On April 21st, both Polymarket and Kalshi announced their foray into perpetual contracts on the same day. This synchrony is unlikely to be a coincidence.

The two platforms belong to different capital systems and user bases, with Polymarket backed by Peter Thiel and Silicon Valley venture capital, while Kalshi recently completed a new funding round in March with a valuation of $22 billion. Their usual relationship can hardly be described as harmonious. However, when faced with the same external threat, they almost simultaneously took the same defensive action.

Polymarket's product was launched on the day of the announcement, initially supporting BTC, NVDA, and gold, with a maximum leverage of 10x. Kalshi is set to go live on April 27th under the brand name "Timeless," leveraging its CFTC DCM license and the margin trading approval obtained in March. Both are playing the same card: licensed compliance + a native user base in prediction markets.

Vertical Competition

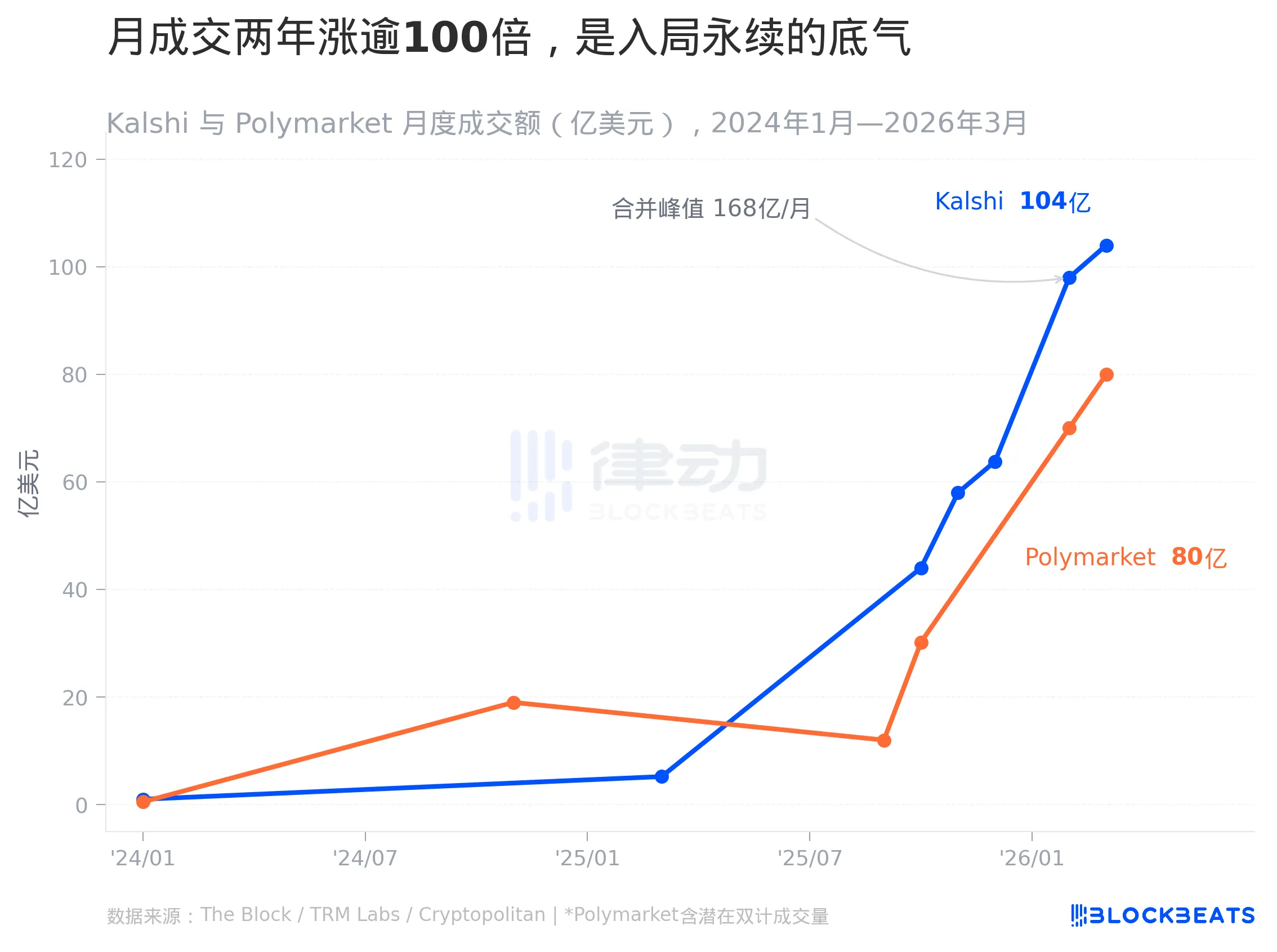

From early 2024 to March 2026, the monthly trading volume growth curves of Kalshi and Polymarket were almost vertical.

In January 2024, Kalshi's monthly trading volume was about $100 million. By March 2025, this number had risen to $5.21 billion. In October 2025, $44 billion. In March 2026, over $104 billion. In a little over two years, it increased by over 100 times.

Polymarket's pace was different but equally intense. During the November 2024 U.S. election, the monthly trading volume surged to about $19 billion, dipped after the election, but the platform then found sustained momentum. In February 2026, Polymarket's monthly trading volume reached $70 billion (according to The Block), around $80 billion in March. It is worth noting that Paradigm highlighted the issue of Polymarket's trading volume being double-counted in a report in December 2025, so the above figures need to retain the corresponding uncertainty.

The peak of the two platforms' combined monthly trading volume occurred in February 2026, totaling around $168 billion.

This set of data gave Polymarket and Kalshi the confidence to enter the perpetual contract market. Users demand such financial instruments, and the platforms have the ability to maintain liquidity and user stickiness. This is a starting point that any platform entering the perpetual contract market will find it difficult to replicate.

The issue is that the time window is narrowing. The perpetual contract products of the two platforms have some interesting differences in key dimensions.

Polymarket is taking the native crypto route. With 10x leverage, the initial batch supports BTC, NVDA, and gold, with direct competition targeting Coinbase and Hyperliquid. From a user perspective, Polymarket's core users are native crypto users, familiar with perpetual contracts and with low migration costs.

Kalshi is playing a more compliant channel. It has already integrated with Robinhood, whose user base consists of U.S. retail investors accustomed to traditional financial products, rather than crypto users operating on-chain daily. Kalshi is valued at $22 billion, higher than Polymarket's $9 billion. Behind the higher valuation is greater market expectations, requiring access to a market larger than the current prediction market.

Both platforms hold the CFTC's DCM (Designated Contract Market) license, a key qualification for legally offering leveraged derivatives in the U.S. Compared to offshore exchanges, this license is a core barrier for them to target U.S. users. In March of this year, Kalshi also obtained a margin trading permit, further enhancing regulatory compliance.

Is Hyperliquid the Real Competitor?

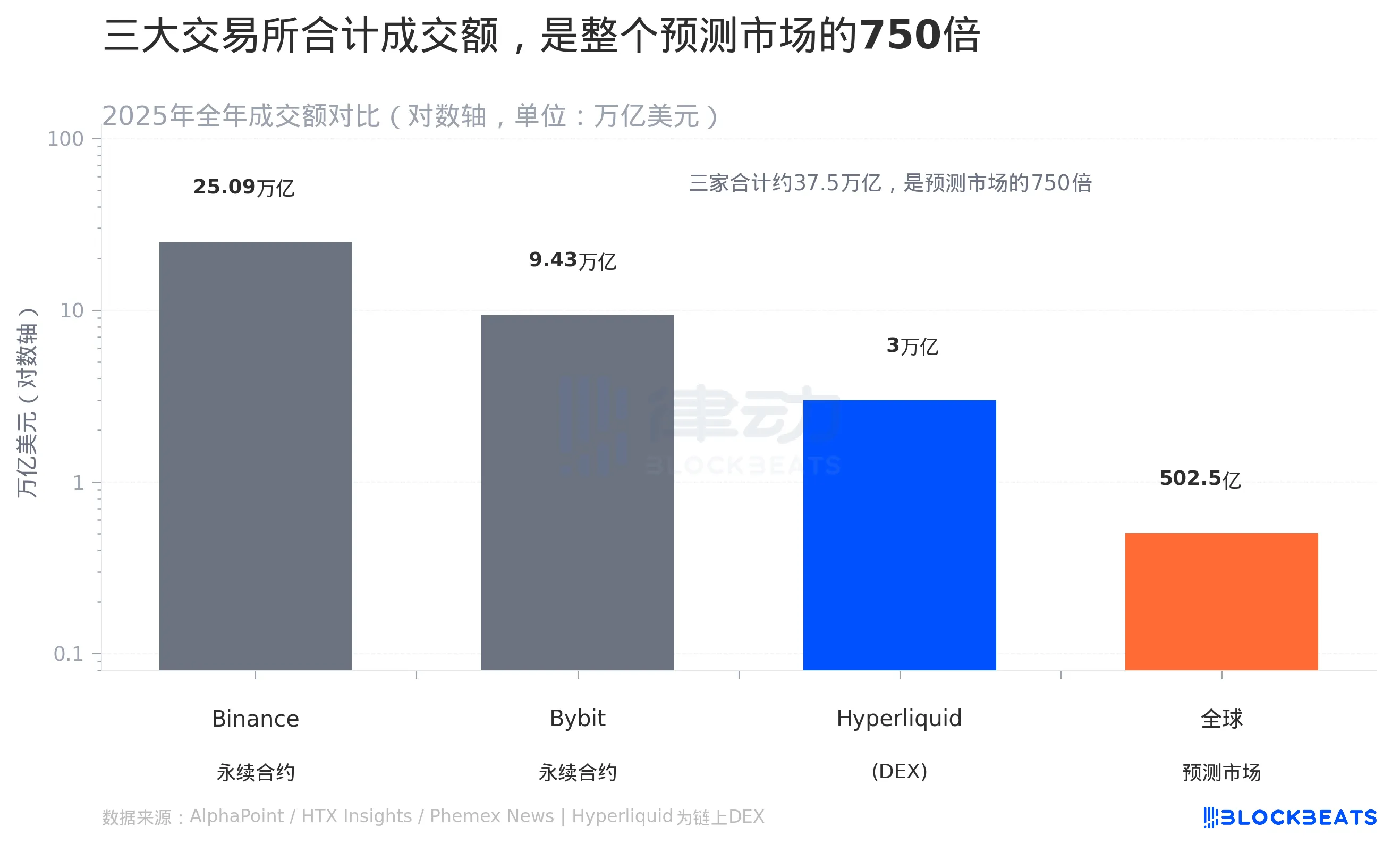

For the entire year 2025, the global prediction market's total trading volume is approximately $50.25 billion. While this number may seem significant, within the perpetual contract market, it is merely background noise. Binance's annual perpetual contract trading volume is $25.09 trillion, Bybit's is $9.43 trillion, and even the on-chain DEX Hyperliquid is projected to reach $30 trillion in 2025. The combined total of these three is around $37.5 trillion, which is 750 times the entire prediction market.

It's not that the prediction market is bad, it's that the two markets are currently not even in the same league. The market Polymarket and Kalshi aim to enter is three orders of magnitude larger than their current core businesses.

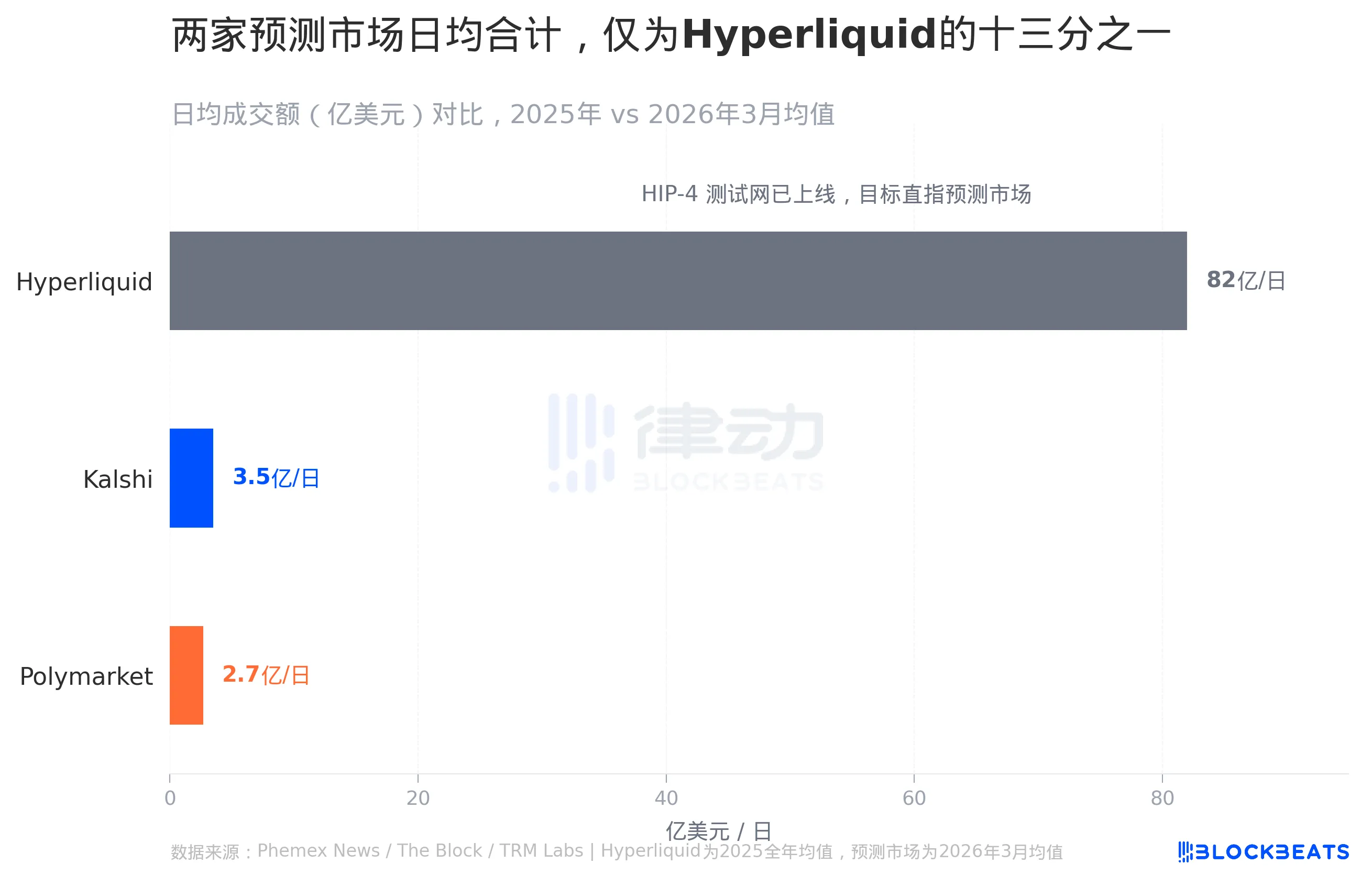

One detail to highlight this issue is that Hyperliquid's average daily trading volume is approximately $8.2 billion, equivalent to 80% of Kalshi's entire prediction market trading volume for the month of March 2026. In other words, Hyperliquid's daily volume almost matches Kalshi's monthly prediction market volume.

They are well aware of this scale difference. They chose to enter the perpetual contract not because they were confident in taking on Binance head-on, but because something else was happening.

By 2025, Hyperliquid had become the largest on-chain perpetual contract DEX with a trading volume of $30 trillion, holding about 38% market share in the decentralized derivatives field, surpassing 70% at one point earlier in the year. This achievement has already put pressure on centralized exchanges. However, what is making the prediction market nervous is another thing that Hyperliquid is doing.

HIP-4, a protocol proposal by Hyperliquid, aims to allow anyone to issue perpetual contracts on Hyperliquid, including contracts based on prediction market events such as election results, match scores, and macroeconomic data. This directly targets the core user demand of Kalshi and Polymarket.

In terms of numbers, the difference between the two sides is obvious. Hyperliquid's daily trading volume is around $8.2 billion, while Kalshi's daily prediction market trading volume is about $350 million, and Polymarket's is about $270 million. Hyperliquid's volume is roughly 13 times that of both combined.

However, trading volume is not the only dimension. Hyperliquid's users are crypto-native on-chain traders, with much less interest in prediction market events (elections, macros) compared to Kalshi's policy enthusiasts or Polymarket's gamers. Whether Hyperliquid can bootstrap liquidity on HIP-4 remains to be seen.

The current situation is that Hyperliquid wants to move towards the prediction market side, while Kalshi and Polymarket want to move towards the perpetual contract side. Both have put up a signboard at the other's doorstep.

Whoever deepens liquidity first will have the upper hand. But one thing is certain, before the official launch of Hyperliquid's HIP-4, Kalshi and Polymarket choosing to take this step on the same day is not just a product launch but more of a strategic move. The combined monthly trading volume of the two platforms has already exceeded $18 billion, holding the only compliant leverage derivatives license in the U.S., targeting U.S. retail users beyond the crypto-native community. These are conditions that Hyperliquid currently does not possess.

On the same day, two prediction markets launched perpetual futures contracts, bringing together prediction market products and cryptocurrency derivative products for the first time. What brought about this milestone was a looming threat that has not yet fully materialized.