the yen has directly reduced Japanese companies' purchasing power for imports, leading to a significant rise in the cost of imported commodities such as energy and raw materials, further driving up domestic price levels.

Although the Japanese Ministry of Finance has intervened in the foreign exchange market several times, the effect has been limited and difficult to sustain. This situation is now forcing the BOJ to tighten monetary policy (i.e., raise interest rates) at the June meeting to prevent runaway inflation expectations.

BOJ Governor Haruhiko Kuroda, in a speech on June 3, explicitly shifted to an anti-inflation narrative, emphasizing that if the upward price risk exceeds the downside economic risk, the pros and cons of raising interest rates must be discussed.

Reuters, citing three sources familiar with the matter, reported that unless there is a sharp escalation in the Middle East conflict, the BOJ will raise interest rates in June and may slow the pace of bond tapering to maintain market stability. Bloomberg and ING, among other institutions, hold similar views and expect the BOJ to raise rates by a total of 50 basis points in 2026.

This series of changes marks Japan's transition from the "world's last lender" to a normalized central bank, posing a direct challenge to global assets reliant on cheap yen financing.

Second, unwinding of yen carry trades leads to continued liquidity tightening

The Bank of Japan has long maintained an ultra-loose monetary policy, and yen carry trades have been a significant part of global liquidity for over a decade. Investors borrow yen at near-zero interest rates and invest in high-yield assets such as US stocks, tech stocks, emerging markets, cryptocurrencies, etc., to earn carry and capital gains.

The BOJ's upcoming interest rate hike will directly increase the yen's funding costs and may trigger yen appreciation (USD/JPY downside), forcing leveraged investors to unwind their positions, creating a feedback loop: Yen appreciation leads to expanded exchange losses → Increased funding costs → Investors forced to deleverage → Massive selloff of risk assets → Further asset price declines → More stop-losses triggered → Intensified liquidation pressure.

Historically, every signal of BOJ policy tightening has caused severe market volatility.

On July 31, 2024, the BOJ raised rates by 15 basis points to 0.25% and announced a gradual tapering of its balance sheet, coupled with weak US employment data, triggering intense global market turmoil.

At that time, both major South Korean indices (KOSPI and KOSDAQ) plummeted, triggering circuit breakers; Japanese stocks crashed, with the Nikkei 225 plunging 12.4% in a single day, accumulating a weekly decline of over 20%, marking the worst performance since 1987; global stock markets fell collectively, with US and tech stocks adjusting simultaneously, and the VIX fear index soaring.

The crypto market has also been hit hard, with Bitcoin and ETH plummeting over 30% in just one week, leading to a surge in liquidations.

According to Morgan Stanley's estimate, despite a significant amount of positions being gradually unwound since 2024, there is still around $500 billion of outstanding yen-denominated funding positions in the market. Although the market has already priced in some of the risks, these positions still pose a significant threat. Morgan Stanley has warned that a rapid yen appreciation could trigger a chain reaction of liquidations, especially impacting high-leverage assets during periods of thin liquidity.

J.P. Morgan's Global Market Strategist, Dubravko Lakos-Bujas, and FX Strategist, Meera Chandan, have both pointed out that the policy divergence between the BOJ and the Fed will exacerbate the instability of arbitrage unwinding, potentially leading to a global repricing of risk assets.

III. Global Risk Assets Wounded, U.S. Stocks and Crypto Market Not Spared

The AI-driven tech frenzy was the main theme of the U.S. stock market in the first half of 2026, with Nvidia, Broadcom, and other chip stocks, as well as mega-cap cloud service providers, leading the Nasdaq to record highs.

However, as June began, the market saw significant rotation and pullback, especially on June 5th, when U.S. stocks experienced their most severe single-day pullback of 2026.

The Nasdaq plummeted by 4.18%, marking the largest single-day decline since April 2025; the S&P 500 fell by 2.64%, ending its nine-week consecutive gains record; the Dow dropped by 1.35%, with the Philly Semiconductor Index plunging over 10%, led by AI core stocks such as Nvidia, Broadcom, Micron, and Marvell.

The pullback in U.S. stocks is influenced not only by macro-level geopolitical tensions and Fed policy uncertainty but also by the potential interest rate hike impact from the BOJ.

Firstly, liquidity tightening will directly impact overvalued growth stocks. AI companies have massive capital expenditures and rely heavily on cheap financing. Unwinding of yen carry trades will reduce global risk-on fund inflows, hitting high-beta tech stocks the hardest.

Leading semiconductor companies like Nvidia and Broadcom, as well as hyperscalers like Meta and Microsoft, are highly sensitive to valuation changes and are prone to sell-offs. An analysis by Investing.com indicates that the high-growth, high-valuation sector is most sensitive to global liquidity shifts, often experiencing rapid deleveraging once arbitrage unwinding kicks in.

Secondly, the rising energy cost will significantly squeeze AI profit margins. The Middle East conflict has pushed up oil prices, leading to a sharp increase in data center power and cooling costs. Together with the BOJ rate hike, it has created a "stagflationary" macro environment, severely testing the sustainability of the AI business model.

BitMEX co-founder Arthur Hayes explicitly warned in his latest article "Reality Test": "The energy reality is testing the market's current 'dream' state." High oil prices not only raise operational costs but may also slow down enterprise token usage growth, further affecting AI-related revenue expectations.

Lastly, there is the impact of massive IPO supply and political regulatory risks. Giants such as SpaceX, Anthropic, and OpenAI plan to go public intensively in the second half of 2026, with valuations often exceeding one hundred times their revenue, and the unlocking of lock-up periods will bring massive supply pressure. Meanwhile, Trump may shift towards anti-AI measures for the midterm elections, increasing regulatory uncertainty.

Cryptocurrency, as the highest beta global risk asset, is even less optimistic. On one hand, the yen rate hike leads to increased financing costs, directly driving up global leverage trading costs and forcing massive liquidation of crypto leveraged positions. On the other hand, in competition with AI for liquidity, AI capital expenditure has absorbed a large amount of market funds, leaving crypto behind. BOJ actions will further tighten marginal liquidity.

Yahoo Finance analyst Lockridge Okoth stated that a 98% probability rate hike could trigger the next round of Bitcoin liquidity shock. An analysis by Investing.com pointed out that the appreciation of the yen and the weakening of BTC often exhibit a high degree of synchrony, serving as a typical signal of global risk aversion.

Arthur Hayes has also emphasized in multiple analyses that the dynamics of yen carry trades remain one of the key variables affecting Bitcoin liquidity, reminding investors to pay attention to short-term liquidity shocks triggered by policy signals. In recent articles, Arthur Hayes emphasized the need to beware of the combined impact of short-term energy costs and currency policy risks; BTC/ETH may adjust in the short term with risk assets but will depend on the reboot of liquidity in the long term.

Closing Words:

The renewed BOJ rate hike concerns are not an isolated event but a signal of global liquidity tightening. Especially with multiple factors such as the ongoing Middle East geopolitical conflict driving up oil prices, AI capital expenditure consuming liquidity, and Fed policy uncertainty compounding, the buffer space has been further compressed.

For investors, in the short term, global risk assets, particularly high-leverage, high-valuation sectors (AI tech stocks and cryptocurrency), may face significant pressure for a pullback. Volatility will noticeably increase, requiring a high level of vigilance and attention to leverage risks.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia