TL;DR

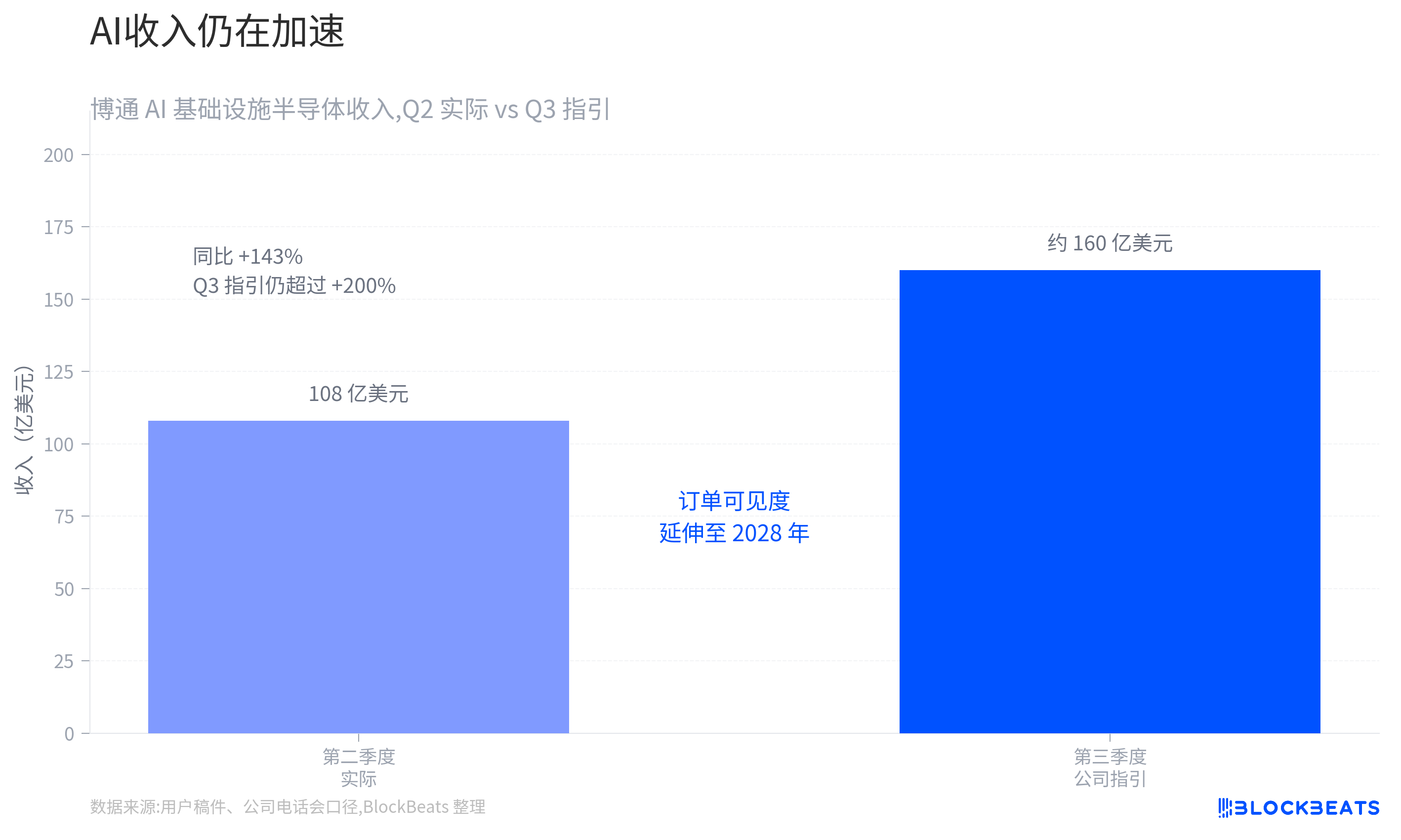

On June 5, Broadcom announced its second-quarter earnings. Looking at the numbers alone, this was almost a flawless report card. In the second quarter, Broadcom's semiconductor revenue related to AI infrastructure reached $10.8 billion, a 143% year-on-year increase. The company expects the related revenue in the third quarter to further increase to around $16 billion, with the year-on-year growth rate still exceeding 200%.

The order side is equally strong. CEO Hock Tan stated on the conference call that customer demand still exceeds the company's supply capabilities, with order visibility extending to 2028. In other words, at least from the data Broadcom holds, the construction of large-scale AI clusters has not slowed down but is still moving forward.

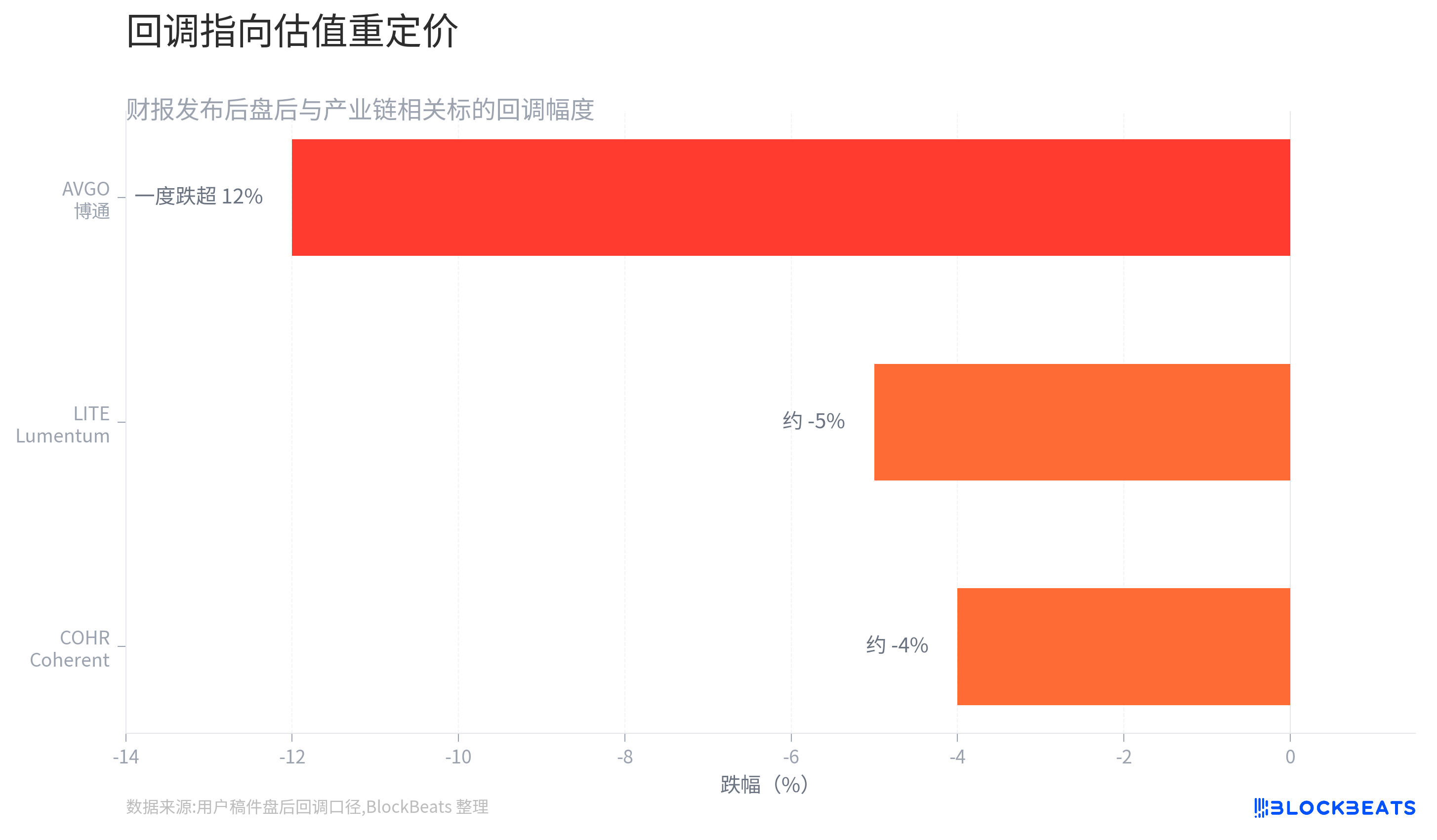

According to the market logic of the past two years, this should have been a report substantial enough to drive the stock price higher. However, the market's response was quite the opposite, with Broadcom's stock plunging by over 12% after the earnings release.

Meanwhile, optical interconnect leaders Lumentum and Coherent plunged simultaneously, and the high-bandwidth memory (HBM) and enterprise storage sectors also experienced a correlated pullback.

On one side, there is record demand and orders, while on the other side, there is a double-digit decline.

This may be the most noteworthy signal in the current AI trading environment.

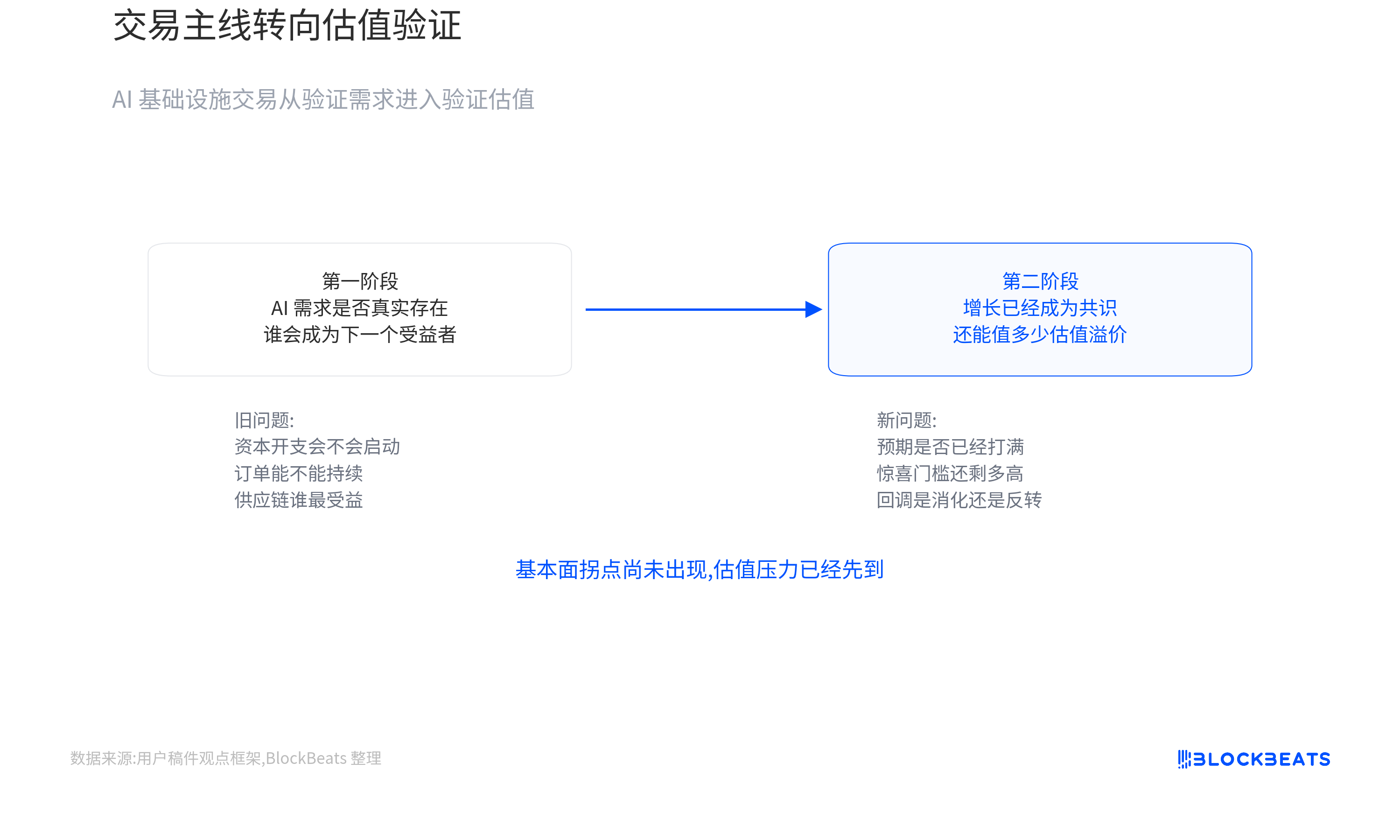

Demand Has Not Cooled Down, But Is Accelerating

From a fundamental perspective, Broadcom's earnings this time did not show any significant signs of cooling down. In the second quarter, AI infrastructure-related semiconductor revenue reached $10.8 billion, a 143% year-on-year increase; the third-quarter revenue guidance is approximately $16 billion, indicating that there is still a possibility of further acceleration in growth.

Of particular note is the visibility of orders. In the AI industry chain, short-term revenue growth is not uncommon, but whether orders can continue to extend into the future determines how the market assesses the length of this round of capital expenditure. The information provided by Hawk Tan is quite clear: demand still cannot be fully met, and orders have already been covered up to 2028.

This means that at least in the exchange chip, custom computing chip, and interconnect infrastructure segments where Broadcom operates, cloud providers are still proactively securing capacity for larger AI clusters. Over the past two years, the market has always been concerned about whether AI infrastructure construction will suddenly slow down at some point, but from Broadcom's financial report, this turning point has not yet appeared.

Stock Price Plunge, Market Sells Not Performance

The market has long ceased to simply trade on current performance.

In the past year and a half, AI infrastructure has become one of the most crowded trades in the global capital markets. From GPUs, exchange chips, optical modules, to HBM, enterprise storage, and data center power equipment, almost all race tracks related to the expansion of AI clusters have undergone a significant round of valuation reassessment.

When investors believe that the AI investment cycle will last for several years, what they are buying into is not just this year's profit, but the growth expectations for the coming years. Therefore, a seemingly counterintuitive but very common phenomenon in high-growth sectors has emerged:

The better the performance, the higher the market's expectations; the higher the expectations, the harder it is for the financial report to truly bring surprises.

Broadcom is facing exactly this issue this time. The company not only delivered high-speed revenue growth data but also signaled that long-term orders are still sufficient. However, for funds that have already factored in a lot of optimistic expectations, merely proving that growth still exists is no longer sufficient.

What the market truly anticipates is a stronger "second-layer surprise": a significant upward revision of AI revenue targets, order sizes significantly larger than previously estimated, a new round of demand surge beyond the market's original model, or further supply bottlenecks driving industry pricing power higher.

In a highly crowded trade, there is often a huge difference between "continuing rapid growth" and "significantly exceeding expectations."

Photonics Modules and HBM Falling Together, What Does It Indicate?

More noteworthy than Broadcom's own decline is the synchronous reaction of the industry chain.

After the financial report was released, Lumentum (LITE) fell by about 5%, Coherent (COHR) fell by about 4%, and storage-related companies like Micron (MU) also experienced a synchronous pullback. These companies belong to different sub-sectors, yet they faced sell-offs at the same time.

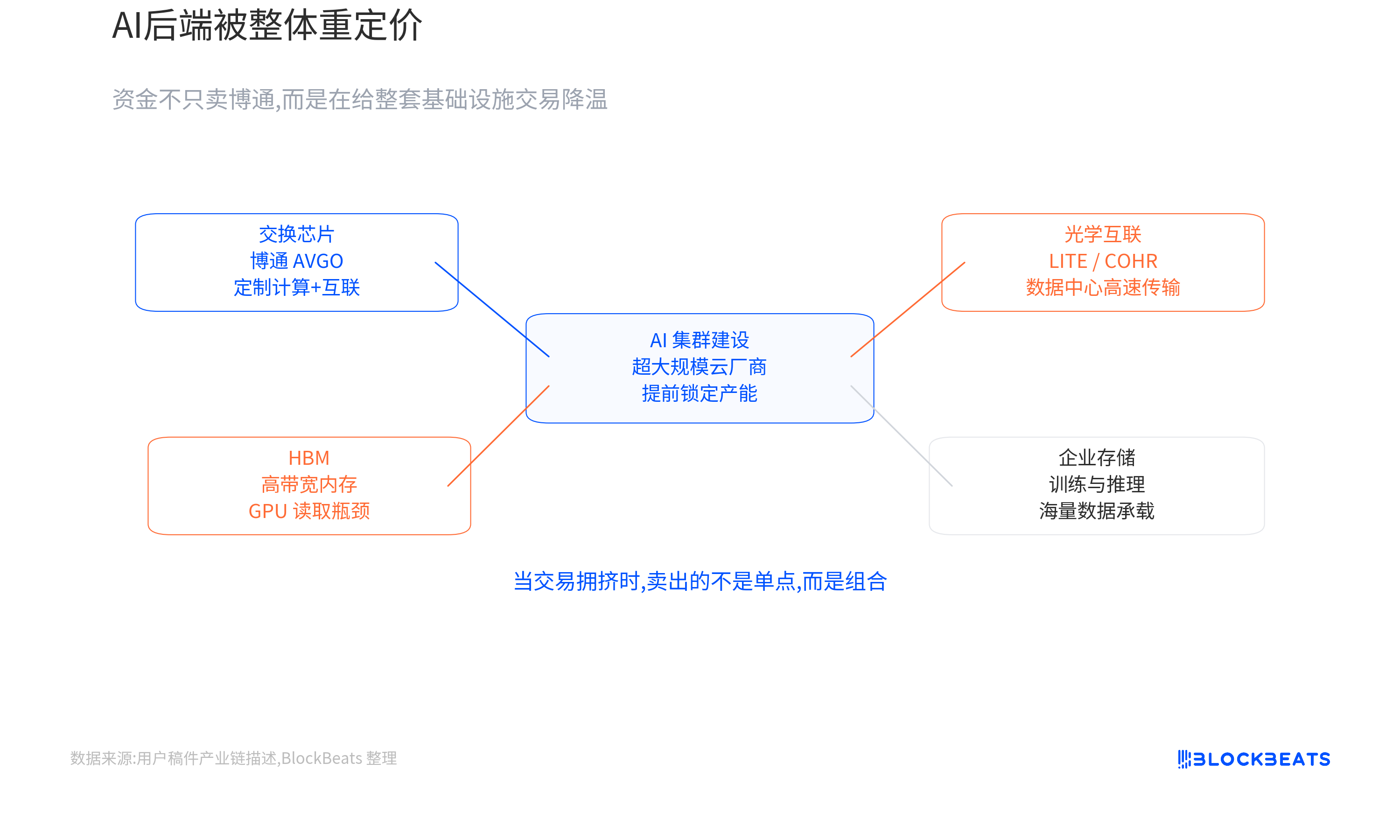

The reason is not complicated. Over the past two years, the market has gradually incorporated them into the same set of AI infrastructure trading logic: optical modules address the high-speed transmission bottleneck within data centers, HBM enhances the data read capabilities of GPUs and accelerators, switch chips are responsible for connecting large-scale GPU clusters, enterprise storage carries the massive data during training and inference processes, and data center power equipment provides energy support for high-density computing clusters.

Together, they form the AI backend infrastructure.

Therefore, when funds begin to reduce the risk exposure of the AI infrastructure sector, the sell-offs are often not of a particular company but of an entire set of trading portfolios.

This is markedly different from the market environment in 2023 and early 2024. At that time, the most pressing question for investors was:

Who will be the next AI beneficiary?

And now, the question is shifting to:

How much are these already identified beneficiaries really worth?

As the market's discussion shifts, so does the trading logic.

Cloud Providers Still Spending, but Valuations Facing Scrutiny

Taking a broader view reveals another seemingly contradictory yet rational phenomenon.

Large cloud providers are still maintaining high capital expenditures. Recent capital expenditure plans announced by Microsoft, Google, Meta, and Amazon remain elevated. Large AI clusters are still being built, GPU procurement scale is expanding, 1.6T optical modules are gradually entering a mass production cycle, and HBM supply remains tight.

So far, the market has not seen clear evidence indicating that AI capital spending has peaked.

In other words, the demand side has not undergone a significant change; what has changed is how much the market is willing to pay in terms of valuation for these demands.

Over the past two years, investors have repeatedly asked: Is the AI demand genuinely present?

Now, the market is entering a new phase: AI demand is indeed present, but has the current valuation already priced in the growth for the next few years?

These are two entirely different questions. The former determines whether an industry trend can establish itself, while the latter determines whether a stock can continue to rise.

The Market is Repricing AI Growth

Putting a few data points together paints a fuller picture than "great earnings but stock plummets": Broadcom's orders are still growing, cloud providers' capex is still expanding, AI infrastructure demand remains strong, yet related stocks are seeing a significant pullback.

All four can be true simultaneously and not contradict each other.

Because what the market is currently trading is no longer whether AI will grow.

It is:

When growth is already consensual, how much is AI's growth actually worth?

For the AI infrastructure sector that has undergone a valuation reassessment over the past two years, this may be the truly notable change to pay attention to.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia