TL;DR

· ZeroHedge suggests that after the opening of SPCX options, a gamma squeeze may occur, potentially pushing the stock price to $400.

· Currently, we can only confirm that the volatility channel has been opened and cannot consider $400 as the market consensus.

· Related Tickers: SPCX, NVDA, MSFT, AAPL, SQQQ, SOXS.

ZeroHedge posted on social media that after the opening of SPCX options, a gamma squeeze may occur, driving the SpaceX stock price to $400. ZeroHedge is a highly influential and aggressively styled financial media and trading account in the U.S. stock market, known for integrating discussions on macro liquidity, position structure, and extreme trading scenarios. This time, it directly linked SPCX's option listing, gamma squeeze, and a $400 stock price together.

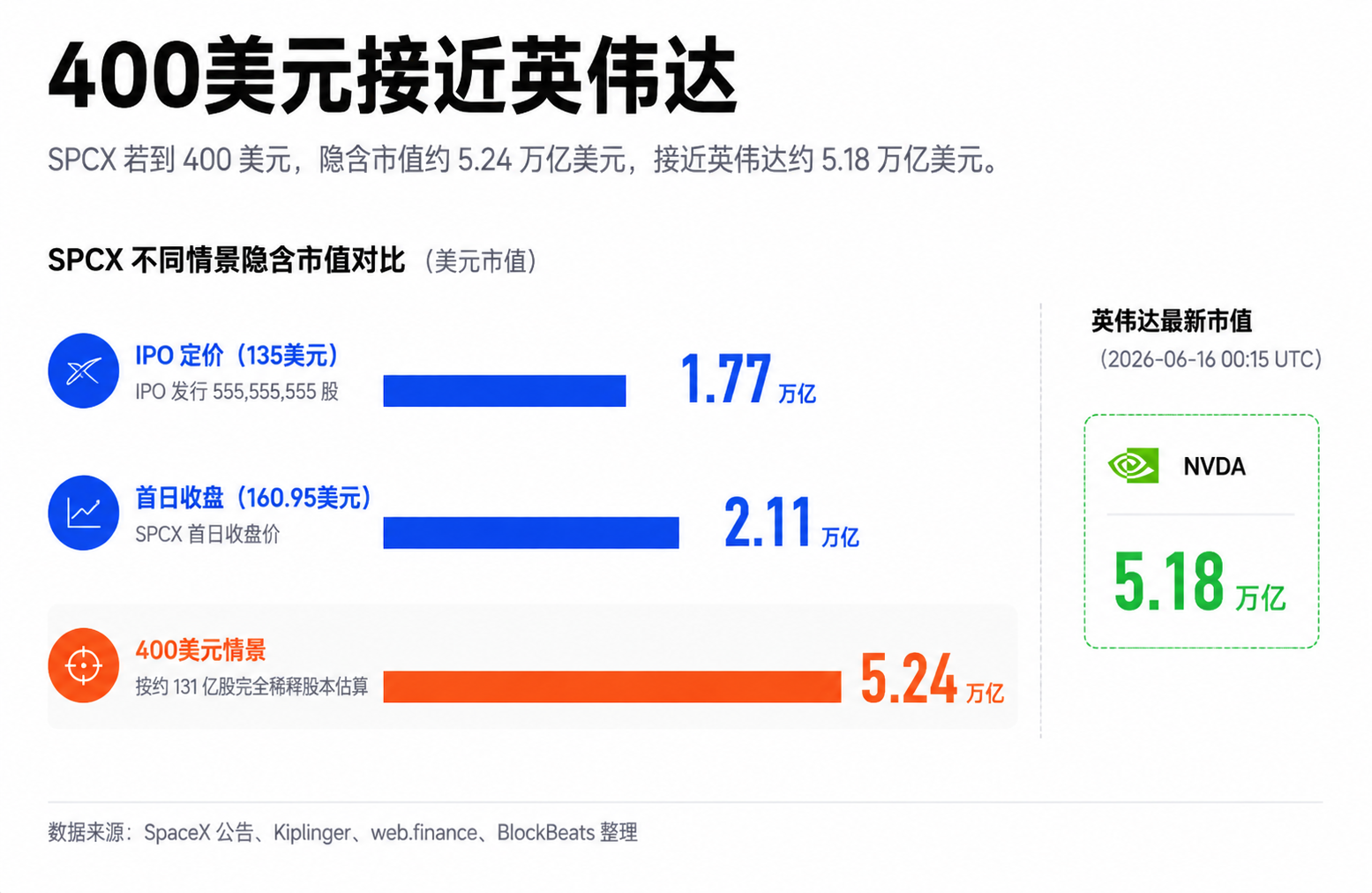

SPCX surged over 25% on its first day of trading, surpassing a $2 trillion valuation. Overnight and after-hours quotes briefly approached $230, but this is not the official closing price and cannot directly represent long-term funds willing to transact at this price. For the average reader, the key point is not how many shares were issued in the IPO, but the limited tradable chips in the early trading period, highly concentrated retail buying, and the upcoming options opening.

This is where the discussion about $400 truly becomes relevant: the number itself is very exaggerated, but it points to a market structure that needs attention. ZeroHedge believes that the combination of SPCX's low float, retail buying pressure, and option listing may trigger a significant gamma squeeze. Based on an estimated fully diluted share count of about 13.1 billion shares, a $400 price corresponds to a market capitalization of around $5.2 trillion, placing SpaceX very close to, or even momentarily surpassing, NVIDIA.

Why Does SPCX Experience Penny Stock-Like Volatility?

SPCX's uniqueness lies not in being a small company but in having a scarcity of early tradable shares.

A low float refers to a limited proportion of freely tradable shares in the market. Even if a company has a large total market value, if only a small portion of shares are initially available for trading, the short-term price can be more sensitive to buying pressure. The pool is large, but there is not much water available for trading.

This is also the difference between SPCX and Apple, Microsoft, and NVIDIA. Mature large-cap stocks have a significant floating stock, institutional ownership, index funds, market makers, and arbitrage funds. To move the market cap of such stocks by hundreds of billions of dollars in a day requires a large amount of capital and a broader consensus.

SPCX is in the early stages of its listing. SpaceX's official announcement confirmed the IPO issuance size and oversubscription arrangement, but the initial public float ratio remains relatively low compared to the company's overall valuation. The combination of a low float and the Musk narrative may cause the stock price to resemble more of a newly listed stock under concentrated buying pressure in the short term, rather than a mature mega-cap stock.

This also explains why the after-hours price was closely watched by the market. Post-market trading has lower liquidity, thinner order books, and once funds start chasing the same stock, price elasticity is amplified. The after-hours price briefly approached $230, indicating tight chips at that time, but it does not directly indicate that long-term investors have accepted this valuation.

ZeroHedge's $400 price extrapolation is rooted in this: if a trillion-dollar company has short-term trading dynamics similar to a low float penny stock, it could experience price jumps rarely seen in normal mega-cap stocks.

Options Bring Leverage to Volatility

The significance of options lies in transforming retail directional bets into passive hedging demand from market makers.

According to Reuters, SPCX options are expected to start trading as early as Tuesday, with Cboe expected to open on Tuesday. The report cited market sources' expectations that early trading may be heavy, highly volatile, and options premiums may be expensive.

For ordinary investors, this means that SPCX is no longer just about buying the underlying stock. After options are listed, the market will see a large number of cheaper, higher leverage, and higher risk call options.

The most emotionally charged are out-of-the-money call options, contracts where the strike price is above the current price. They are relatively cheap, more like lottery tickets. If the stock price rises fast enough, the returns can be significant. If it doesn't rise, the options can quickly go to zero as well. Retail investors usually prefer these contracts on hot stocks because they allow betting on larger price increases with a smaller initial capital.

The core mechanism of gamma squeeze occurs here.

When a large number of investors buy call options, the other side selling the options is usually the market maker. To control risk, market makers often need to buy some of the underlying stock for hedging. The higher the stock price rises, the closer the options are to being profitable, and the more stock the market maker may need to buy. This sets up a positive feedback loop: retail investors buy call options, market makers buy stock, as the stock price rises, market makers continue to buy more to hedge, which attracts more buyers, leading to further price increases.

Applied to SPCX, this mechanism offers a lot of potential. It combines a low float, a popular narrative, retail investor attention, an open window for options trading, and dramatic price fluctuations already seen in the early stages of listing. ZeroHedge believes that once the demand for out-of-the-money call options is concentrated enough, market maker hedging purchases could quickly drive the stock price to $400.

The boundary also needs to be drawn. The $400 price target is an extreme upside scenario provided by ZeroHedge, not a baseline judgment that current evidence can independently support. The upcoming options launch only indicates the emergence of a new leverage channel. To prove that gamma squeeze is forming, we still need to see the real trading volume on the first day of options trading and the following days, out-of-the-money call options open interest, strike price distribution, implied volatility, and market maker net gamma exposure.

At this point, what can be said is that the machine is ready to start. What cannot be said is that the machine has definitely started.

Vanda Data Supports Crowded Trades, But Not Equivalent to Widespread Frenzy

If we only look at SPCX's trend, it is easy to think that retail investors have entirely returned to risk assets. However, Vanda's fund flow perspective provides a narrower explanation.

According to ZeroHedge citing VandaTrack data, SPCX ranked first in retail net buying for the second consecutive trading day, with a net buy of about $93.8 million on a single day, accounting for approximately 73% of the total net retail buys of individual US stocks that day. This set of data has not been cross-confirmed through independent public channels this time, making it more suitable as a reference for observing retail crowding rather than a market-established fact.

Even so, this perspective still supports part of ZeroHedge's assertion: SPCX has indeed seen a rare fund concentration. For low float stocks, concentrated buying itself can significantly impact prices. If options trading amplifies this directional bet, volatility may continue to expand.

However, this set of data also imposes constraints. During the same period, although there was a mild return flow in semiconductor stocks, there was no indication of a widespread indiscriminate spread of market risk appetite. Short ETFs like SQQQ and SOXS continued to receive buying interest, indicating that retail investors are not pouring into risk assets across the board but rather focusing on the singular narrative of SPCX.

This distinction is crucial.

If it were a broad-based expansion of risk appetite, SPCX's rise could be understood as part of overall market sentiment. If it is a concentration on a single target, the faster the rise, the more fragile the position structure. The more concentrated the funds are, the stronger the short-term upward momentum, but once expectations are disappointed, option premiums fall, after-hours liquidity deteriorates, the reversal move will also be more intense.

This is also the most easily misinterpreted aspect of SPCX compared to Nvidia's market cap. Nvidia's valuation comes from the continuous validation of AI chip revenue, data center demand, profit margins, and long-term growth expectations. The current short-term trading of SPCX is more driven by the liquidity structure since its IPO, Musk's narrative, and expectations of options leverage. Both could be overvalued, but the underlying support mechanisms differ.

$400 Option Chain Validation

The most critical variable for SPCX going forward is not whether more people are calling for $400 on social media, but what the option market actually looks like.

If ZeroHedge's extreme scenario is to materialize, we first need to see a sufficiently concentrated volume and open interest of out-of-the-money call options. Just having options listed and actively traded is not enough. The key is whether the buying pressure is concentrated in above-the-spot price call contracts, and whether these contracts are forcing market makers to continue buying underlying stock to hedge.

The implied volatility must also be taken into account. When options are first listed, the premium may be very high. For buyers, even if the underlying stock continues to rise, if the implied volatility quickly falls, the option's gains may be eroded. For market structure, high premiums can discourage further buying, and may also lead early buyers to take profits.

The underlying stock trading volume is equally important. A low float can amplify both the upswing and the downturn. After-hours high prices may indicate liquidity stress but cannot demonstrate a willingness of long-term investors to continue buying. If the options buying pressure is not as strong as anticipated, or if there is a concentration of profit-taking among early buyers, SPCX may experience a feedback loop in the opposite direction.

Lastly, the fundamental anchor comes into play. SpaceX's long-term narrative is not weak, with Starlink, launch services, space infrastructure, and potential communication synergy being the reasons the market is willing to assign a high valuation. However, moving from around $3 trillion to above $5 trillion, in the short term, looks more like a trade structure extrapolation rather than a revaluation already validated by financial data.

In the next few days, what investors really need to focus on are the distribution of strike prices on the option chain, the open interest of out-of-the-money call options, changes in implied volatility, and whether there is still real trading volume support for the underlying stock at high levels. Only when all these data points align in the same direction will ZeroHedge's $400 scenario transition from an extreme extrapolation to a market-imposed risk that needs to be priced in.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia