AI is the Nerd's Opportunity, Agent is the Money's Opportunity

Venture capital, A16Z, and other MegaFunds have always told us a story about cycles and exits, but for Solo GPs, it appears more like a signal and structure harmonic vibration. You need to find the true pattern they haven't mentioned.

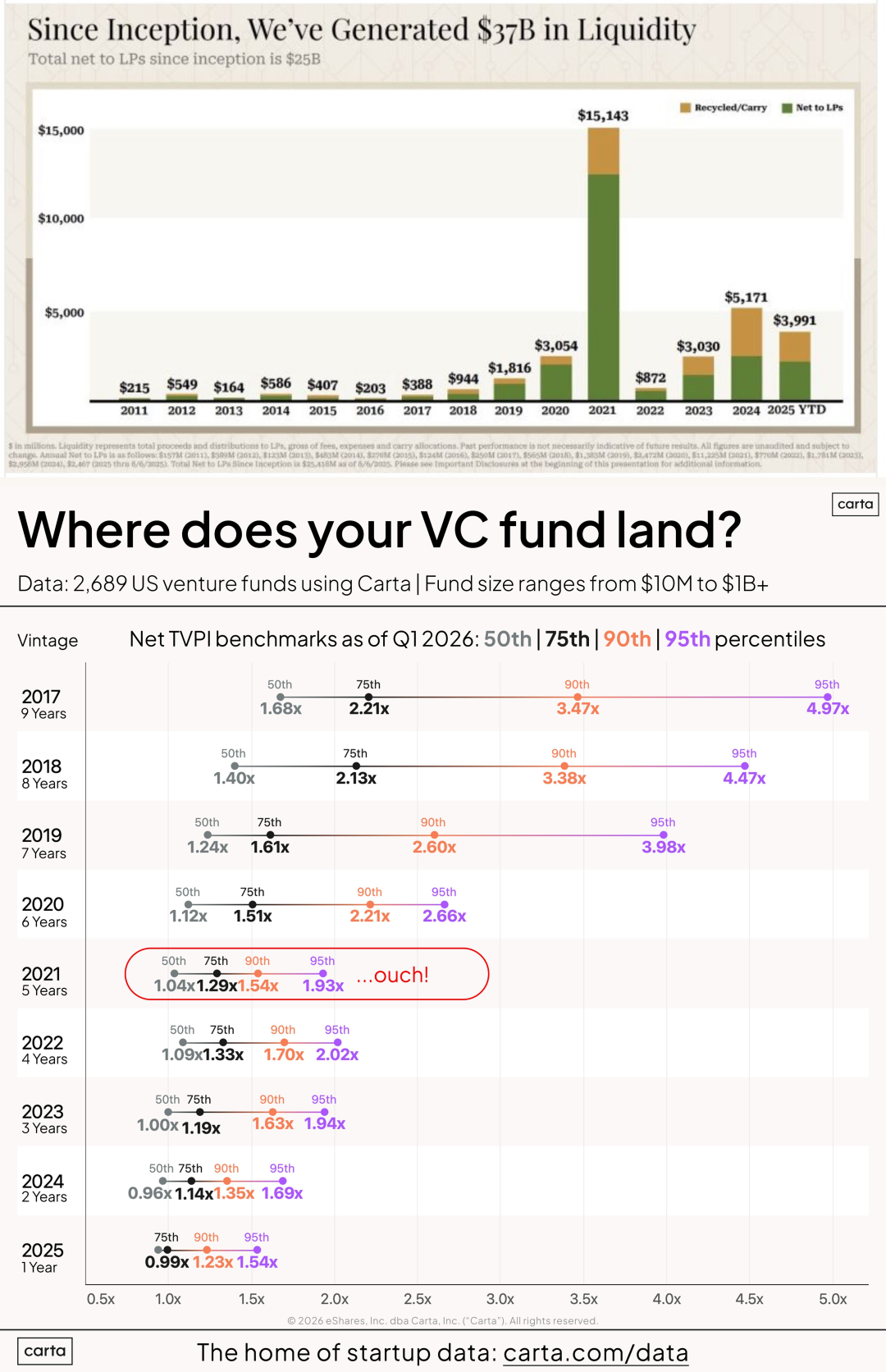

In 2021, a16z returned $12.5 billion in profits to LPs, a DPI higher than the sum of the previous decade. However, 2021 also marked the beginning of a disaster for the U.S. VC industry. Apart from tangible DPI, it was just paper gains.

In other words, 2021 was the golden age of exits, where LPs could tangibly receive their returns. But if LPs reinvest, they will have to endure the pain that has persisted until now.

All this tells the opposite narrative. The volatility of the crypto market also synchronizes with this. The Metaverse concept in 2022 set Web 3 on fire, even forcibly extending the bull market until early 2025, when Binance's "BFF Coin" farce drew a line under VC coins.

Today, most VCs have fallen into a silent mode. Economies of Scale have been dragged into a heavy capital model of computing power and data, unable to break even. The network effect has no place on-chain, heading towards institutionalization and surviving on SaaS channel fees.

However, looking at the history of venture capital, in each round of interest rate hikes or cuts, the water released will nurture different VC models. We will invent the valuation logic of risk over and over again, and the relative freedom of the crypto market will also allow the savvy players in this market to discover the most profitable signaling mechanisms.

When VCs No Longer Take Risks

"Every passion starts with an external object that impacts the sensory organs, causing the animal spirits to move through nerve motions."

If you still remember, in March and April 2021, Roblox and Coinbase chose the Direct Listing method for their public debut. Setting themselves apart from the traditional IPO, a direct listing involves selling only existing shares, without underwriters and lock-up periods.

Interestingly, both were led by A16Z. Amidst the dazzling DPI data, in June 2021, A16Z raised $22 billion for its third crypto fund. Then, in January 2022, A16Z raised a whopping $90 billion for a new fund.

So, what was the cost?

The cost was Coinbase's stock price plunging 90% from its peak in 2023. It can be unequivocally stated that A16Z's role in the US stock market is no different from its role in the crypto VC world. However, A16Z could still raise $7.2 billion in 2024 and $15.1 billion in 2026.

Even in May 2026, its fifth crypto fund raised over $22 billion, bringing its total crypto fund history close to $100 billion.

The market presents a choice: either become an LP of A16Z, waiting for the astonishing DPI at the moment of cashout, or become the cost of A16Z, being the source of the astonishing DPI.

However, a subsequent issue arises; A16Z's signal detection in the market is not keen. In other words, every VC kingpin of each cycle will face the curse of scale. Their oversized scale hinders them from having enough motivation to discover super early-stage paradigms, especially revolutionary rather than incremental mechanisms.

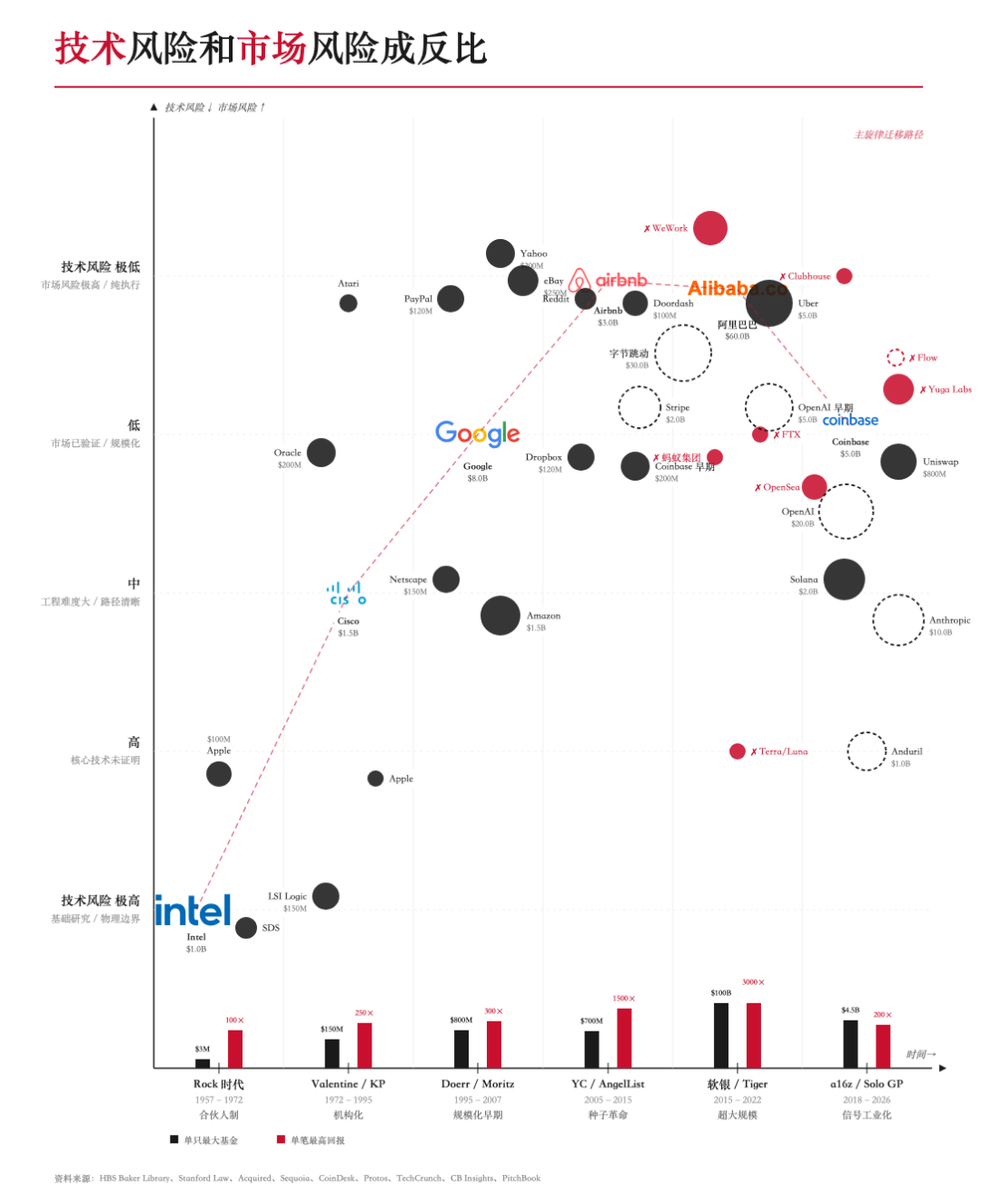

1. The father of modern venture capital, Arthur Rock, started at the pinnacle, with Fairchild and Intel pioneering the venture capital model in Silicon Valley;

2. KP and Sequoia formally introduced the institutionalized venture capital model, but were overtaken during the PC to mobile internet transition;

3. Y Combinator turned venture capital into a probabilistic system under the Big Data mechanism, churning out unicorns under the power law;

4. Masayoshi Son, with SoftBank, created the Alibaba China concept myth, turning venture capital into a Ponzi-like game at a massive scale;

That's how, as the old titans bask in past glory, new ambitious players will prove their unique vision through innovative mechanisms, secure cheap money, and embark on their adventurous new era.

Furthermore, reputation itself can be converted back into money. Paradigm founder Matt Huang invested in ByteDance, and although ByteDance cannot go public, Paradigm chose to leap into the crypto dance. In the latest news, they have pivoted towards AI and robotics.

Let's correct the answer. If you can't become an LP of A16Z and don't want to bear the cost of being trampled, then you need to discover the unscaled new signals and use new mechanisms to kill the old guard.

A gap has emerged. In 2021, A16Z was not "allowed" to participate in Anthropic's funding round. Instead, more individual investors made early bets, such as Skype co-founder Jaan Tallinn, former Google CEO Schmidt, and others leading the Series A round. FTX's SBF entered in 2022, giving us another timeless imagining of Crypto X AI.

A16Z doesn't need to take risks. SBF is efficiently leveraging retail investors' money. If you want to find the most reasonable starting point for a Solo GP, Claude's venture capital history is the most typical.

Unlike individual angels, Solo GPs operate the entire VC based solely on their research ability. In the age of Agents, we can easily understand this, but it is precisely humans who first put it into practice. Unlike YC's wide net approach, Solo GPs still need to deeply invest in each project; each deal is crucial to DPI.

A16Z has become a market indicator itself. As new technology trends emerge, newer participants try to think of ways slightly earlier than A16Z. Beyond AI's large models, they are eyeing the Agent.

There is a dangerous leap here: economies of scale cannot exist in AI's large models. For every additional human user, server costs increase, unable to spread costs like software. The network effect has not materialized as expected in Agents; interaction between Agents is still an ideal state.

Non-Human Network Effects

"In 1784, Watt improved the rotary steam engine, and in 1824, the complete theory of the steam engine was expounded by the Frenchman Carnot."

AI is all a black box, and the Scaling Law was observed by Adi Wang at Baidu. The math required for Transformers does not exceed the level of a graduate student, but why it surpasses a graduate student's mathematical level remains unknown.

AI is a Nerd's opportunity. You just need to give money to the cutting-edge group of people and then wait for miracles to happen. The popular talent acquisitions in Silicon Valley are the best proof: Researcher> Data> Model.

However, large models themselves are difficult to recoup costs, emphasizing once again the backlash against economies of scale. Even transitioning from training to inference, even transitioning from conversation to task, cannot stop this process.

The only way out for AI large models is to become a traffic center like AWS or CloudFlare. If it is destined that production-side costs cannot be reduced, then consumer-side growth must be unlimited.

Agent is an opportunity for Money. Agents must become the consumer subject, where the subject is unlimited and the consumption is infinite. This is the root cause of Agents calling each other becoming a mainstream topic.

But to a considerable extent, Agents and Bots are indistinguishable. It is unclear what an Agent is, as it seems that Bots have long existed.

If we must define an Agent, the "evaluative agent" in reinforcement learning is the origin of this round of technological trends. In DeepMind's thinking, enabling the agent to autonomously evaluate training success is crucial for the next step in intelligence enhancement.

This differs greatly from Claude's role division from coding. From a programming perspective, an Agent is actually a role mapping for human programmers. When we talk about Agentic Coding, we are already far off from AlphaZero's Agent.

Only from this perspective can Agents substitute for people and Claude's impact on SaaS hold water, which is nothing more than the continued iteration of a human outsourcing mechanism:

1. Moving towards high-value scenarios, after programmers come accountants and analysts;

2. Moving towards fewer full-time employees, outsourcing is followed by multiple agent invocation fees.

However, a problem still exists. Agents do not exhibit human social relationships, and real business relationships do not become smooth by applying agents. Humans still prefer to interact with other humans.

We have indeed created more agent scenarios, which work well in "internal" coordination, such as large companies using layoffs to switch to GPUs.

But in "external" collaboration, one must be cautious. As of May 2026, the U.S. witnessed strong job growth, with non-farm employment increasing by 172,000, mainly in blue-collar sectors like leisure and hospitality and healthcare, while the financial sector saw a decrease of 22,000 jobs.

The human society's fear of agents is indeed real but greatly overestimated.

Of course, just like whether the Sahara needs shoes, this can also continue to enhance model intelligence, further increase agent capabilities, and signal investments in robotics.

In other words, the economics of agents only holds true in theory; consumption-side infinite growth has not materialized. The continued bet is, how can agents be invoked with each other to create network effects?

The Era of Crypto Placeholder Agents

"Evolution does not always lead to increased complexity; evolution does not always follow an upward trend."

Let's summarize what we know as a warning for the unknown.

Venture capital cannot represent an effective exploration of technological signals; this has become a game for the few brave souls;

Agents have been mass-produced forcibly, with hopes of reducing the production cost of large models, but natural invocation relationships are not established between them.

These two seemingly contradictory discourse systems involve clever coordination—finding signaling mechanisms that stimulate agent invocation.

Merely issuing Agent assets or trying to make a DeFi protocol Agent-centric is meaningless. The blockchain is already crowded with few humans and many bots. Adding smart contract calls will only increase technical risk, making this path far from straightforward.

In practice, human agency cannot be replaced by Agents, as role mapping relies on business relationships. Trust in innovation is not achieved in a vacuum, the US and China do not see eye to eye, and the technological boundary is narrower than we imagine.

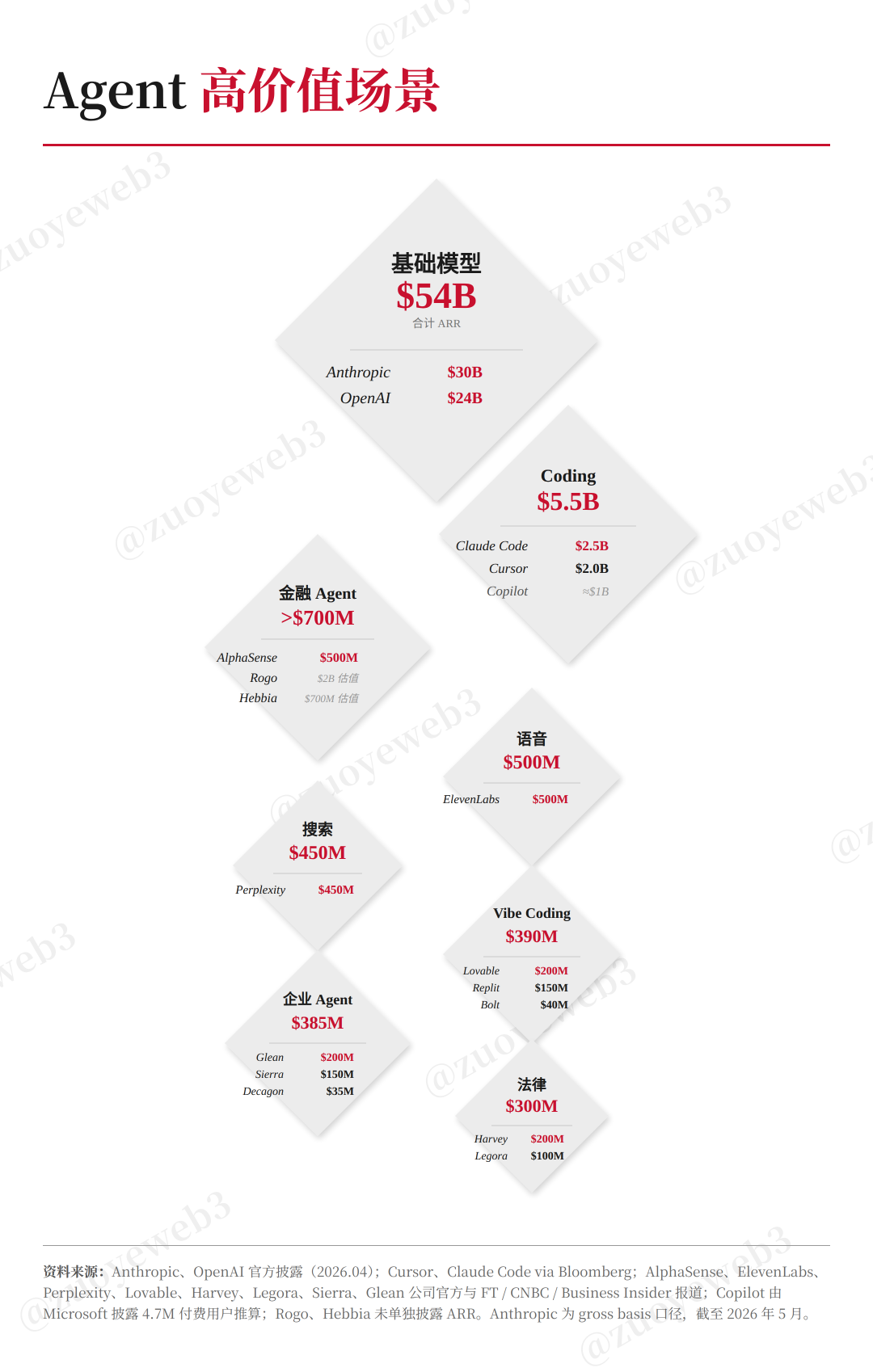

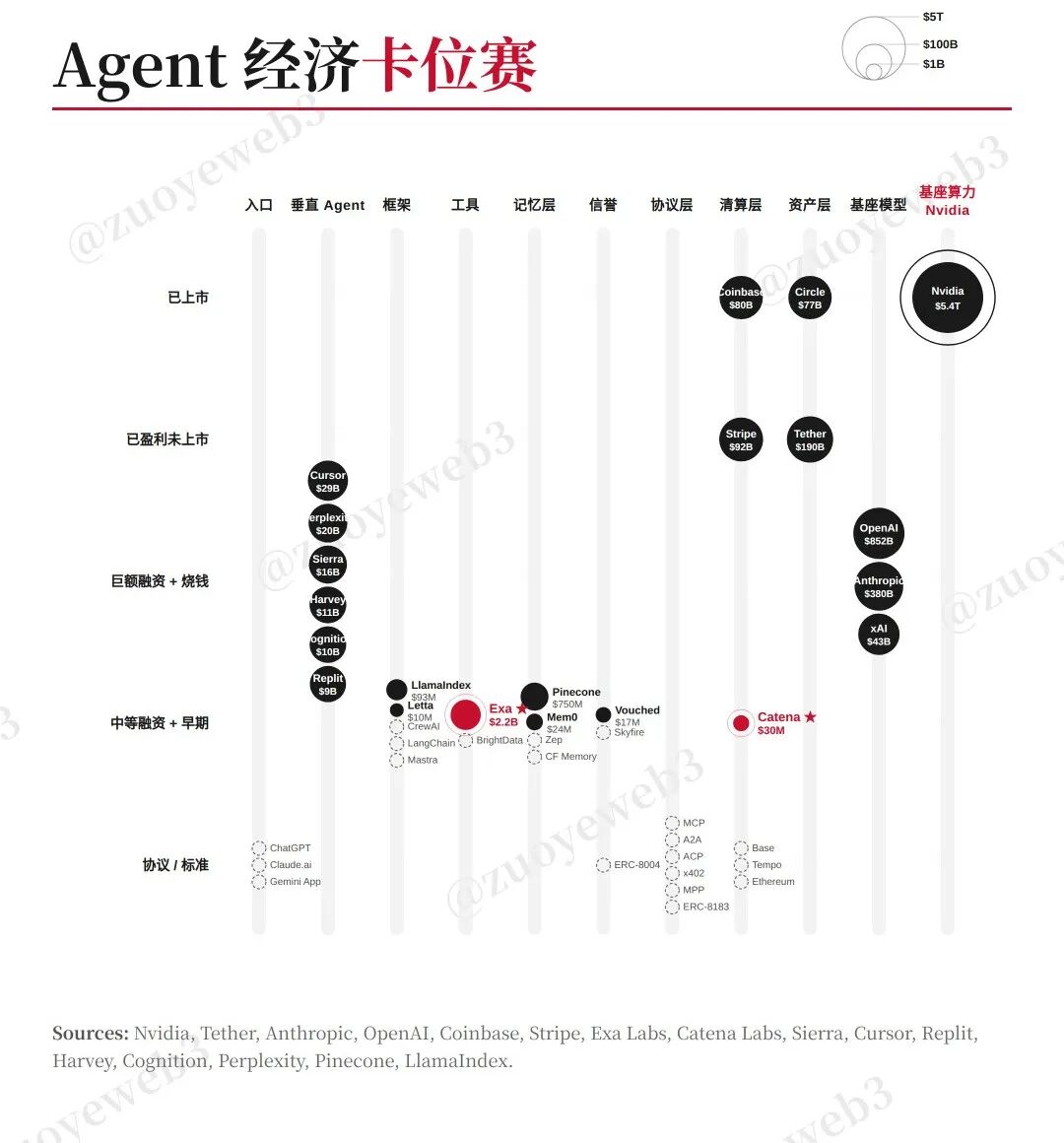

Exa aims to meet the demand for Agent real-time and high-quality data, one-time cleansing, multiple calls, which represents true economies of scale. However, it is challenging to trigger calls between Claude and Codex.

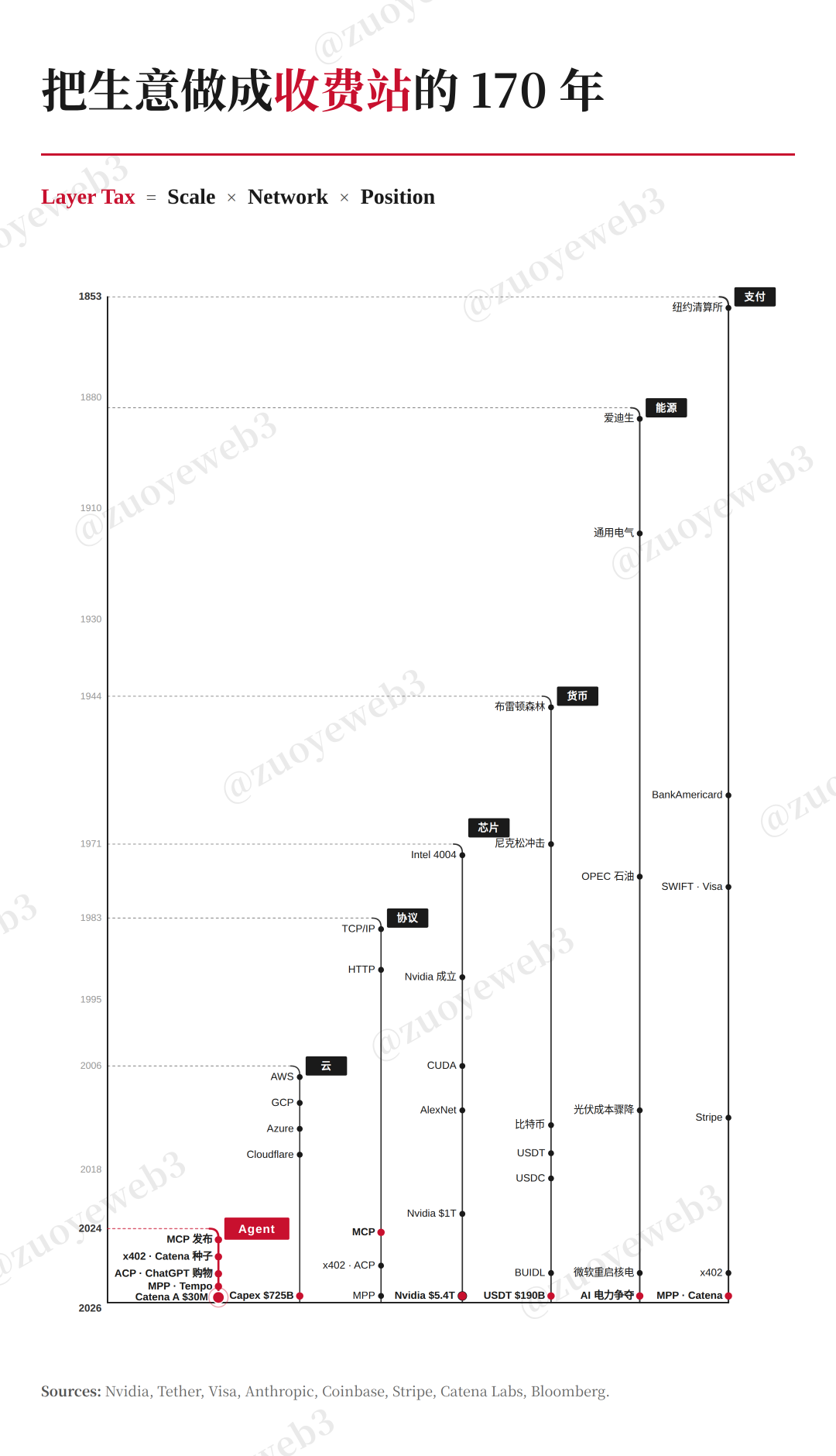

Catena caters to the compliance financial needs among B2B Agents, even requiring an OCC license to facilitate B2B compliance. This represents a specialized version of network effects, but it is challenging to reduce the cost of scale usage.

On the other hand, various payment protocols represented by stablecoins seek to tap into the demand for C2C entry points and settlement exits, lightweight protocols to reduce usage costs, microtransactions reduce collaboration costs.

However, it is still not enough. To achieve the ultimate A2A daily communication, it is necessary to make humans willing to devote their souls, following a three-step approach similar to TrueNorth:

1. Let people use Agents to assist in transactions;

2. Let Agents learn from human participation in transactions;

3. Let Agents take the lead in on-chain transactions.

Compared to Claude's access to IBKR's policies and legal restrictions, which can only become a kind of CoPilot, TrueNorth's use of Hyperliquid for live trading is not difficult.

But making humans willingly accept Agent guidance is still a distant goal, at least more distant than VCs imagine.

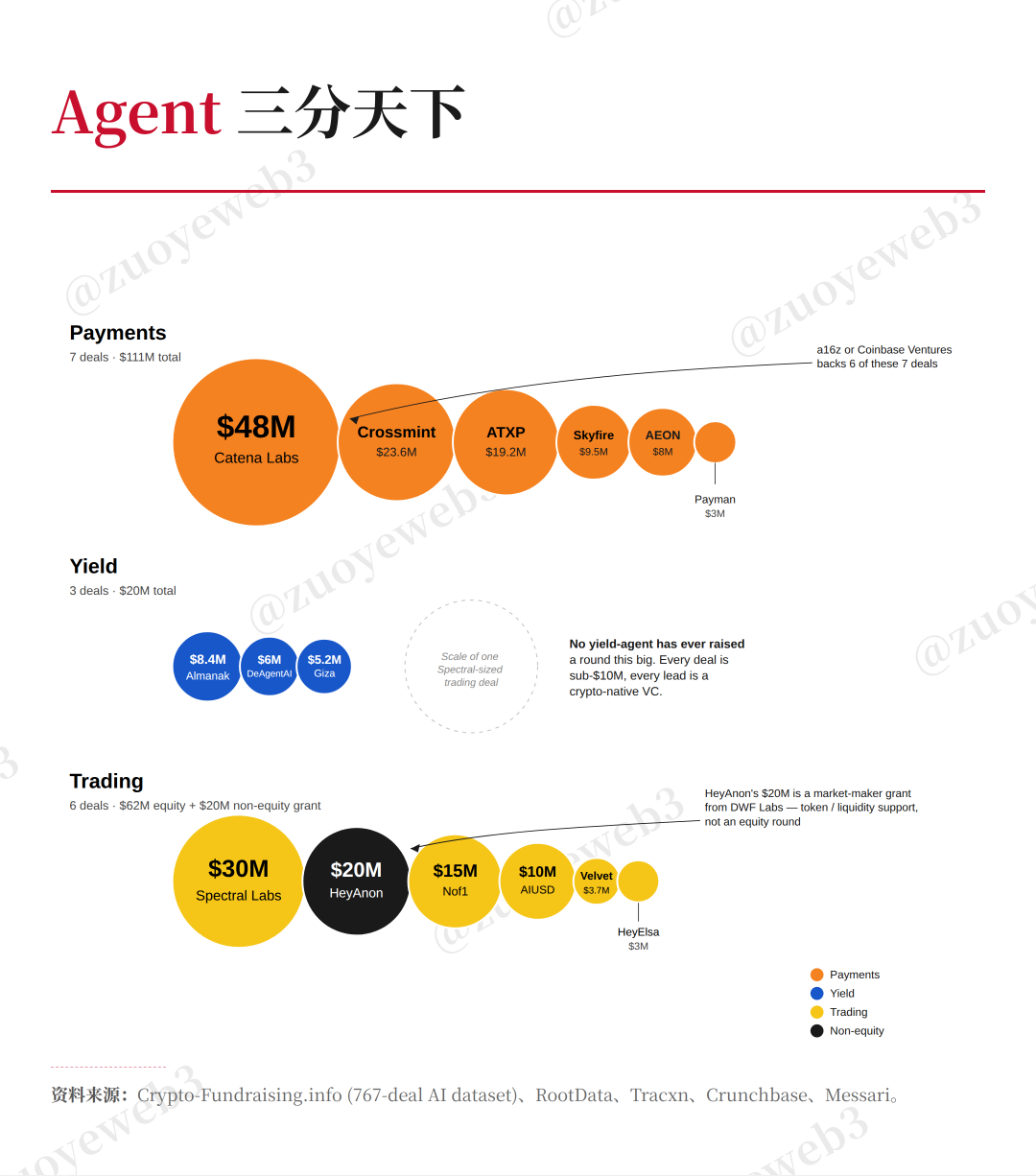

In the attempt of Agent+Finance, the "Pay First, Trade Second" approach dominates the landscape.

Payments are very certain, with the market share of PayPal and Stripe being tokenized into stablecoins, which in turn will be agentized.

The trading outlook is promising, from Simmons to Jane Street, and the never-ending magic square of Liang Sheng'en, sparking infinite VC imagination.

However, all of this is quite different from the envisioned scenario where Agents take over transactions and payments.

Quantum establishes "computing power supremacy," still holding a speed advantage relative to humans, while transactions establish "channel advantage," still enjoying preferential rates compared to banks.

A gap emerges here; VCs want to facilitate a situation where people are willing to be actively replaced by Agents. A16Z is powerless in this regard. Money cannot ensure the success of new social platforms like Clubhouse and Towns Protocol. Thus, for more complex financial Agent scenarios, all that can be done is to lie flat directly.

Drawing from the successful experience of DeFi, allowing Agents to touch funds, verifying feasibility at low frequency and small amounts can pave the way for high-frequency, large-scale daily use.

Imagine a scenario where the roads are filled with FSD Tesla Robotaxis, which is actually safer than a mix of human/AI driving. However, to make this happen, humans need to act as guinea pigs:

1. A few people use AI-assisted driving to establish technological parity with human drivers;

2. Reduce the mortality rate of a few people using AI-assisted driving and establish a compensation mechanism.

In other words, establishing a mechanism for Agents to touch money will be easier to convert users than making Agents earn money. Only when the Agent has gathered enough money usage experience can humans stop thinking and simply click confirm all the way.

Only when Agents actively participate in the market can market efficiency and security be enhanced. It can be understood in this way: Agent's pursuit of profit is the process of improving market efficiency, gradually self-bootstrapping, writing C++ with C++, and optimizing Agents with Agents.

Trading is the end goal for Agents, but before that, you must go through a long elliptical runway.

In this high-value financial scenario, blockchain is an open financial experimentation ground, stablecoins are proof of the Agent-optimized market process. This is not about scale and resource input; it is about establishing mechanisms and expansion.

Conclusion

“Life is full of cycles. Without cycles, there would be no era dividend, and the new generation would always surpass the old.”

VC is becoming smaller and more personalized. Whether it's a Solo GP or an OPC, the trend of Solo GPs investing in OPCs has not yet become mainstream. Amid the uncertainty of technological trends, we do not know which paradigm will prevail.

After the dot-com bubble in the early 2000s, which gave rise to a dividend lasting over 20 years, we are now entering a new era of “Agents eating software.”

An Agent is a development tool and a sign of productivity evolution. However, software developed using Agents has not yet become ubiquitous. Following the IPOs of SpaceX, OpenAI, and Anthropic, the era of foundational large-scale models is coming to an end.

If we are entering a new era of long-term dividends, then new crypto VCs like Dragonfly, ParaFi, Haun, Paradigm, and a16z will continue to scale up. They may also launch market-specific funds such as 5cc to showcase their strength amidst the new deployment frenzy.

Even the entire DeFi industry will undergo a paradigm shift. Through the innovation in the financial system over the past two Kondratieff waves, this time, Agents and stablecoins will mark the beginning of a dual-core revolution.

Crypto is small, but the world is vast. Let's witness this together!

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia