TikTok influencer "Li Yien" has found his traffic password. Before reviewing the stock market every day, he always shouts a slogan, "As always, time will prove the importance of photovoltaic modules and hash rate." After shouting for more than a year, the number of likes on a single video has increased from two to three thousand to forty to fifty thousand. The netizens flooding the comments section only ask one thing: now that they are finally "in the light," is it too late?

The three words that string the netizens' anxiety together are called "Yi Zhongtian." It is not the scholar from the Lecture Room of the Hundred Schools but a nickname given by the A-share market to three leading photovoltaic module companies: New Energy Sheng, Zhongji Xuchuang, and Tianfu Communication, each taking one character. From the low point in April 2025, New Energy Sheng has increased 16-fold, Zhongji Xuchuang 17-fold, and Tianfu Communication 10-fold. Those who bought in early have made a killing.

But the story takes a turn in June 2026. On June 5, the "Yi Zhongtian" trio collectively plummeted, with Zhongji Xuchuang experiencing a nearly 8% single-day drop. On June 11, New Energy Sheng nearly hit the limit down intraday, and the CPO concept began to pull back. Those fleeing for the exit and those swarming to buy the dip completed the handover in a massive trading volume.

The story of wealth creation has been told to exhaustion. The real question that no one seriously answers is another one: if you could only choose one of the three companies, which one is the most worthwhile? In this article, we will not discuss whether it's still possible to get on board; we will only dissect one question: among Yi Zhongtian, who provides the best value for money.

In this round of the photovoltaic module market, no one has been looking at the current P/E ratio.

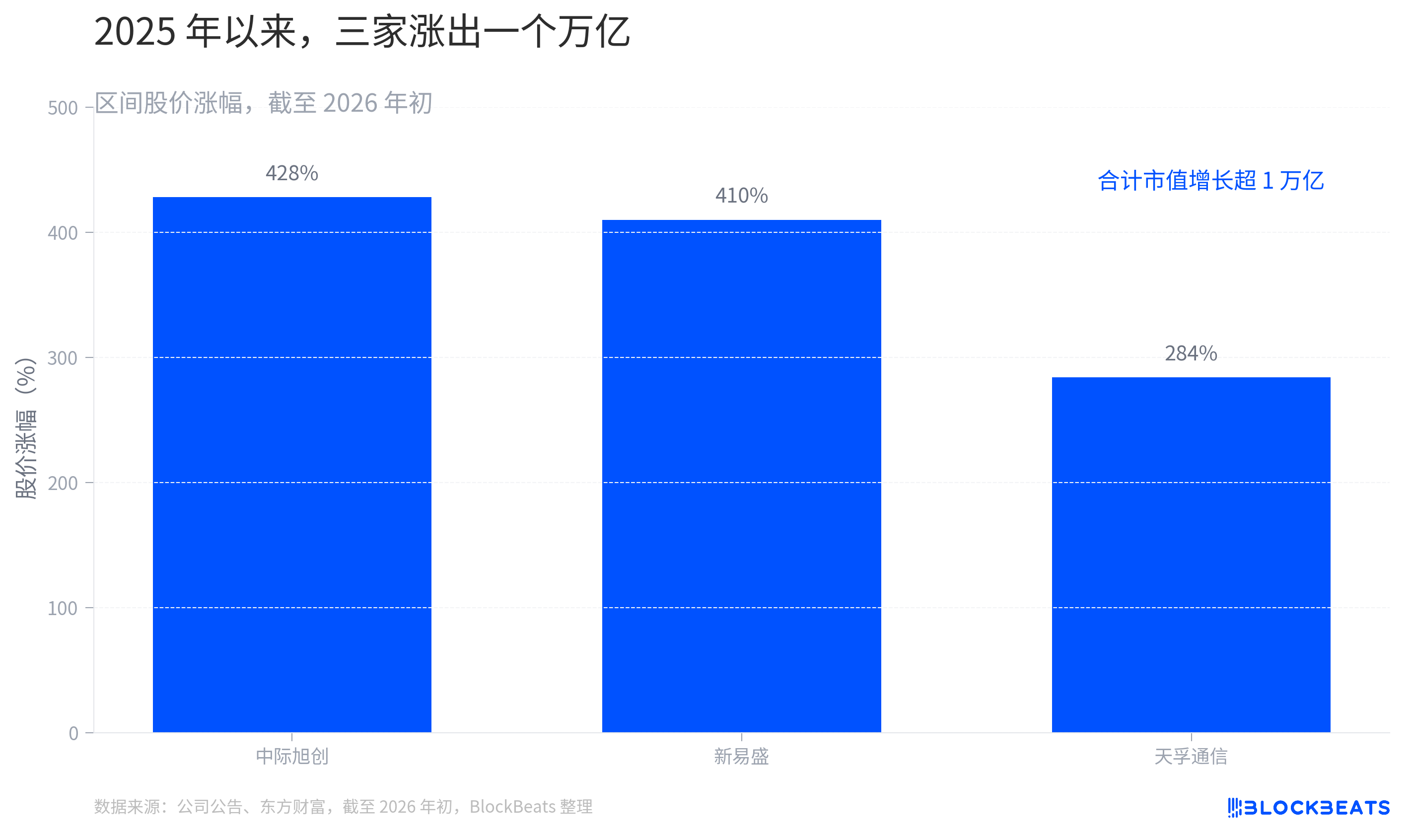

The reason is simple: when a company's profits are still growing at a three-digit rate, calculating the P/E ratio based on the past twelve months' earnings yields a meaningless number. The market's pricing anchor has shifted from "how much they earn this year" to "how much they can earn in 2026 and 2027." As of the beginning of 2026, the three companies have seen their stock prices surge since 2025: Zhongji Xuchuang by 428%, New Energy Sheng by 410%, and Tianfu Communication by 284%, with a combined market cap increase of over one trillion yuan. This trillion yuan is not a bet on the present but on the expectations for the next two to three years.

Therefore, "value for money" here is not about "which stock has a lower price" but needs to be broken down into three metrics. The first is PEG, which is the dynamic P/E ratio divided by the growth rate, measuring "how much you paid for the same growth." The second is earnings quality, evaluating whether the money earned is clean and if the gross profit margin is high. The third is a premium for certainty, gauging how much the market is willing to pay extra for "stability" and how much discount is applied for "uncertainty."

After measuring with these three metrics, each of the three companies provides a completely different answer. One is the king of value for money in numbers, one is expensive but stable in certainty, and one is the most expensive in certainty.

New Prosperity: The King of Value on Paper, but Cheapness Comes with a Reason

Let's first look at the one that is the cheapest on paper.

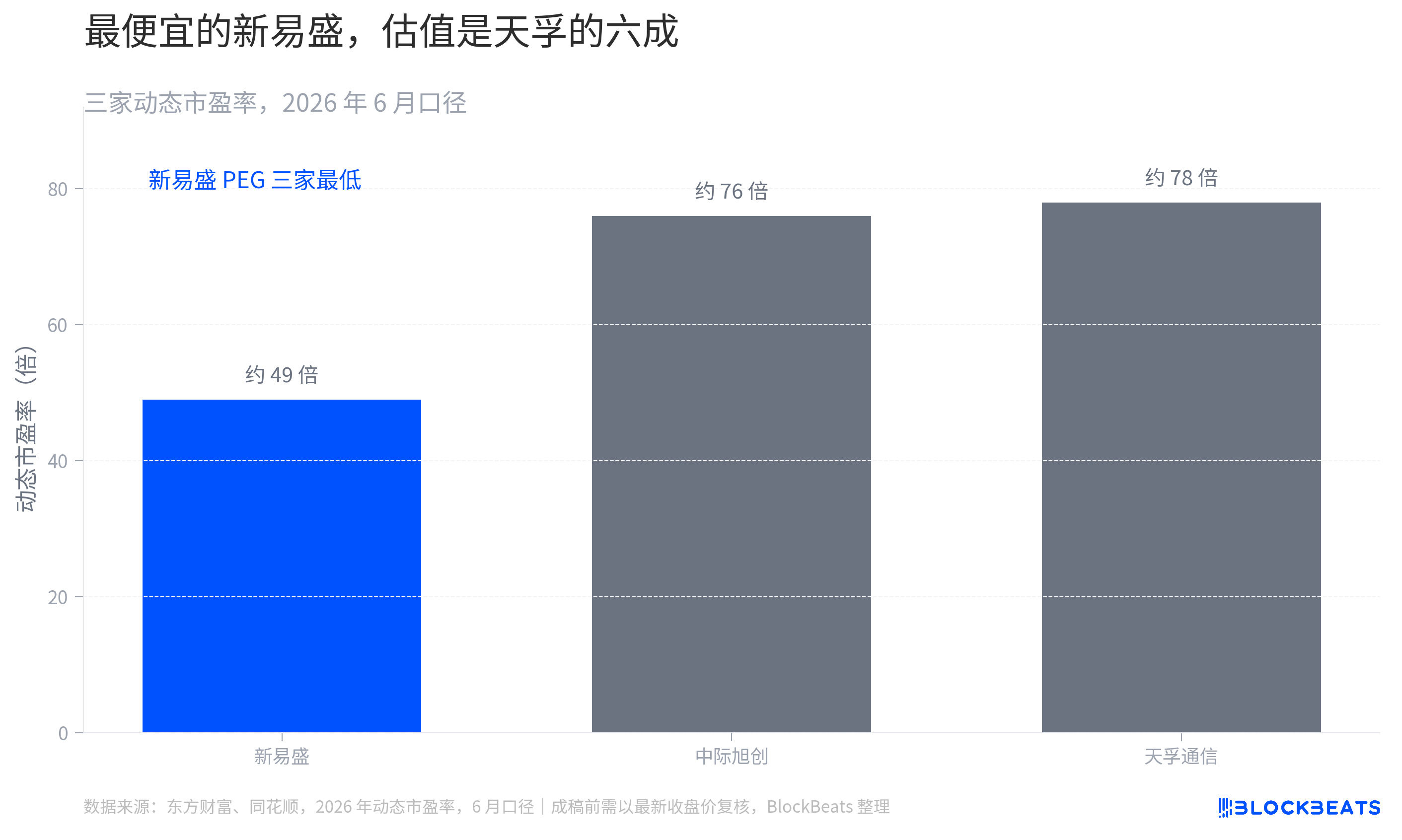

Based on the PEG ratio, New Prosperity is the most cost-effective of the three. Its year-on-year net profit attributable to the parent company for 2025 is nearly 2.5 times, significantly higher than InterSunTech's 89.5% to 128%. The net profit for the fourth quarter is also up by 39% sequentially, with an early volume release of the 1.6T product. Despite such rapid growth, its valuation is the lowest. Based on the consensus estimated net profit for 2026, its forward P/E ratio is only around 22.8 times, corresponding to a PEG ratio of about 0.30, which is the lowest among the three. For the same unit of growth, you pay the least for New Prosperity.

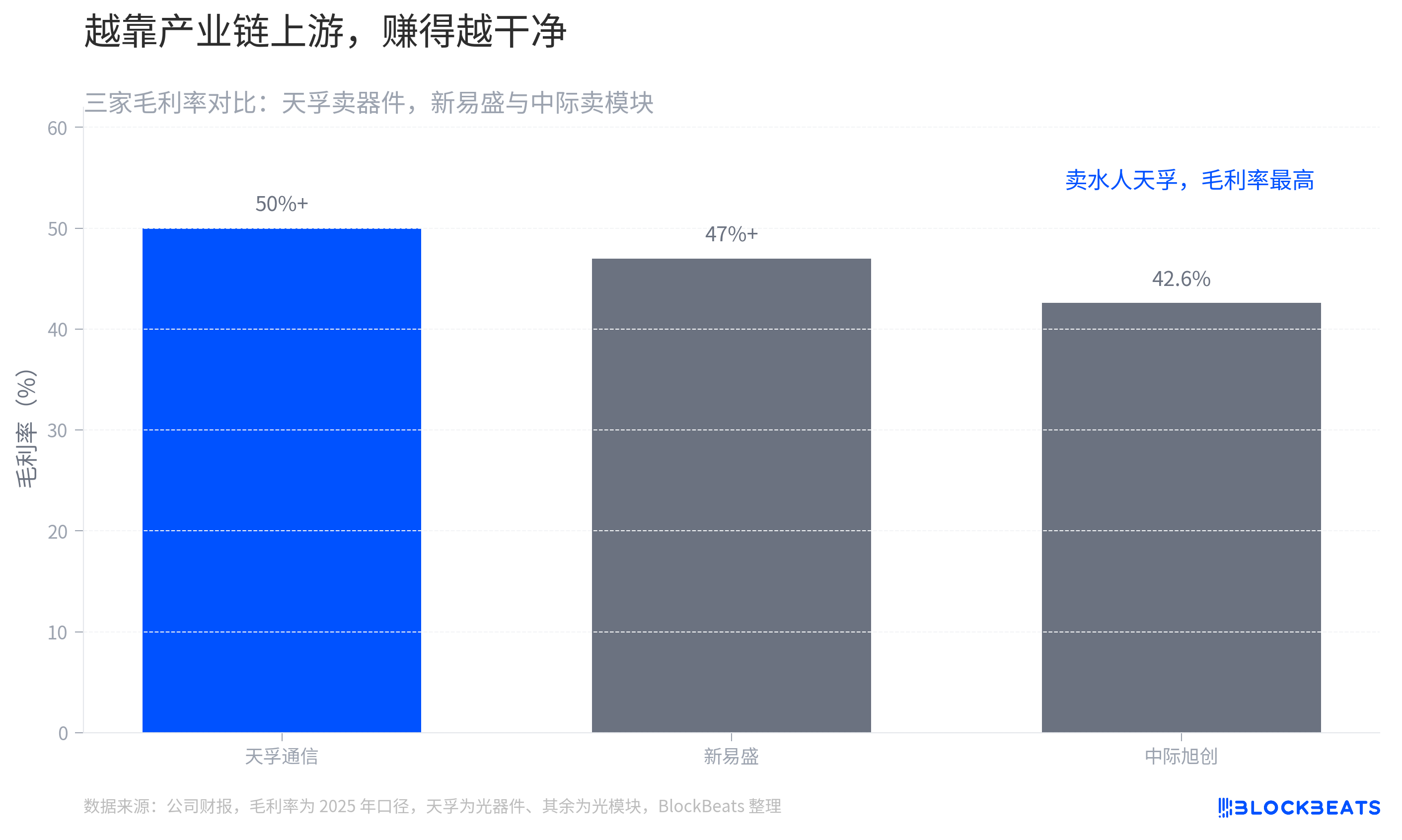

Not only is it cheap, but it also earns money the most "cleanly." In its 2025 performance, New Prosperity's non-recurring gains and losses were only 33 million CNY, and the gross profit margin was maintained at above 47%, relying on cost advantages brought by vertical integration. In terms of earnings quality, it even outperformed the larger InterSunTech.

Up to this point in the story, New Prosperity looks like an underestimated dark horse in the market. However, this is precisely the point where one should not stop at the surface. Its cheapness is a discount, not a free lunch.

The market does not give a high-growth company a discount for no reason. What New Prosperity is being undervalued for are several real risk points. It has a high customer concentration, with performance highly dependent on a small number of major clients. Its overseas revenue accounts for 78%, directly exposed to tail risks of tariffs and trade restrictions. And most crucially, whether the explosive power of the "dark horse" can be sustained. In terms of long-term technological narrative and forward-looking layout, its story is not as convincing as that of InterSunTech. The low P/E ratio the market is offering fundamentally discounts the "sustainability."

This discount is currently being partially corrected. Within 2026, New Prosperity's stock price has risen by over 79%, and it has begun preparations for a Hong Kong IPO. Capital is voting with its feet, shifting it from the "untrusted dark horse" to the "repriced leader." It's cheap, but the cheapness is converging.

Now, where does the expensive one stand?

InterSunTech: Expensive Certainty

InterSunTech's value proposition lies not in cheapness but in certainty.

Just look at a comparison. In the first quarter of 2026, InterSunTech reported a quarterly revenue of 19.496 billion CNY and a net profit of 5.735 billion CNY. The net profit for one quarter exceeded its total for the full year of 2024. During the same period, its optical communication transceiver module gross margin increased from 34.65% in 2024 to 42.61%, nearly an 8 percentage point increase. As its scale grows, so does its profitability efficiency, showcasing the demeanor unique to a market leader.

Supporting this level of certainty is market share and technological delta. Jiuzhou Xuchuang has secured over half of NVIDIA's 800G optical module procurement. With the 1.6T generation, leveraging its first-mover advantage in completing NVIDIA's validation, the market expects it to capture 50% to 60% of the market share. During last year's third-quarter earnings call, company executives made the timeline clear, stating, "Starting from the third quarter of this year, key customers will begin to deploy 1.6T and continue to increase orders... It is expected that from 2026 to 2027, other key customers will also deploy 1.6T on a large scale." To capture these orders, the company is ramping up chip reserves and expanding production capacity both domestically and internationally.

However, the cost is high. Jiuzhou Xuchuang's trailing price-to-earnings ratio once reached 73 to 74 times, more than 40% higher than Xin Yisheng's. What you pay for is a premium for "industry leadership + technological edge." This premium is suited for those who value certainty more and can afford the premium.

But certainty does not mean lack of risk; rather, its risks tend to be more of the "Black Swan" nature. On June 8, 2026 (U.S. time), Jiuzhou Xuchuang was placed on the U.S. Department of Defense's "1260H List." The company responded promptly, stating that this designation did not align with objective facts, as the company is neither a defense company nor a civil-military integration company, and it has not had a substantial impact on its operations, with orders, production, and the supply chain all functioning normally. While the response was given, for a company with overseas revenue accounting for as much as 86.8%, geopolitical issues are the real sword hanging over its head. It does not affect the fundamentals but can slash its valuation on any given trading day.

After dismantling the two module manufacturers, one significant player who is not even at the same table remains: Tianfu Communication.

Tianfu Communication: The Most Expensive Certainty, Betting on the Next-Generation Architecture

What sets Tianfu Communication apart? It does not sell modules but sells "water."

A straightforward analogy of the industry chain. If Jiuzhou Xuchuang and Xin Yisheng are restaurants directly serving diners, Tianfu Communication is the supplier to those restaurants. It sells core components like optical engines and optical devices to downstream optical module manufacturers, who then assemble them into complete modules for shipment. While it does not directly take orders from cloud service providers, its components are found in every high-end optical module.

Operating upstream gives it the highest gross profit margin among the three, consistently above 50%, and the competitive landscape is the most transparent. More importantly, it has keyed into an ultra-high-certainty long slope: CPO/NPO architecture. An institution's calculation shows that in the value chain of a high-end 51.2T switch, Tianfu Communication's cumulative potential value in the FAU, precision lens, and optical engine packaging segments is expected to reach the range of $7,000 to $10,000.

Comparing to the traditional plug-and-play era where a single server part cost tens of dollars, this is a thorough uplift in both quantity and price. No matter which modular solution downstream cloud manufacturers ultimately choose, as long as data centers continue to evolve towards a more efficient and energy-saving architecture, the position of the "water seller" remains secure.

It sounds beautiful. But Tianfu's problem is precisely hidden in the three words "water seller." It has the least elasticity, the highest valuation, and is the easiest to disappoint.

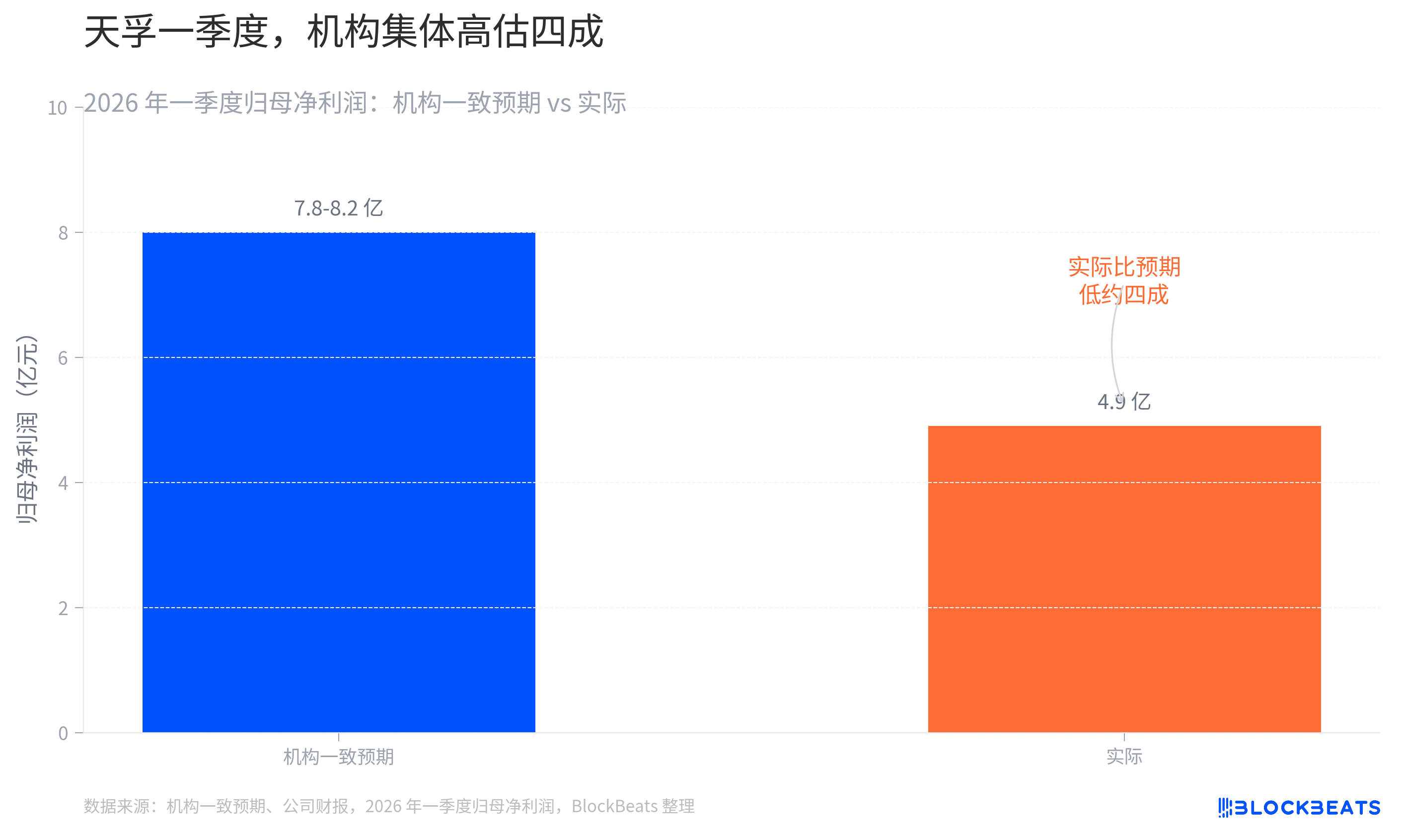

The lack of elasticity is because its growth is a stream, not a surge. Companies like Interjoy and NewEase directly benefit from AI capital expenditure surges, showing significant performance elasticity. Tianfu's growth is stable but flat. The high valuation is because the market has priced in this certainty to the skies. As of February 10, 2026, its trailing P/E ratio is about 122 times, much higher than the other two. And the ease of disappointment, in the first quarter of 2026, just went through a bloody example. Institutions unanimously expected its quarterly net profit to be between 780 million and 820 million yuan, but the actual figure was only 490 million yuan. The huge gap is the result of institutions applying the surge logic of a module factory to an optoelectronics company.

This precisely reminds everyone who wants to rank Tianfu with the other two: Tianfu and the other two are not the same. Using the logic of selling complete machines to price engine sales is a misinterpretation in itself.

At this point, the three companies have been dissected. But the "cost-effectiveness" issue still has a hidden variable that everyone has overlooked.

The Profit Pool is Not in Their Hands

Returning to that poker table, ask a more ruthless question: Is the money Yizhongtian earns really "good money"?

The essence of optoelectronic modules is system integration. Procuring optical chips, electrical chips, and optical components, and then using packaging processes to assemble them into a complete module. The barrier is not in the assembly itself. The real profit pool and moat are concentrated at both ends of the industry chain: the upstream laser chips and switching chips. The part dominated by Chinese manufacturers is the intermediate assembly process.

Therefore, when many people talk about "Interjoy surpassing Lumentum and Coherent," it needs to be viewed in two layers. In terms of module market share, it is valid. Interjoy did indeed outperform these two long-standing American manufacturers. But in terms of profit quality, it's a different story.

Lumentum and Coherent are guarding the upstream. They hedge against supply chain risks through vertically integrated laser chip supplies, and the advantages of III-V platforms such as indium phosphide and gallium arsenide in high-power applications still exist to this day. And these two are by no means defeated underdogs; they are upstream players who are rapidly recovering. In the first quarter of the 2026 fiscal year, Lumentum's revenue increased by 58% year-on-year, and its gross margin rose from 28% to 34%.

Coherent achieved a quarterly revenue of $1.81 billion, a 21% year-over-year growth. The data center and communications business accounted for over 70% of total revenue, with a growth of over 40% year-over-year. The non-GAAP gross margin reached 39.6%.

What's even more intriguing is coming up next. Yizhongtian's bet on a trillion-dollar valuation is based on the CPO architecture switch. And CPO relies on CW sources and indium phosphide substrates, both of which happen to belong to American fabs. Coherent is doubling its indium phosphide production capacity, with its facility in Sherman, Texas, being the world's most advanced indium phosphide production line, specifically designed to scale up CW laser diodes for solutions like NVIDIA's CPO.

The more Yizhongtian bets on architectural upgrades, the more he is expanding the territory for upstream American chip fabs. That's why Yizhongtian earns money from assembly and components, while Coherent and Lumentum earn money from chips. The latter is thinner, slower, but more enduring.

This is also why everyone associates "Swept High-Power Laser" with "Yizhongtian." Swept Technology represents the effort of domestic laser chip manufacturers to climb upstream in the industry chain. Its 100G EML has passed customer validation in 2025, entered mass production in 2026, and the CW 100mW high-power light source has also achieved mass delivery, with first-quarter revenue growing over threefold year-over-year. If this layer can truly break through in EML, high-power laser chip, the most profitable bottleneck, then "Yizhongtian's" moat extends from assembly to chips, and the binding becomes solid. If it can't climb up, no matter how high the cost-effectiveness, it's just hard-earned money.

This is the true hidden variable to measure the long-term cost-effectiveness of the three companies, not whose PEG is lower, but whether China's optical module industry can snatch the profit pool from the upstream.

Whether time will prove the value of optical modules and computing power, no one knows. But at the very least, those standing in the light should first think about which beam they are standing in.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia