SpaceX is set to land on the NASDAQ tomorrow.

With a price of $135 per share, the company plans to issue approximately 556 million shares, raising around $75 billion at a valuation of approximately $1.75 trillion to $1.8 trillion. Market sources indicate a subscription demand of over $250 billion, nearly 4 times oversubscribed.

Goldman Sachs and Morgan Stanley are the two lead underwriters, with a total of 23 investment banks participating in the underwriting syndicate. Goldman secured the coveted "lead left" position, with its name on the top left of the S-1 cover page and serving as the actual bookrunner. Interestingly, despite Morgan Stanley's 15+ years of partnership with Musk, spanning from the Tesla IPO to fundraising for the Twitter acquisition, they are relegated to second place this time.

Barclays is in charge of distribution in the UK, Deutsche Bank and UBS cover the European continent, Royal Bank of Canada is handling Canada, and Mizuho is responsible for Asia.

Considering the fundraising size, this deal could bring Wall Street's underwriting fee pool to between $800 million and over $1 billion.

This offering did not have a "price range." SpaceX bypassed the traditional IPO roadshow and price discovery process, opting for a fixed price of $135 for direct subscriptions, with the book set to close between June 8 and 10, and pricing on June 11.

In terms of stock structure, SpaceX had previously received approval for a 5-for-1 stock split. After listing, Musk will still maintain high voting rights, while common shareholders will have economic exposure. There is no lock-up period on control rights, with insiders subject to a 180-day lockup period strategically scheduled around mid-December NASDAQ rebalancing, when passive funds will be compelled to buy significantly.

This IPO will issue approximately 556 million new shares, all entering the float post-listing, representing around 4.3% of the total company shares. 30% of these will be allocated to retail investors, totaling around $22.5 billion, triple the typical 5% to 10% allocation in large U.S. IPOs. Morgan Stanley's E*Trade platform will serve small to mid-size retail investors, Bank of America will cater to U.S. high-net-worth clients, and platforms like Fidelity, Robinhood, Charles Schwab, and SoFi have opened their subscription channels.

Will SpaceX Create a Liquidity Black Hole?

Intuitively, an IPO raising $75 billion with retail investors owning 30% of the new shares would inevitably draw liquidity from elsewhere.

Retail investors would have to come up with this cash from somewhere, and the most convenient option would be to sell off their stocks and crypto assets. With Bitcoin under pressure in recent weeks, some of this selling pressure may have originated from here.

So, does the IPO of a large tech company inevitably lead to a liquidity drain? Let's first look at a set of background data.

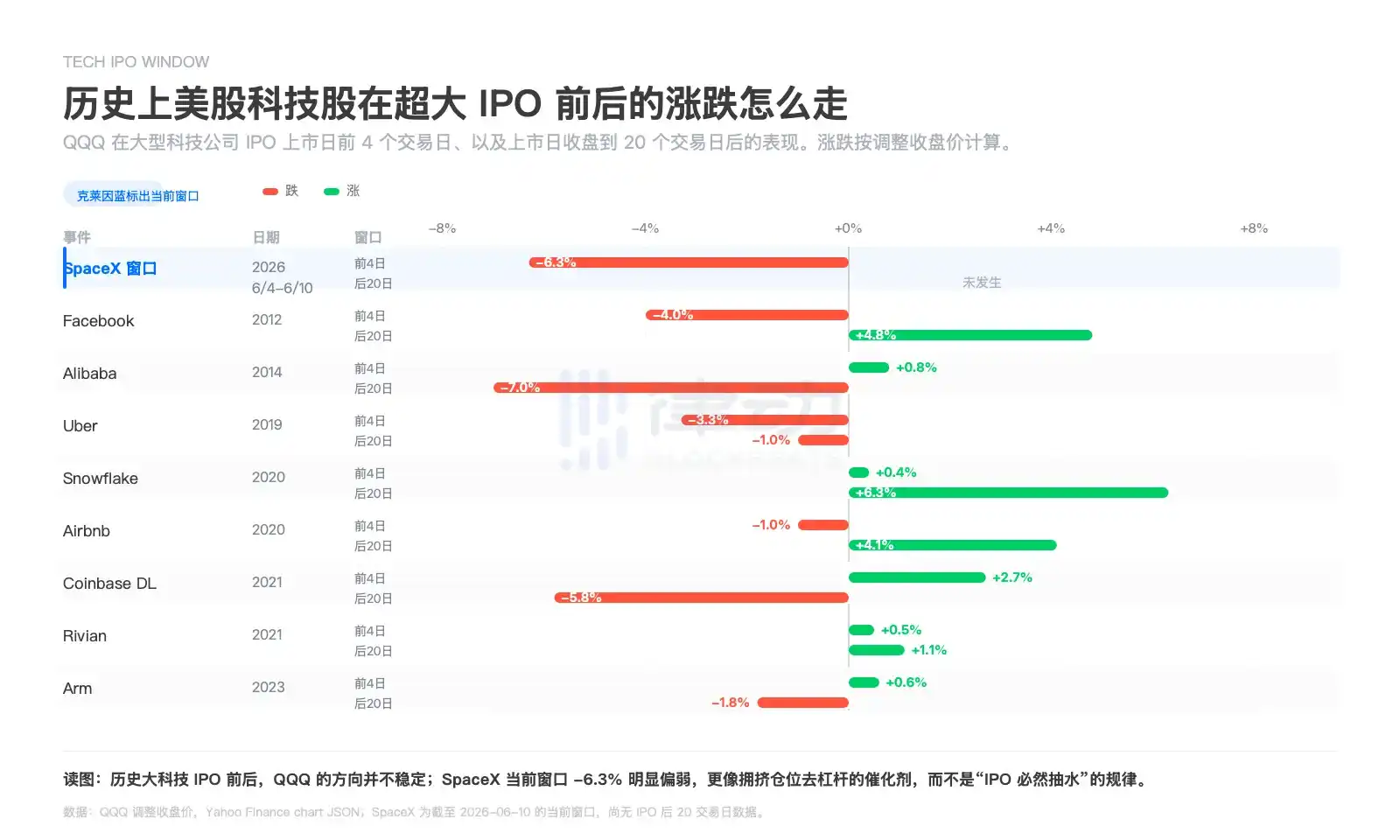

According to data, the performance of the Nasdaq ETF (QQQ) in the 4 trading days before and after the IPO of large tech companies and in the 20 trading days after listing shows a significant divergence.

Companies like Facebook, Snowflake, Airbnb, and Coinbase mostly saw positive returns in the 20 days post-listing, while Uber, some stages of Alibaba, Arm, and others showed weakness or significant volatility.

Current data from the SpaceX IPO simulation window shows a cumulative return of about -6.3% in the first 4 days, underperforming most historical samples.

Based on this set of data, our conclusion leans more towards: the IPO of a large tech company does not necessarily lead to a liquidity drain.

However, this does not mean that all assets are safe. SpaceX is likely to put pressure on the part of the funds that are most dependent on future risk appetite, such as tail assets and high-beta positions.

Andri Fauzan Adziima, Research Director at Bitrue Research Institute, refers to this pressure as an "IPO Tax".

Can Financial Data Justify the Valuation?

This is also the biggest point of contention for SpaceX's listing.

Public documents show that SpaceX is expected to have revenue of around $18.7 billion in 2025, with a net loss of about $4.9 billion. At a $1.75 trillion valuation, this translates to a market-sales ratio of about 94 times for 2025, for a company that is still incurring losses.

In terms of business structure, the connectivity services in which Starlink operates are closest to a mature listed company, with rocket launches providing deployment capabilities and a technological moat. What truly pushes the valuation ceiling higher is AI. Since SpaceX's $1.25 trillion post-merger valuation in February 2026, following the acquisition of xAI, it is no longer just a space company.

What Musk wants to convey is a longer chain: rockets reduce the cost of reaching orbit, Starlink establishes global connectivity, Starship delivers heavier payloads to orbit, AI business generates computing demand, and data centers are eventually placed in space.

The story is grandiose. But Musk has packaged all businesses together for investors, not just the already operational Starlink and the proven Falcon 9, but also the non-commercialized Starship, the economically unproven orbital data center, and the still money-burning yet somewhat stranded AI business.

Therefore, analysts and different markets have a significant difference in their estimates of SpaceX's revenue and fair valuation.

The most conservative estimate comes from Morningstar, with a fair value estimate of around $780 billion, which is less than half of the IPO target. Morningstar does not deny SpaceX's technological capabilities, believing the company has a "narrow moat." SpaceX alone accounted for more than half of last year's global rocket launches. However, Morningstar feels highly uncertain about the feasibility, timetable, and financial results of orbital computing and the AI business.

NYU finance professor Aswath Damodaran's model ranges from $1.22 trillion to $1.29 trillion, recognizing the engineering advantages but stating that the upside potential above $1.75 trillion has diminished. Long-term holder Scottish Mortgage's anchor point is at $1.25 trillion and does not directly align with the IPO target price.

On the other hand, underwriters are pushing the price up. Goldman Sachs predicts that SpaceX's AI division will contribute annual revenue of $322 billion by 2030, with the company's overall revenue exceeding $470 billion. Morgan Stanley goes even further, forecasting revenue to reach $34 trillion by 2040, with adjusted EBITDA surpassing $27 trillion.

And the most aggressive pricing comes from the crypto space. Binance's SPCXUSDT perpetual contract launched in May reflects an expected valuation range between $1.75 trillion and $2 trillion. On Polymarket, over 70% of bets anticipate the final IPO valuation surpassing $2 trillion. As the listing approaches, Binance has adjusted the estimated number of SpaceX shares corresponding to the SPCXUSDT contract from 11.87 billion to 13.08 billion, translating to a valuation exceeding $2 trillion at the current price.

Currently, the next Starship test flight is scheduled for June. If it can enter commercial operation stably, frequently, and cost-effectively, Musk may once again successfully craft a perfect narrative. However, if there are failures during the roadshow or if the progress is below expectations, many long-term narratives will be affected, potentially shaking the market value and stock price.

Is the Unlocking Happening Too Quickly

On the topic of unlocking, this is also a point of contention for investors regarding the SpaceX IPO.

Normally, new stocks have a 180-day lock-up period during which insiders cannot sell, aiming to allow the market enough time to establish a true price.

SpaceX nominally also has 180 days, but what many people don't know is that it follows a staggered early unlocking structure, breaking down these 180 days into several segments.

The first unlocking date comes after the Q2 earnings report, where eligible insiders can sell 20% of their shares, roughly between mid-July and September.

In other words, just over a month after going public, the first batch of unlocked shares may appear. Other insiders can start selling as early as the second trading day after the first quarterly earnings report, most likely in August.

There are further arrangements: if the stock price is more than 30% above the offering price for 5 out of 10 consecutive trading days before the first earnings report, up to an additional 10% can be unlocked early. In addition to releases spread across five timeframes at 70, 90, 105, 120, and 135 days after the IPO, up to an additional 28% can be released after the Q3 earnings report, with full unlocking by day 180 (mid-December).

While Musk himself has pledged not to sell within 366 days, all other early employees, venture capitalists, and the banking syndicate eager to exit can start leaving after the first earnings report.

For those who just bought in at $135, the first wave of selling pressure they may face could come sooner than expected.

Index Funds Rush to Amend Rules for SpaceX

The first three points can be seen as issues and controversies specific to SpaceX, but this one may be a problem with the entire market mechanism.

Nasdaq changed its rules for this listing. Normally, new companies have to wait about a year before qualifying for entry into major indices to ensure that the market completes true price discovery first.

Nasdaq's "fast-track inclusion" mechanism has compressed the window for SpaceX's entry into the Nasdaq-100 to 15 trading days, with FTSE Russell even shorter at just 5 trading days. MSCI also confirmed a fast track for large IPOs. The S&P 500 is one of the few that has not followed suit because it still requires companies to have sustained profitability, a criterion which SpaceX does not currently meet, thus temporarily excluding it.

Another issue lies in the free float. This time, SpaceX's new shares account for about 4.3% of the total shares outstanding, with over 95% held by Musk, early employees, and institutional investors, all of which are under lock-up and cannot be traded on the secondary market. In comparison, Microsoft has a free float ratio of 99.97%, NVIDIA 95.8%, and Amazon 90.5%.

Nasdaq also allows stocks with a low free float to have their weight calculated based on up to three times the actual free float. This means taking a tightly held real free float in the billions and slapping on a fictional weight in the tens of billions, then forcing a large amount of price-indifferent passive money to buy in according to the rules.

Some estimates suggest that passive money could consume approximately 30% of the free float within the first 15 trading days post-listing, with the total amount of funds tracking the Nasdaq-100 around $1.4 trillion. What's even more painful is that since no constituents are removed to make room, every Nasdaq-100 fund has to proportionally sell all its other holdings to buy this new stock. This means, for one stock, a forced liquidation of all other stocks.

'The Big Short' Michael Burry echoed criticism of this rule, with Wall Street veterans directly calling it 'outrageous' index manipulation. A Wall Street Journal columnist described Nasdaq's rapid inclusion rule as 'arbitrary, unfair, and potentially dangerous,' while a Financial Times journalist referred to it as the 'largest game of pass the parcel in history.'

In general, the core of market criticism is that low-fee index funds were originally meant to be a tool for ordinary people to access the market at extremely low costs. Now, due to rule rewrites, they could become channels for early capital exit and risk transfer. Pouring retirement account money, as per the rules, indiscriminately into a new stock with a market-to-sales ratio of 94x is the antithesis of what index investing was supposed to solve initially.

The bigger the tree, the more wind it catches, and naturally, the more controversy it attracts. SpaceX's IPO is the grandest of this era and also the most controversial.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia