Editor's Note: Against the backdrop of a Super IPO, an AI narrative, and the repricing of risk assets, the market's discussion of SpaceX's listing is shifting from "how much is this company really worth" to "how will it trade once it goes public." However, as SpaceX becomes one of the most-watched tech assets, a more critical question begins to emerge: on the first day of trading with no historical price, no mature option structure, and no clear chip distribution, should investors understand it through a valuation framework or through market microstructure?

This article is translated from The Flow Horse's video content on SpaceX IPO's first-day trading strategy, focusing not on SpaceX's long-term fundamentals, but on dissecting the liquidity flow, float, index inclusion, and unlock pace it may face in its early days as a listed company. The video creator is a market trader who has long focused on IPOs and order flow trading, with a perspective closer to the order book and trade execution rather than traditional company valuation analysis.

In this piece, the SpaceX IPO is dissected into a set of more fundamental structural issues: it is not a simple "to buy or not to buy" question, but a process in which traders, retail investors, passive funds, and internal shareholders reprice around limited liquidity at different time windows.

Firstly, retail investors are most likely to misjudge the first-day trading environment. In the past, when retail investors traded popular stocks, they usually relied on trendlines, support and resistance, highs and lows, and opening momentum. However, on the first day of the SpaceX IPO, there are no historical charts, no volume profiles, and no mature option structures. Before the first candle, the market does not have reusable price memory. What really determines the short-term direction now is the order book, volume, VWAP, opening range, and where real turnover occurs. This means that if retail investors chase the initial uptrend at the open or use technical analysis too early to find so-called trends, they are likely taking on the highest risk when the structure has not yet formed.

Secondly, past popular IPOs do not support the notion that there will inevitably be a one-way upswing in the early days of listing. Coinbase, Airbnb, and ARM have all had extremely high attention, but in the early days of their listings, they did not immediately show a stable trend; instead, they first experienced drastic two-way fluctuations. In the past, the market tended to interpret popular IPOs as the realization of emotional consensus; a more accurate understanding now is that they often first become places where short-term funds, profit-taking, and new buyers repeatedly turn over. This means that even with a strong narrative and brand recognition, SpaceX may not be suitable for trend followers in the first week. Those truly suitable for participating on the first day are often traders who can quickly read order flow, control positions, and accept two-way fluctuations.

Third, the key to the first day strategy is transitioning from "predicting direction" to "waiting for structure." In the past, many traders would preset their long or short views before the market opened, and then use the first price movement to validate their judgment. However, for low float IPOs like SpaceX, it is more important to let the market establish a structure first: to see if there is support around $135, if the 5-minute opening range is cleanly broken, if VWAP retest holds, and if there is continuous refreshing of hidden buy and sell strength in Level 2. The essence of trading now is not to rush to a conclusion before others, but to assess who takes the lead after the market forms the initial price coordinates. This means that the most crucial aspect is not entering the market first but avoiding being passively traded at the most chaotic, widest spread, and strongest emotional position.

Fourth, investors must understand that different stages are dominated by different types of capital. In the first 15 trading days, SpaceX resembles more of a short-term trading game led by low float, emotional capital, and order flow. Around the 15th trading day, the Nasdaq index includes anticipation of price-insensitive buying pressure for the second stage; post first earnings report, unlocking of supply tests market absorption; looking further ahead, unlocking by major shareholders at 70 days, 90 days, 120 days, 180 days, and one year will gradually provide more reliable long-term signals. In the past, IPOs were often judged based on their first-day performance; now, SpaceX is more like a series of continuous liquidity tests. This implies that long-term judgment should not be based on first-day emotions but on whether the price can stabilize after new supply enters the market.

Fifth, SpaceX trading may not necessarily be confined to SpaceX itself. Assets related to aerospace and the space economy, such as Rocket Lab and LUNR, may become shadow stocks expressing the same theme during the listing period. In the past, IPO trading usually revolved around the main asset; now, when the float of the main asset is too low, the volatility is too high, and the spread is too wide, related assets may actually provide a clearer trading structure. This means that market trading involves not only SpaceX's stock but also the industry narrative and liquidity spillover it activates.

If this article is condensed into one judgment, it would be: the SpaceX IPO first day belongs to traders, and long-term judgment should wait for supply testing. For traders, the first day may be the "Super Bowl" of order flow trading; for investors, the price movement on the first day should not be overinterpreted. In this sense, the core issue of the SpaceX IPO is no longer just whether to buy on the first day but whether participants can determine which game they are entering: looking at order flow on the first day and assessing long-term supply absorption capacity. Mixing these up is precisely why most retail investors are prone to losses.

Below is the video content (rearranged for better readability):

Why Most Retail Investors Might Lose Money in the SpaceX IPO

The riskiest aspect of the SpaceX IPO's first day is that many people will treat it like a regular hot stock to trade.

A regular stock has a historical price range, previous highs and lows, trading volume clusters, and plenty of market memory. Traders can reference past support and resistance levels, moving averages, options positioning, and cost basis. But the IPO's first day is a blank chart. Before the first candlestick appears, there is no real trading history in the market.

This means that drawing trendlines too early is meaningless, and chasing the initial rally right after the market opens can easily be pierced by a reversal. Especially in a low float environment, the price may spike due to brief buying pressure and then suddenly drop due to profit-taking or institutional selling. Retail investors who only focus on price gains and emotions can easily enter the market at the most chaotic moment.

The true trading logic of SpaceX's first day is the real-time formation of an auction mechanism, where both buyers and sellers seek a balance at different prices. What traders need to observe is: Who is willing to bid up to buy? Where are sellers constantly adding liquidity? At which price levels is there significant volume but the price cannot move? This order book information is more important than any pre-drawn technical analysis.

Trading Details: $750 Billion Financing, 3% Float, and High Retail Allocation

In this IPO, SpaceX plans to issue approximately 5.55 billion shares, raise about $750 billion, price each share at $135, and achieve a valuation of about $1.7 trillion. This scale alone is enough to make it a market-moving event.

But what truly determines the first-day volatility is not just the financing size but the float. Initially, only about 3% of SpaceX's shares will be freely tradable. This means that even moderate buying pressure could significantly impact the price. Retail FOMO, active fund accumulation, and small-scale institutional buying could all cause the price to temporarily deviate from the fundamentals.

Another special variable is the retail allocation. The retail allocation in this IPO could be around 30%, roughly 3 to 4 times that of a typical IPO. This will make post-listing trading more difficult to assess. On one hand, more retail investors holding chips early might reduce the FOMO of missing out on buying at the listing; on the other hand, these early chip holders may also take profits after listing, creating an initial supply.

Therefore, the core of the SpaceX IPO is not simply judging "oversubscription is a positive sign" but understanding the chip structure: an extremely low float can amplify both the upside and downside, while high retail allocation may make first-day buying and selling more aggressive simultaneously.

Day 15 of Trading: Inclusion in Nasdaq Index Could Alter Fundamentals

Another key milestone is the 15th trading day after the IPO. According to the schedule, SpaceX could be included in the Nasdaq 100 Index (NDX). While this arrangement is subject to final rules and actual results, the trading logic associated with it is crucial.

During the initial listing phase, price action is primarily driven by fast money, retail investors, active funds, and sentiment-driven funds. These funds are price-sensitive and tend to enter and exit quickly based on volatility. However, after inclusion in the index, another type of funds will enter the market: passive funds.

Passive funds are characterized by being price-insensitive (Price-insensitive Flow, meaning they must buy due to index rules or portfolio requirements, not because the price is cheap). Index funds, ETFs, and related tracking products need to allocate constituent stocks according to rules, and this type of buying is often more mechanical and can be front-run by the market.

Therefore, prior to the 15th trading day, active funds may try to front-run (buying before definitive buying pressure arrives). If SpaceX has already built upward momentum in the early days of trading, the mechanical buying pressure from index inclusion may further amplify the trend. However, if the trend has been weak in the first two weeks, this buying pressure may not be sufficient to single-handedly reverse the market direction.

This is also what sets SpaceX's IPO apart from a regular first-day trading: it is not a single-point event but a series of capital flow nodes.

The First Day Is About Order Flow Trading, Not Chart Trading

The most critical assessment on SpaceX's debut day is: do not treat it as chart trading.

Ordinary traders are used to asking: where is the support? Where is the resistance? Where is the previous high? Where are the high-volume nodes? What are the key pain points for options? However, most of these questions do not have answers on IPO day. Without a historical price chart, there is no reliable technical structure; without a mature options market, there are no open interest contracts to refer to either.

The real questions on the first day are: where do buyers and sellers find agreement? Where is there significant turnover? Is there buying interest below the offer price after a price drop? Are sellers continuously supplying during price spikes? These are the core of order flow trading.

The first critical price levels must be determined by the market on the same day. The first one is $135, the IPO set price. Traders need to observe the price's performance relative to $135: can it quickly recover after falling below? Can it sustain above once breached? If there is buying interest every time the price drops below $135, it indicates this level might become an early cost anchor; if selling occurs every time it goes above $135, it suggests stronger supply overhead.

Next is VWAP (Volume-Weighted Average Price, representing the average transaction cost in the market for the day). During the first hour after listing, whether the price is above or below VWAP, and whether there is support upon retracing to VWAP, will directly reflect which side, buyers or sellers, is in control.

Lastly, we have the first-day high and low points. After the closing bell, the first day's high and low prices will become the most important reference for the following days. For a new stock without a price history chart, the price range on the first day forms the market's initial coordinate system.

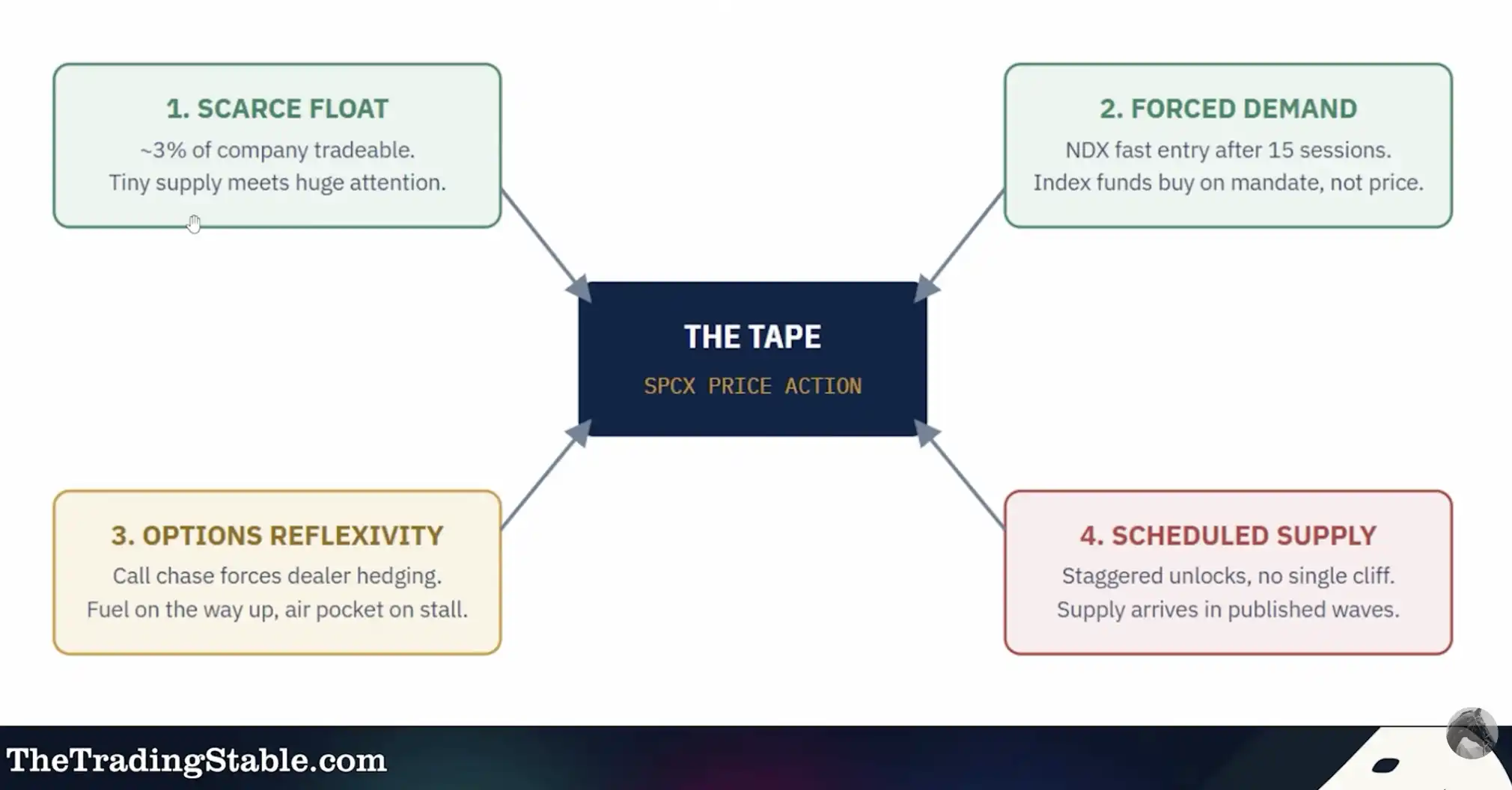

Four Types of Fund Flows Driving Price

The price fluctuations of a SpaceX IPO early on can be divided into four categories of fund flows.

The first type is scarcity-driven buying pressure from a very low float. A 3% float means there are very few tradable chips in the market, so a slight demand concentration can quickly drive the stock price up. This is also why blindly shorting on the first day is very risky. Low float stocks may not always continue to rise, but they are most likely to "squeeze" shorts in a short period of time.

The second type is passive buying pressure brought by inclusion in the Nasdaq index. If it is included in the NDX on the 15th trading day, index funds and related products need to buy according to the rules. This type of fund does not place orders based on valuation but based on index weight. For long positions, this is an ideal mechanical demand; for day traders, it is a time window that can be traded in advance.

The third type is Options Reflexivity, where the options market affects stock prices in return. Once options are listed, retail investors buying a large amount of call options may force market makers to buy the stock to hedge, thus forming a Gamma squeeze (options buying pressure drives market makers to buy the stock to hedge, further amplifying the uptrend). However, this mechanism usually does not appear immediately on the first day of listing and may not mature in the first week.

The fourth type is share unlocks (Unlocks, i.e., gradually entering restricted shares into the market). This will bring additional supply and is a risk point that all long-term investors must pay attention to. What makes SpaceX special is that it may not simply wait for a one-time unlock after 180 days, but may release chips in stages.

Unlock Schedule: Not a One-Time 180-Day Cliff

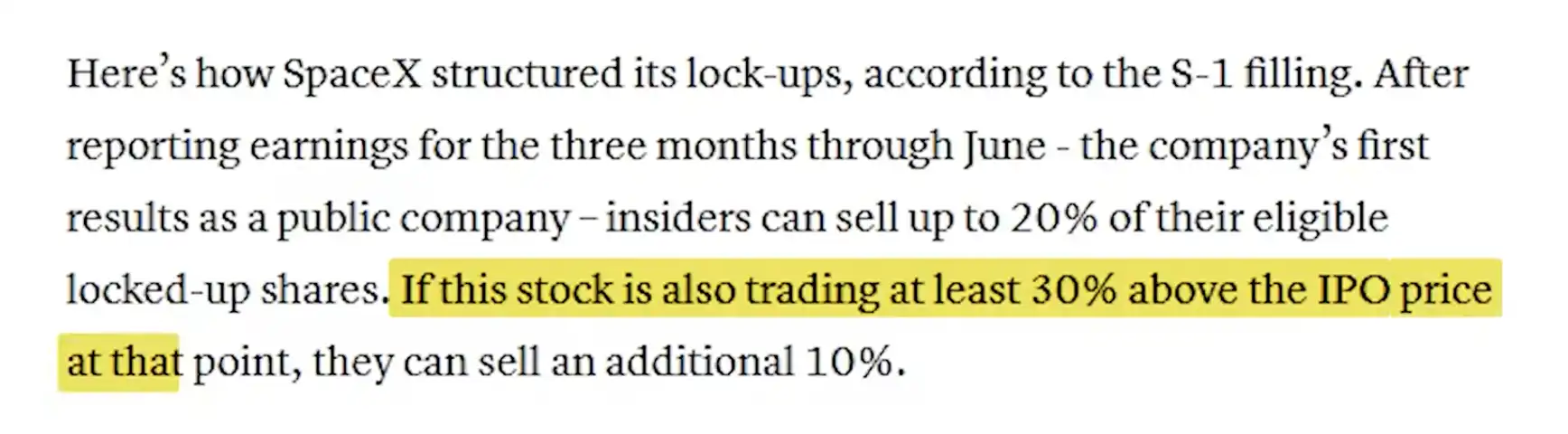

A common risk point in traditional IPOs is that after the 180-day lock-up period ends, early investors and employee shares are unlocked in concentration, causing a sudden surge in market supply. However, the unlock structure of SpaceX described in the video is more complex: it may not be a one-time cliff, but a set of staged liquidity events.

Firstly, after the first earnings report, up to 20% of eligible shares may unlock. This means that the earnings report is not only a performance event but also a supply event. If the stock price was driven up by sentiment before the earnings report, additional supply after the report may dampen momentum.

Secondly, the unlock may also be tied to price performance. If the stock price stays above $135 for more than 30% of the 10 trading days before the earnings report, an additional 10% unlock may occur. Such arrangements allow the price rally itself to trigger more supply, creating a dynamic equilibrium: the sharper the rise, the more shares available for sale afterwards.

Subsequent unlocks are equally important. The video mentioned that approximately 7% of shares may unlock around the 70th, 90th, and 120th days, with a complete unlock after 180 days. Regarding employee shares, about 5% of employee holdings may be sold immediately after the first earnings report, without additional performance or price conditions. Musk and the largest shareholders may need to wait for over a year, around 366 days.

These dates are especially important for long-term investors. Determining whether SpaceX is truly forming a bottom cannot be solely based on the stock's debut performance but on whether buying interest can absorb each new round of supply entering the market.

Lessons from Past IPOs: Coinbase, Airbnb, ARM Did Not See a One-Way Trend at the Beginning

A hot IPO often creates a misconception: since there is high market attention, the stock should only rise after going public. However, early trading of Coinbase, Airbnb, and ARM shows that hype does not equate to a one-way trend.

The video mentioned that these hot IPOs experienced significant volatility in the early days of trading. Coinbase's early volatility reached about 119 points, Airbnb around 53 points, ARM around 22 points. The key point is not the specific numbers but what they indicate: in the first few days or weeks of a hot IPO, there is often intense two-way trading instead of a stable trend.

This environment is more suitable for day traders, scalpers (traders who profit from frequent small price fluctuations through quick in-and-out trades), and flow traders, rather than ordinary trend followers. Trend traders need structure, which is often lacking in the early stages of an IPO.

SpaceX might be even more extreme. It has already been heavily oversubscribed and may allow more retail investors to get an early allocation. This means that after the opening, there are both chasing momentum funds and profit-taking funds; there are people looking to buy on the 15th day for expected index inclusion and others believing that the hype itself is a selling opportunity. Both long and short positions are crowded simultaneously, leading not to a clean trend but to high turnover, high volatility, and high noise.

Day One Trading Strategy: Wait for Market Structure Before Taking Action

SpaceX's first-day trading rule is not to chase the opening bell.

The opening moment is usually when the noise is highest, the spread is widest, and emotions are most extreme. Especially in a low float environment, the initial surge may just be a short squeeze, and the first drop may be due to insufficient liquidity. The real tradable structure needs to wait for the market to form.

The first key level to watch is $135. If the price breaks below $135 but quickly recovers and reclaims the opening range and VWAP, it indicates genuine buying interest below. Conversely, if the price repeatedly tries to move above $135 but gets sold off, it suggests that sellers might be in control.

The second key level is the 5-minute Opening Range. Filtering out noise with the 5-minute or 30-minute opening range can help avoid premature stop-outs. A breakout after a narrow opening range is more meaningful because many intraday positions are concentrated within a limited price band. Once the price exits this range, stop-losses and chasing orders are more likely to be triggered.

The third key level is the VWAP. If, after one hour of trading, the price is operating above the VWAP and quickly attracts buying interest on pullbacks to the VWAP, it may signal a bullish advantage. If the price remains under pressure below the VWAP for an extended period, showing weak rebounds, it indicates that the day's average trading cost is turning into resistance.

The fourth key level is the "Ghost Level," which represents hidden buy or sell orders continuously absorbing transactions at a specific price level. If a price level appears to have limited visible orders but is seeing sustained high volume, yet the price cannot break through, it suggests hidden sellers are consistently filling orders. Conversely, if a price level is seeing continuous volume but the price refuses to drop, it may indicate hidden buyers are accumulating.

These temporary price levels may not necessarily be significant for the following months, but they are crucial on the first day. This is because, in the absence of historical charts, they are the initial milestones created by the market.

Position Sizing and Risk Management: Don't Trade Low Float IPOs Like Blue Chips

While SpaceX may be a large company, its early trading characteristics may not resemble those of large-cap blue-chip stocks.

If the float is only 3%, the order book may be thin, the spread may be wide, and the price may experience rapid fluctuations due to consecutive sweeps. Additionally, if the options market is not yet mature, traders lack hedging tools, and having a large position can easily amplify losses due to slippage and trading halts.

Therefore, you cannot trade SpaceX using the position sizing strategy for mature large-cap stocks like Apple, Microsoft, or NVIDIA. Beginners who simply want to learn order flow should start with a very small position, or even just observe without trading. For most people, missing the opportunity on the first day is not the most serious issue; being driven by FOMO to enter a heavy position at the most chaotic point is the greatest risk.

Day traders must accept one reality: on the first day, the most important thing is not to capture every price swing, but to avoid being "washed out" by the market in an unstructured position. Long-term investors should pay more attention to subsequent supply nodes rather than rushing to prove themselves right about SpaceX on the first day of trading.

Four Key Things to Understand

First, the first 15 trading days are likely primarily driven by emotion. With an extremely low float, immense attention, and a lack of technical levels, the price will mainly rely on order flow and short-term fund inflows.

Second, the 15th trading day may be a node for a change in fund nature. If SpaceX is included in the Nasdaq 100, price-insensitive mechanical buying may enter the market, and active funds may also trade this expectation early.

Third, the first earnings report is not just an earnings event but also a supply pressure point. Some shares may start unlocking post-earnings, and the market needs to prove it can absorb the additional supply.

Fourth, unlocking is not a one-time event but a liquidity stress test spanning the next year. Share unlocks by major stakeholders at 70 days, 90 days, 120 days, 180 days, and even one year later will retest the true buying foundation for SpaceX.

SpaceX Shadow Stocks to Watch

During SpaceX's listing, proxy assets in related industries (Proxy, i.e., substitutes used to express similar themes or risk exposure when direct trading of the core asset is not possible) are also worth watching.

Stocks related to aerospace, defense, rocket launches, satellites, and the space economy may receive overflow funding due to SpaceX's market hype. Examples mentioned in the video include Rocket Lab (RKLB) and LUNR among other space-related assets.

The opportunity with these shadow stocks lies not in a guaranteed benefit but in their potential to serve as an alternative path for funds to express the SpaceX theme. Especially when SpaceX itself has wide spreads, high volatility, and low float, some related assets with better liquidity may actually provide a clearer trading structure.

However, the proxy transaction must be based on on-chain validation. If the underlying asset only experiences a temporary price increase without trading volume, sustainability, or relative strength, the SpaceX logic cannot be forcibly applied.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia