TL;DR

· Alphabet is planning to conduct approximately $800 billion equity financing, with the subsequent size increased to $847.5 billion, putting the funding pressure for AI development in the spotlight.

· The market's concern is not about the direction of AI going astray, but rather how much money needs to be initially spent on data centers, chips, power, and network infrastructure, and how long it will take to see a return on investment.

· Related stocks: GOOGL, NVDA, AVGO, AMD, MU, DLR, EQIX, as well as assets related to power and data centers.

For the past few years, the most fundamental question in AI transactions has been quite simple: Will AI change the world? As long as the answer leans towards "yes," the market is willing to give higher valuations to chipmakers, cloud providers, software companies, and model firms.

Recently, the market narrative has started to shift. There have been pullbacks in some semiconductor and high-valuation AI software stocks, and market participants are beginning to reallocate their preference towards areas with clearer orders and more stable cash flows. Meanwhile, Alphabet announced a large-scale equity financing and raised its 2026 capital expenditure guidance in the previous Q1 earnings report.

These two events cannot be simply attributed to a "drop caused by financing." A more accurate context is that the market is repricing AI from a software-like growth story to a round of heavy asset infrastructure cycle.

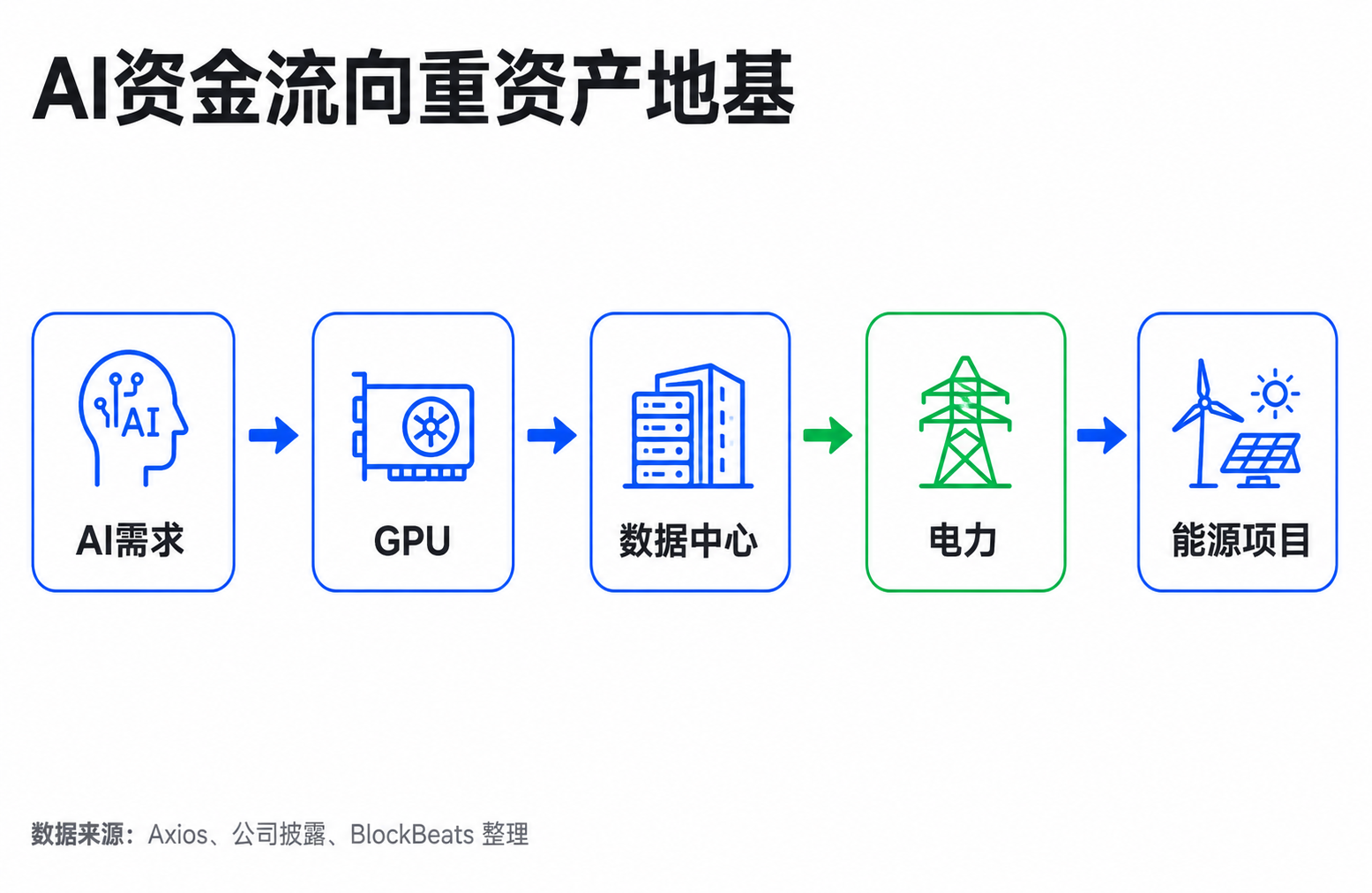

The key term here is capital expenditure. AI is not a business that can expand with just a few lines of code; it requires chips, data centers, networks, power, and land. The larger the capital expenditure, the more investors will ask three questions: where does the money come from, how expensive is the money, and how long until there is a return.

Alphabet's Financing Forces the Market to Recalculate Capital

Alphabet's financing itself is not a crisis signal, but it serves as a strong reminder: AI development is already a giant capital project.

According to SEC filings and reports from Reuters and Investing, in June 2026, Alphabet announced that it is planning to conduct approximately $800 billion equity financing, with the subsequent size increased to $847.5 billion. The funding purposes include AI infrastructure and computing power expansion needs, but not all funds are directly allocated to AI capital expenditures. SEC documents show that out of the $400 billion ATM program, approximately $300 billion is expected to be used for administrative arrangements related to employee equity award tax obligations.

This distinction is very important. Representing the full $847.5 billion as "AI Investment Fund" would exaggerate the direct scope, but it would still change investors' perception. Even cash cows like Alphabet need to expand financing in the public markets. Naturally, the market will question: If even it needs to enhance financial flexibility, who will provide the money for OpenAI, Anthropic, xAI, data center REIT, and power companies in the future?

Capital expenditures and operating expenses are also not the same. Spending money on hiring employees and marketing is considered operating expenses, while buying servers, building data centers, and pulling power is categorized as capital expenditures. The latter is more like building a factory, with significant upfront cash flow pressure that will gradually be reflected on the balance sheet through depreciation, but the market will immediately assess the payback period.

In Alphabet's Q1 2026 earnings call, the company raised its full-year capital expenditure guidance from $175 billion to $185 billion to $180 billion to $190 billion. The reasons cited by the company include investments related to the Intersect acquisition and the demand for AI compute. The company emphatically stressed maintaining a healthy balance sheet and financial flexibility, with management not framing financing as a survival pressure.

Investors are doing the math. As the capital expenditure guidance continues to increase, the denominator in valuation models also changes: depreciation increases, free cash flow is under pressure, financing costs, and potential equity dilution come into the calculation. AI transactions are entering the next stage, with the previous stage rewarding imagination and the latter stage rewarding capital efficiency.

AI Money Isn't Just Burning on Big Factory Accounts

The capital demand for AI infrastructure does not only rest on the shoulders of tech giants like Alphabet, Microsoft, Amazon, and Meta. What truly concerns the market is that multiple entities may be competing for the same pool of capital.

The first category is cutting-edge model companies. Companies like OpenAI, Anthropic, and xAI are experiencing rapid revenue growth, but training and inferring models require continuous purchases of computing power, leading to substantial cash burn. Unlike mature cloud providers with advertising, cloud, and software cash flows as foundations, they rely more on external financing, strategic investments, and may also depend on IPOs or the debt market in the future.

The second category is data center companies. AI doesn't need ordinary office servers but high-density, high-energy-consuming data centers. Data center REITs raise capital to build facilities and then lease the computing infrastructure to cloud providers or AI companies. Assets like Digital Realty and Equinix benefit from demand expansion, but the expansion itself also requires ongoing financing.

The third category is Electricity and Utilities. One of the biggest bottlenecks for AI data centers is not the chips, but the electricity. Large data centers will put pressure on the power grid, substations, transmission lines, and long-term power purchase agreements. The money burned by AI companies will not stop at the GPU; it will flow through the industry chain to land, data centers, cooling, the power grid, and energy projects.

According to Axios on June 10, Alphabet, Amazon, Meta, Microsoft, and Oracle have already raised $255.34 billion through equity and debt financing by 2026 and have stated that the AI data center spending of these five companies will reach approximately $750 billion within the year. This number cannot be taken as definitive causal proof, but it gives the market a sense of scale: AI's capital needs are transitioning from a problem of individual companies to a financing cycle that the entire financial market needs to absorb.

In the past, the market often viewed AI as a software revolution: low marginal costs, rapid growth, high profit margins. Now, advanced AI resembles more of an infrastructure revolution like railways, electricity, and communication fiber optics: early-stage concentrated construction is needed, requiring massive investment. It may eventually create value, but in the middle, it will face tests of financing capacity, capital costs, and capacity utilization.

Valuation Logic Shifts to Payback Speed

When a market reassessment occurs, the first thing that prices usually reflect is not that the fundamentals have deteriorated, but that investors are starting to ask a different set of questions.

In the past, the questions were: Whose AI narrative is the strongest? Whose revenue is growing the fastest? Who is closest to the next-generation platform entry? Now, the questions have changed to: Who can turn invested capital into cash flow? Whose orders are firm enough? Who can access low-cost financing? Who will be diluted or see profits dragged down in a high capital expenditure cycle?

This explains the recent differentiation in the AI sector. High valuation AI software companies and those with a heavy focus on long-term stories are more likely to come under pressure because their valuation depends on future growth. Once the market adjusts the cost of capital upwards, the value discounted from future cash flows will decrease. Some semiconductor companies may also be affected because investors will be concerned about whether orders can continue to grow at a faster-than-expected pace.

However, this does not mean that all AI assets are being abandoned. Hardware, storage, network equipment, data centers, and power assets with clearer orders may actually receive relative support in the reassessment. The reason is straightforward: when the market begins to focus on the construction cycle, those selling shovels will still have demand; but investors will more critically ask, whose orders are truly visible, and who is just relying on a narrative to boost valuation.

This is also where Alphabet's management differs from cautious investors. The management emphasizes that AI investment is a strategic necessity, and the financing is to maintain the initiative in long-term competition. Cautious investors are concerned that the pace of AI monetization may lag behind capital expenditures, especially when multiple tech giants and AI companies are simultaneously expanding financing, causing the capital market to demand higher returns, thus depressing valuations.

Both sides can coexist. AI can be a long-term correct infrastructure investment, but it can also temporarily depress free cash flow and valuation multiples. For investors, being "bullish on AI" and "bearish on some AI valuations" are not contradictory.

Next Step: Focus on Capital Expenditure and Revenue Realization

It is premature to attribute the recent pullback purely to AI financing pressures or to declare that AI is facing a liquidity crisis. Macro interest rates, profit-taking, cooling of crowded trades, and labor market disruptions could all be reasons for sector fluctuations. Financing news is more like being incorporated into the market's explanatory framework rather than being a standalone price driver.

However, this explanatory framework itself is worth noting. Once the market begins to price AI based on "capital expenditure, financing costs, payback period," the rankings of many assets will change.

For cash-cow companies like Alphabet, the issue is not whether they can raise money but whether AI investment will continue to squeeze free cash flow and whether the additional investment can translate into cloud revenue, advertising efficiency, subscription revenue, or enterprise service revenue. As long as revenue growth can cover depreciation and financing costs, the market can accept higher capital expenditures; if capital expenditures continue to rise while returns are slow to materialize, valuation pressure will become more apparent.

For pure AI companies, the issue is more direct: whether high revenue growth can keep up with computing power consumption. If companies like OpenAI, Anthropic, and xAI can demonstrate that enterprise customers are willing to continue paying and that unit economics are improving, external capital will still flow in; if revenue growth is mainly eaten up by higher training and inference costs, the next round of financing or IPO pricing will be more demanding.

For data center and power assets, the market will look at long-term contracts, utilization rates, financing structures, and power constraints. The more real the AI demand, the more important these "groundwork" assets become; but if financing costs rise, or if data center construction outpaces actual demand, they will shift from beneficiaries to recipients of heavy asset pressure.

The most important validation point going forward is not a single day's semiconductor index movement but whether the next round of earnings reports will continue to raise capital expenditure guidance, whether AI revenue can be realized more quickly, and whether the public market can still smoothly absorb large-scale equity and debt issuances. As long as these variables remain positive, AI trading will not end; however, the market's valuation language for AI has now moved beyond the stage of just looking at the imagination space.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia