TL;DR

· Oracle reported strong earnings and cloud business guidance, but the stock dropped over 10% in after-hours trading as the market feared the high cost of AI infrastructure.

· The demand is still there, but the issue has shifted to how much free cash flow can remain after orders flow through data centers, GPUs, power, and financing costs.

· Related Tickers: ORCL, NVDA, MSFT, AMZN, GOOG, META, QQQ, and potentially IPO-bound OpenAI, Anthropic, SpaceX.

This Oracle earnings report is nearly everything AI bulls wanted to see.

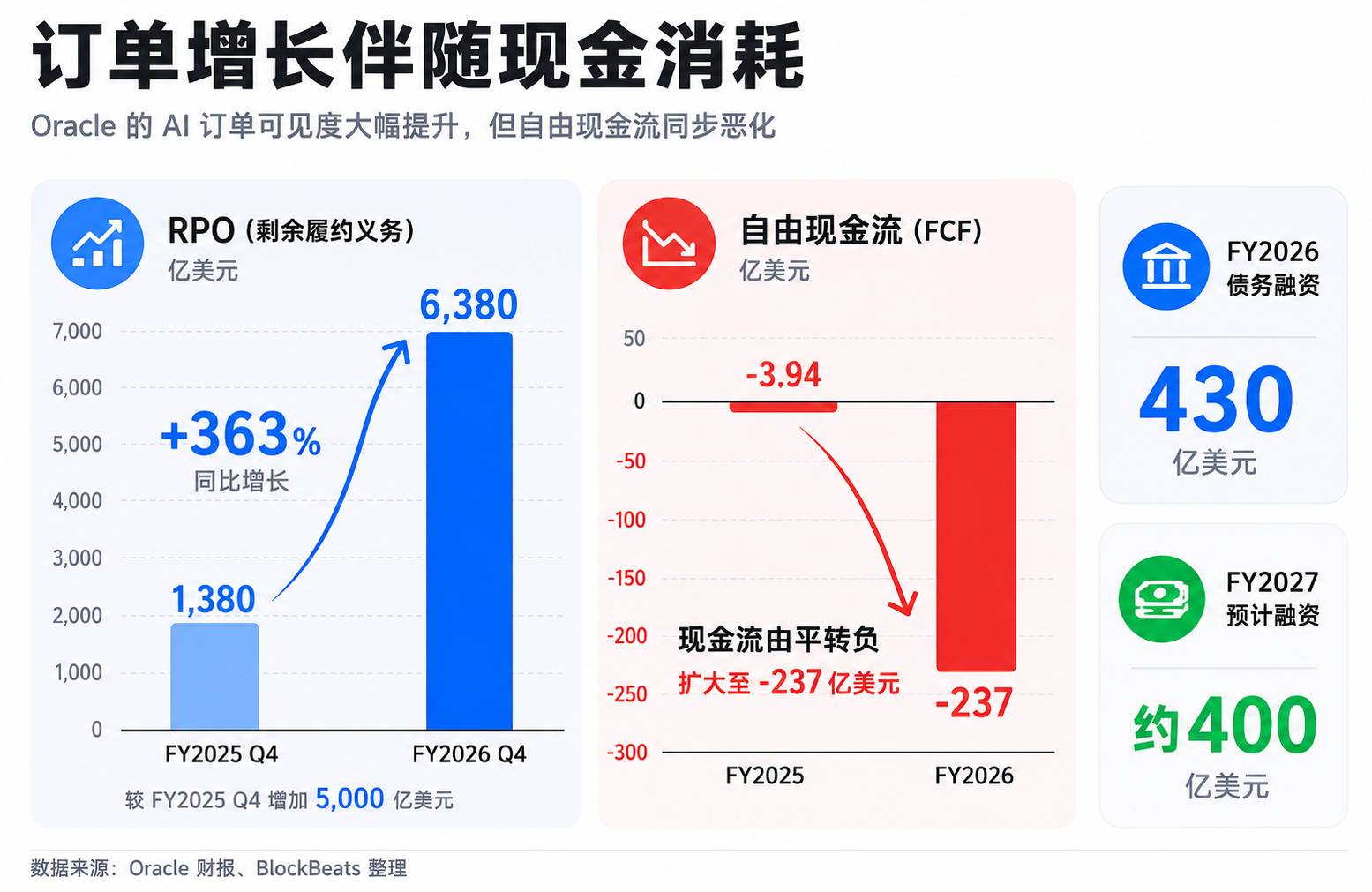

According to Oracle's official financials, Q4 FY2026 revenue was $19.2 billion, cloud revenue was $9.9 billion, IaaS revenue was $5.8 billion, up 93% year over year. Remaining performance obligations (RPO, contracted not billed) increased from $553.0 billion to $638.0 billion. The company's guidance for Q1 FY2027 was also strong, expecting total revenue to grow 27% to 29% year over year, with cloud revenue growing 57% to 63% on a constant currency basis. The full-year revenue guidance is $90.0 billion.

However, the market's initial reaction was not a reward but a sell-off. Oracle's stock price dropped from around $205.11 in the post-market to touch $177.52, a maximum decline of about 13.5%.

This AI trade's most notable change is right here: the company talks about growth, but the stock price asks about payback.

Over the past two years, the market has been willing to pay a premium for "How big is the AI demand." Growth in cloud revenue, AI chip orders, GPU purchases, and model collaborations could all be reasons for a valuation uplift. Oracle's response this time indicates that the same set of good news is being recalculated by the market using a different formula: how much money does the company need to spend upfront to get the order? How much debt to take on? Should there be an equity issuance? How soon after data center delivery will they be at full capacity? When will gross margins and free cash flow catch up?

The AI demand is still there, but AI trades are transitioning from "Who gets the order" to "Who can book it."

Good Earnings Trigger Financing Concerns

If we only look at the revenue side, Oracle doesn't seem like a troubled company.

Q4 revenue beat market expectations, cloud revenue continued to grow, especially with strong IaaS growth. The significant increase in RPO has also enhanced visibility into future revenue. For a company shifting towards AI cloud infrastructure, this type of data should have supported the narrative of "real demand."

The company's guidance is equally aggressive. Both next quarter's revenue and cloud business are expected to maintain high growth, with a target of $900 billion in total revenue for the 2027 fiscal year. The earnings call and media briefing also mentioned large AI infrastructure contracts, data center delivery progress, and hints of customer collaboration such as OpenAI. Customers have not stopped placing orders, and the demand for AI computing power has not suddenly disappeared.

The market is now not only looking at the size of orders but also at the capital expenditure behind those orders.

AI cloud is not a light asset software business. Oracle needs to meet the needs of cutting-edge model companies and large enterprise customers, which requires building data centers, procuring or accessing GPUs, configuring networks, power, cooling systems, and investing a significant amount of cash upfront before customer revenue is fully realized. The larger the order, the more visible the future revenue, and the heavier the upfront investment.

This is the reason for "good news turning into a sell-off reason." RPO growth indicates future work to be done and also requires the company to build capacity. High cloud revenue growth demonstrates strong demand while also reinforcing the market's expectation of continued capital expenditure. Investors are starting to translate the same set of data into another question: Does this company need to have a heavier balance sheet to achieve this growth?

Oracle's official disclosure states that the free cash flow for the 2026 fiscal year was -$23.7 billion. The company completed $43 billion in debt financing and $5 billion in equity financing during the 2026 fiscal year. For the 2027 fiscal year, the company expects to raise approximately $40 billion through debt and equity financing, including the announced $20 billion ATM equity issuance plan, and stated that no more debt is expected in the 2026 calendar year.

There is also a piece of reverse information that needs to be included in the valuation framework. The company mentioned that part of the large AI contracts includes customers' prepayment or self-provisioned GPUs totaling $75 billion, which can reduce the capital Oracle needs to raise on its own. In other words, the pressure is not "Oracle fronting all the money," but the market needs to confirm: after deducting customer prepayments and self-provisioned hardware, whether the remaining financing, depreciation, and operational burdens on the company are still too heavy.

Growth still holds value, but the market is beginning to demand proof that the value of growth exceeds the cost of growth.

AI Infrastructure Resembles a Power Plant More Than Software Subscription

One of the easiest misconceptions for investors when it comes to AI infrastructure is to view it as traditional software growth.

The ideal model for software companies is that after the product is developed, the additional customers bring relatively low marginal costs, and revenue growth can quickly translate into profit. AI cloud is more like a combination of a power plant, a highway, and a warehouse. Before customers actually use it, the company needs to have data centers, chips, power, and network infrastructure. After customers start using it, they also have to bear the costs of depreciation, maintenance, energy consumption, and upgrades.

This will create a timing mismatch: cash flow pressure appears first, profit realization comes later.

It can be understood as a restaurant receiving a large number of reservations, and then deciding to open more stores. The reservations indicate good demand, but opening a new store requires renting a place, renovation, purchasing equipment, and hiring staff. The more reservations there are, the faster the expansion, and the tighter the early cash flow. Only when the new store is full, table turnover is stable, and average spending covers rent and labor costs, these reservations will turn into profit.

An AI data center follows a similar logic, but with larger amounts, longer periods, and higher uncertainty.

Oracle is facing cutting-edge model companies and large enterprise clients. Their computational power needs may be very real and may also grow over the long term. However, infrastructure providers must make upfront investments: how many GPUs to buy, how much capacity to build, how much electricity to secure, and at what price to sign long-term contracts. If future utilization ramps up slower than expected, or if cloud service prices drop, or if electricity and hardware costs are higher than anticipated, today's seemingly attractive orders may not quickly turn into high-quality cash flow.

This is also why the market is particularly sensitive to capital expenditures.

Capital expenditure itself is not a bad thing. For cloud providers, expanding capacity is a necessary condition to seize the AI demand. NVIDIA, Microsoft, Amazon, Google, and Meta are all in the same chain: someone sells chips, someone builds clouds, someone trains models, someone embeds models in products. In the past, investors were willing to believe that the entire chain would benefit from the expansion of AI demand.

However, as capital expenditures grow, the market will begin to differentiate between "spending to buy growth" and "spending to buy profit."

If a company's data center quickly reaches full capacity, customers renew steadily, cloud gross margins improve, free cash flow rebounds, then high capital expenditure is locking in future profits. Conversely, if a company continues to increase investment but needs continuous financing to support expansion, and profits are eaten up by depreciation, interest, and operating costs, high growth will be discounted.

Oracle's recent decline fundamentally means that the market is reevaluating AI infrastructure from a "revenue story" perspective back to a "return on assets" framework.

The Public Market Begins to Reassess AI Assets

Oracle is not alone; it is just exposing a larger issue early: the public market is reevaluating the quality of AI assets.

In the past, AI transactions had a relatively simple order. Whoever is closest to computational power, whoever is closest to the model, whoever can secure enterprise AI spending should enjoy a valuation premium. NVIDIA became a core target due to GPU demand, cloud providers were revalued for handling training and inference demands, and software companies increased prices around AI functionality and subscriptions.

The sorting is now starting to refine. Investors are no longer just asking "Who has an AI story," but rather "Who can incorporate AI demand into the income statement and cash flow statement."

For NVIDIA, the market will scrutinize if customer capital expenditures are sustainable, as chip demand ultimately comes from cloud providers and AI model companies' budgets. For Microsoft, Amazon, Google, and Meta, the market will assess whether AI investments can translate into cloud revenue, advertising efficiency, subscription growth, or cost reduction. For infrastructure expanders like Oracle, the market's question is more direct: Can data center investments bring high enough utilization and return on investment.

This is also the reason why potential large IPOs will have an impact.

If large private companies like SpaceX, OpenAI, Anthropic, and others were to enter the public market in the future, they might not simply "siphon off" Nasdaq liquidity, as historically, the large IPO window has not shown a consistent pattern for tech stocks' performance. However, they will bring a reality check: the public market will see a new batch of highly valued, highly narrative-driven AI or tech assets whose path to profitability still needs validation.

When these assets are placed on the same shelf, investors will reassess. Buying shares of a listed cloud provider means buying more certain cash flow and platform capabilities. Investing in a model company means buying into a more advanced technology narrative and application entry point. Buying into an infrastructure company means buying the certainty of computing demand while also facing capital expenditure pressure. Investing in NVIDIA is a bet on the entire AI investment cycle continuing to lengthen.

If risk appetite is high, investors may simultaneously acquire all AI assets, believing they are on the same growth trajectory. Once interest rates, financing costs, or profit expectations change, the market becomes more selective. The higher the revenue certainty, the more stable the gross margin, the faster the cash flow improvement, the easier it is to maintain a valuation.

Oracle's counterintuitive decline occurred right in the middle of this transition. The AI trade is not over yet, but the phase of indiscriminately pushing valuations higher has become more fragile.

Next Step: Focus on Data Center Monetization

The recent sell-off of Oracle does not necessarily imply that the AI bubble has burst. Demand-side data remains robust, with cloud revenue, RPO, customer partnerships, and company guidance all indicating that the need for computing power by enterprises and AI model companies persists. More accurately, the market is now beginning to price demand and returns separately.

The most critical variable going forward is the utilization and profit margin post-data center delivery.

If the relevant project is delivered as planned, customer usage ramps up quickly, cloud revenue continues to materialize, and gross margin is not significantly eroded by electricity, depreciation, and operational costs, market concerns about high capital expenditure will be alleviated. Today's decline may only be a phase of revaluation: investors initially demand a higher risk premium, and then revalue the company after cash flow proof.

However, if subsequent financial reports show that revenue growth still relies on larger-scale capital expenditure, financing needs continue to rise, free cash flow improvement is slow, or equity financing brings dilution pressure, Oracle will not just be a stock issue but will become a sample of the AI infrastructure valuation framework change.

What investors need to look at next is not whether AI orders continue to increase, but how much cash flow remains after orders pass through the data center, GPU, electricity, and financing costs.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia