Abstract

The crypto industry constantly talks about the lack of users, but the data tells a different story. The active users of consumer-grade crypto have long exceeded tens of millions, they are just not in the sight of Silicon Valley and New York. These people in Manila, Lagos, Buenos Aires, and Hanoi are using Coins.ph (18 million users), MiniPay (4.2 million weekly active users), Lemon Cash (Argentina's #1 app) daily, yet they have been hardly covered by English media.

Conversely, the protocols that Western VCs discuss every day have a daily active volume that is not even enough for one hour of Tron's shadow settlement network.

Seven Key Takeaways: The user issue in crypto is fundamentally a geographical issue; Tron is the most important consumer-grade public chain, but no one talks about it in NYC and SF; on-chain e-commerce is virtually non-existent; the biggest prediction markets are centralized; revenue and user numbers often move in opposite directions; the perpetual DEX battle has ended; genuinely profitable consumer-grade crypto companies do exist—they just don't look like DeFi.

Payments and Neo-Banking: Users have long existed, just not in the VC's line of sight

Common Understanding: Crypto needs to go mainstream, bring in the next billion users, and wallet UX is the bottleneck.

Data Shows: The next billion users are already here, and the biggest bottleneck is not user acquisition, but monetization.

First, let's look at the current scale. The Telegram Wallet claims to have 150 million registered users (unverified—low confidence level), but let's put that number aside. Focusing only on verified data, the user base is already very impressive:

Coins.ph has 18 million confirmed users in the Philippines, mainly operating on the Tron-based USDT track; MiniPay, as Opera's mobile stablecoin wallet on Celo, had 14 million registered users and 4.23 million weekly active USDT users as of March 2026, with a monthly transaction volume of $153 million, experiencing a 506% year-over-year on-chain activity growth (high confidence level—disclosed by Tether/Opera/Celo consortium).

Chipper Cash, with 7 million users across 9 African countries, recently achieved positive cash flow. Lemon Cash has been downloaded 5.4 million times and ranks as the top financial app in Argentina and Peru, with its monthly active users quadrupling since 2021. In Nigeria, Paga processes an annual transaction volume of 17 trillion Naira, but the share related to crypto is unclear (medium confidence).

The only payment company currently scaling revenue in tandem is RedotPay: with 6 million users, $158 million in annual revenue, $10 billion in annual transaction volume, and a valuation that has increased 16x since its seed round (high confidence—The Block, CoinDesk, company disclosure).

RedotPay operates as a crypto-to-fiat card processor focused on the Asia-Pacific region, earning transaction fees and bearing zero chargeback risk—it is essentially a crypto-native Visa issuing-acquiring entity. It is currently the clearest case proving that consumer-grade crypto can achieve real, recurring, non-incentivized revenue at scale.

Another revenue standout is Exodus, which, as per its SEC 8-K filing, is projected to reach $121.6 million in revenue by 2025 (high confidence), making it one of the few audited consumer-facing crypto companies publicly listed on the US stock market. Its revenue is derived from fees on exchanges and staking by 1.5 million monthly active users, with its stock trading under the symbol EXOD on the NYSE.

The Cash product from Ether.fi is the most notable DeFi-native entrant: profitable in its first year, with over 70,000 cards issued, Cash currently contributes about 50% of total revenue, generating monthly revenue of $2.8 million (high confidence—TokenTerminal daily verified). It demonstrates that a DeFi protocol is capable of delivering a truly consumer-grade product—albeit its total user base of 200,000 remains niche.

The customer acquisition problem in emerging markets has been solved, but the monetization challenge remains. The stark disparity between MiniPay's 4.2 million weekly active users and its undisclosed (presumed minimal) revenue stands out as one of the largest unresolved issues in the crypto industry—and also represents its biggest opportunity.

Marginal Improvement vs. Non-Incremental Value: Fine-Tuning Screening Criteria

A common argument against consumer-grade crypto investment is that crypto must offer non-incremental value relative to fiat solutions to offset integration costs. Data suggests that this framing of the test itself is flawed. Consider the two clearest data points in the payment category. The advantages of MiniPay over traditional mobile money products like M-Pesa are, at most, marginal in the hands of users—slightly cheaper transfers, slightly wider USD exposure, slightly broader cross-border coverage. It has 4.2 million weekly active users but minimal revenue. RedotPay's advantages over traditional Visa issuing-acquiring entities are likewise marginal in terms of consumer experience—swiping a card, buying a hot dog—but the underlying mechanics are structurally different: zero chargeback risk, instant cross-border settlements, no reliance on correspondent banks. RedotPay generates $158 million in annual revenue from its 6 million users.

Both products have been successfully validated and have achieved Product-Market Fit (PMF). The difference lies in the fact that RedotPay's "marginal yet structural" advantage can compound into pricing power, while MiniPay's "marginal and superficial" advantage cannot. Zero chargebacks are not a feature that users will notice, but they represent approximately a 1.5% gross margin captured by the issuing bank on every transaction. Slightly cheaper transfers are something users will only pay attention to once and then take for granted.

Therefore, the right filtering question is not "Is this not incremental?" but "Does this marginal improvement map to a structural feature of unit economics?" If the answer is yes—chargeback risk, settlement efficiency, correspondent banking, capital efficiency, custody costs—then a product that feels almost unchanged to the user can still compound into a substantial business. If the answer is no, then a product, even with tens of millions of users, lacks investment value. Both consumer-grade crypto categories have suffered from being conflated, causing the entire category to miss out on a generation of capital.

E-commerce

Common Belief: Crypto payments are gradually being adopted by e-commerce, it's just a matter of time.

Data Shows: There is not a single on-chain e-commerce protocol on DeFiLlama with daily protocol revenue exceeding $10,000. Not "sparse," but literally zero.

This chapter is not about a showdown between early competitors, but rather the absence of competitors. After auditing all protocols tracked by DeFiLlama and TokenTerminal, as well as all companies with public disclosures, we found only one noteworthy player: Travala, a centralized travel booking platform, with reported revenue of $7.17 million in February 2026 (medium confidence—self-reported, not independently verified). Travala is not a protocol; it is a travel agency accepting cryptocurrency.

UQUID claims to have 220 million users and 50 million monthly visits (the 220 million figure actually represents users of partner platforms—such as Binance—rather than UQUID's own users). The headline numbers are misleading, but their product catalog is indeed extensive—175 million physical items, 546,000 digital items—with Tron's share of their transaction volume doubling to 39% in the first half of 2025, and 54% of transactions priced in USDT-TRC20. However, there are no publicly disclosed revenue figures, and the user numbers are also questionable.

Gift card and voucher service provider Bitrefill has a monthly revenue of approximately $1 million (low confidence estimate — Growjo's estimation, historically inaccurate). There are no other notable on-chain ecommerce protocols to mention.

What truly exists is a shadow ecommerce economy running on the Tron USDT track — but it's P2P, entirely informal. Coins.ph facilitates overseas Filipino remittances, channeling funds into retail consumption. Nigeria's P2P ecosystem sees $59 billion in annual crypto transaction volume through OTC desks and USD savings accounts (from Chainalysis), serving as an alternative to the broken banking system. In Argentina, SUBE public transport top-ups are done through Tron USDT and cash OTC channels. Vietnamese freelancers are paid in TRC-20 USDT, then exchange it through a local P2P network.

This is real economic activity — but it is not ecommerce infrastructure. No protocol truly captures any part of it. The entire ecommerce stack native to crypto — product selection, checkout, custody, fulfillment tracking, dispute resolution, loyalty points — is almost entirely blank.

How much of these demands will remain after compliance?

Before declaring this as crypto's biggest product gap, a more challenging question must be answered: How much of the existing demand is structural, and how much is regulatory arbitrage? An honest assessment is that the vast majority is regulatory arbitrage.

Today, mainstream use cases on the Tron-USDT ecommerce track fall into three categories: USD exposure demand from users in capital control areas (Argentina, Venezuela, Nigeria) — these users cannot legally hold USD through traditional channels; VAT, sales tax, and import duty evasion, especially on digital goods and gift cards — tax authorities find it difficult to verify buyer identities; and cross-border freelance and gig economy payments bypassing bank controls — primarily in Vietnam, Iran, and parts of Africa.

UQUID's product catalog heavily leans towards gift cards, mobile top-ups, and digital goods — these categories exist precisely because they can convert opaque crypto balances into spendable fiat equivalents with almost no identity friction.

This is crucial for the investment thesis, as the survival rate of regulatory arbitrage demand under compliance varies greatly. Domestic VAT and tax evasion demand goes to zero at the moment merchants enforce KYC at the checkout — these users are not paying for a better checkout experience but for the "no tax ID" field, which immediately loses its value once a tax ID is requested. FX control evasion demands are more enduring, as their underlying issues (Argentina's capital controls, Nigeria's naira controls, Venezuela's bolivar) are structural and long-standing.

However, platforms serving these needs cannot legally operate within the required corridors. They can scale but cannot register, cannot engage in priced financing, nor can they collaborate with local fintech issuers—a key factor in establishing their moat.

The opportunity for survival within compliance is narrow but real.

Traditional slow or expensive cross-border merchant settlement—Latin America to Asia, Africa to anywhere, freelancer payments—can operate under any regulatory framework, as the underlying value proposition is "Stablecoins offer a cheaper track than SWIFT structurally," not "Stablecoins help you bypass the rules."

B2B settlements between small businesses in different jurisdictions also fall into this category. The merchant settlement for cross-border digital services is the same.

Therefore, the concept of a "global $5 trillion e-commerce" miscalculates this opportunity. The truly investable space is closer to the $200 billion to $400 billion cross-border B2B and freelancer payment market—whose value proposition can transition from the gray area to the legitimate market. Domestic encrypted checkout for Western consumers—what most refer to as "crypto payments"—is not this opportunity and never has been.

Winning in this category of agreements will look more like the "Stablecoin version of Wise" rather than the "Crypto version of Shopify." For investors, the key question is whether a team is building for a market that is surviving or one that is about to disappear.

Speculation: The Perpetual Battle Has Long Been Over

Common Understanding: Decentralized perpetuals are a competitive market, with dYdX, GMX, and others vying for market share against Hyperliquid.

Data Shows: Hyperliquid has emerged victorious. GMX and dYdX are not competitors but protocols in a terminal decline.

Hyperliquid currently controls over 70% of all on-chain perpetual venue open interest, with a monthly nominal trading volume of $1.05 trillion and a March fee income of $58.8 million—an annualized figure exceeding $640 million (High Confidence—TokenTerminal, DeFiLlama, Dune). During the most recent reporting period, its fees increased by 56% WoW. It has executed over $800 million in HYPE buybacks, making it one of the few protocols where value capture is not just talk.

Comparing with the established player. GMX has a daily revenue of $5,000 with approximately 500 daily active users. dYdX has a daily revenue of $10,000 to $13,000 with 1,300 daily active users, experiencing an 84% year-on-year fee reduction. This is not a struggling competitor—this is an agreement where the race has ended mathematically rather than strategically.

Noteworthy data about edgeX: Verified 30-day fee revenue of $14.7 million, fee retention rate of 73%, operating on StarkEx ZK-rollup. A previous dataset error showed $2.5 million initially—correcting it, edgeX now firmly holds the second position in on-chain perpetual venues by revenue rankings (high confidence—TokenTerminal daily verification). Whether edgeX can sustain its growth or follow the path of GMX/dYdX is the only unanswered question in this category.

The reason Hyperliquid is worth analyzing is that its success is not based on a better trading UX—the difference in order execution compared to GMX or dYdX is real but marginal. It wins in terms of liquidity depth, listing speed, and brand.

Once perpetual liquidity consolidates into a venue, network effects are nearly unshakeable: traders go where the spread is narrowest, the narrowest spread is where the highest volume is, and the volume loops back to where the traders are. The perpetual DEX category has gone through the winner-takes-all phase, and deploying capital against Hyperliquid in this category is akin to burning money.

Prediction Markets: This is a story of category selection, not decentralization

Another speculative category worth examining is prediction markets, where the mainstream narrative has been validated by Polymarket in the on-chain prediction market space. The data tells a different story—one whose lessons have nothing to do with decentralization.

· Kalshi is for off-chain/class CEX. The comparison itself is where the insight lies.

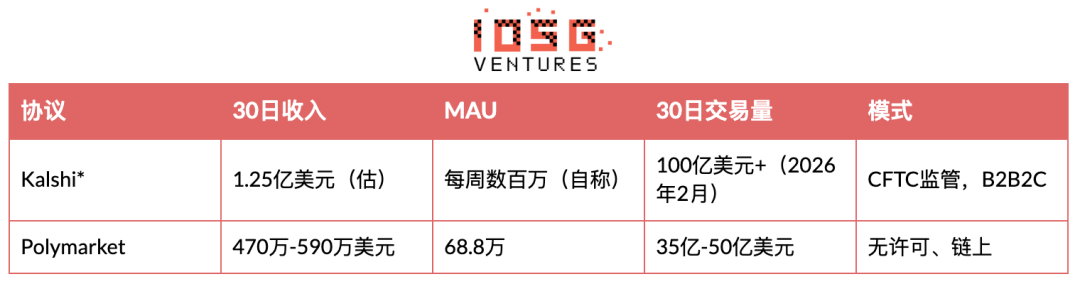

According to Bloomberg's report (high confidence), as of March 2026, Kalshi has achieved an annualized revenue of $1.5 billion, with a valuation of $22 billion. In February 2026 alone, it processed over $10 billion in volume, with trading volume increasing 12x in six months. Sports betting accounts for 89% of its revenue. On-chain alternative Polymarket has a monthly revenue of $4.7 million to $5.9 million, with 688,000 monthly active users. Kalshi's monthly revenue is approximately 25 times that of Polymarket.

The lazy explanation is that Polymarket has UX issues. From most product dimensions, Polymarket is the better-built side—cleaner order book, faster settlement, and even a more mature trader experience compared to Kalshi. The UX argument cannot justify a 25x revenue difference. The defense that Polymarket "hasn't started charging yet" actually makes the comparison worse, not better: if Polymarket is losing by 25 to 1 even with no fees, the underlying revenue potential gap will only be larger than the surface numbers.

The real explanation lies in category choice, distribution channels, and jurisdictional positioning—three things completely unrelated to decentralization.

Kalshi chose sports. Sports is a high-frequency, mass-market, structurally frequent category: there are betting opportunities every week, every day, every year, with commonly understood rules, and audiences self-refresh with each new season. Polymarket positioned itself in politics and event markets—these are dispersed, election-cycle-dependent, and structurally low-frequency. For Polymarket users who arrived for the 2024 election, there is no reason to come back in March 2026.

For Kalshi users for NFL, there is a reason to come back every Sunday. Ongoing engagement compounds into liquidity, liquidity compounds into spreads, spreads compound into more users. Polymarket chose the wrong end of the flywheel.

The second factor is distribution. Kalshi adopted a B2B2C model, integrating the order book with brokerage platforms, fintech apps, and partner integrations, rather than relying solely on direct-to-consumer acquisition. Polymarket is DTC-only, with every active trader bearing the full marketing cost.

Crucially, Kalshi is legally operating under CFTC regulation within the U.S., while Polymarket—following the settlement with the same agency in 2022—completely geoblocks U.S. users. The largest English prediction market audience structurally cannot be reached by an on-chain product. Kalshi not only excels in execution; it has access to a market from which Polymarket is legally barred.

The insights for evaluating prediction market projects are very specific. The right due diligence questions are:

(1) How frequent is the participation in the selected category;

(2) Does the project have a B2B2C distribution path, or does it rely on direct customer acquisition;

(3) What is the regulatory stance in the largest addressable market.

The level of decentralization is largely irrelevant to the outcome. Polymarket lost 25 to 1 because of a wrong category choice, wrong distribution model, and wrong jurisdictional choice—in roughly that order of importance.

Implication of this Chapter

The speculation sector has two key points:

(1) Once a category has produced a winner, it has truly produced a winner, and capital should not flow there anymore;

(2) The winning mechanism is not decentralization, UX, or tokenomics—it perpetually relies on liquidity concentration, and the prediction market relies on category selection plus distribution.

Both conclusions point towards the DeFi mullet proposition: the most defensible consumer-side positioning is to wrap a compliant front end around a crypto-native backend. Ether.fi Cash is the cleanest present-day case study. CrediFi and next-gen adjacent to payments all fit this model.

Stablecoin Infrastructure: Tron Is the Most Important Consumer-Grade Public Chain That No One Talks About

Common Knowledge: Ethereum L2 and Solana are the main consumer-grade public chains, with Tron being seen as a legacy network primarily used for low-cost transactions.

Data Shows: Tron's monthly stablecoin transaction volume is over $600 billion—comparable to Visa—with 14.3 million MAU, 72.8 million USDT holders, and a stablecoin velocity ratio of 0.2–0.3x—proving its activity is more for payments than speculation. It has an entire unmarked shadow economy of protocols, completely uncovered by Western media.

The numbers are staggering. The USDT-TRC20 supply on Tron is $86.4 billion. Monthly transaction volume ranges between $600 billion and $1.35 trillion (lower limit high confidence—TronScan, TokenTerminal; upper limit includes recycled volume). On March 29, 2026, the daily transaction volume reached $44.9 billion. The network processes over 2 million transactions daily, reaching 14.3 million MAU, with an estimated 80% of transaction volume below $1,000, of which 60%–70% are below $100. This is a retail payment network, not a whale-dominated settlement layer.

The velocity metric is a key analytical signal. Tron's USDT velocity is 0.2–0.3x, meaning that on Tron, each USDT takes about 3 to 5 months to turnover on average. In contrast to speculative chains, the velocity can exceed 10x—rapidly circulating between DeFi protocols, leverage positions, and Launchpads. Tron's stable, slow velocity is a characteristic of the payments track: money comes in, used for one real-world transaction, then sits in a wallet awaiting the next bill or remittance. The top ten USDT holders on Tron only control 8.7% of the supply—indicating broad and decentralized retail distribution.

Next is the shadow economy. Our audit of TronScan identified several protocols that are unlabeled, generate significant income, but have absolutely no English documentation:

CatFee has a daily fee of $82,000. No one in the Western crypto media knows what it is. TRONSAVE generates $863,000 in monthly revenue, all parties unidentified. These protocols operate in the shadow economies of Vietnam's P2P network, Nigeria's OTC countertop, the Philippines remittance corridors, and Latin America cash channels. We estimate that billions of dollars flow through these unlabeled clearinghouses daily—dynamic addresses, escrow settlements, and freelance payment infrastructure, effectively serving populations excluded from the traditional banking system.

Celo is the fastest-growing chain in this category, entirely driven by MiniPay's integration with Tether. Independent users grew by 506% year-on-year, with a total of 12.6 million wallets and a transaction volume of $153 million in December 2025 (high confidence). However, its scale is still only a fraction of Tron's.

Ethereum remains in the institutional settlement lane—high fees limiting retail use. Solana's stablecoin activity is led by trading and Launchpad traffic (pump.fun, Jupiter, Meteora), not payments. BNB Chain processes $600 billion in monthly stablecoin transaction volume, primarily for CEX settlements. TON is a variable—Telegram's wallet integration has brought a large number of registrations, but the depth of engagement remains unclear.

Sum Up: Regulatory Arbitrage Life Cycle and DeFi Mullet

Every successful consumer-grade encrypted category in this census has gone through the same curve. Starting with regulatory arbitrage; accumulating capital and users in the gray area; enduring — or not enduring — a compliance-driven event; and emerging from that, becoming a legitimate financial infrastructure. Protocols and companies generating real revenue today are at different stages of this lifecycle, and their position determines the risk and return curve of investment.

Phase 1 — Gray Area Launch. A protocol or service emerges to address a problem that traditional finance refuses or is unable to serve, almost always due to some regulatory constraint. Small user base, high technicality, can tolerate legal ambiguity. Profit margins are extremely high because regulatory risk is priced into the take. Tail risk is unlimited. Today's examples: Unmarked shadow clearinghouse on Tron (CatFee, TRONSAVE), Nigeria P2P USDT on the surface, and early pump.fun, NFT, and even Hyperliquid's early days.

Phase 2 — User and Capital Accumulation. PMF becomes indisputable. Transaction volume grows, users start coming from outside the core tech circle. Western media begins to take notice, but regulation has not yet taken action. Tron's USDT economy is currently in this stage today — 14.3 million MAU, monthly transaction volume exceeding $6 trillion. pump.fun in 2024, Polymarket in the 2024 election cycle, and Hyperliquid today are also in this stage.

Phase 3 — Compliance Transition. A single compliance-driven event — litigation, enforcement action, settlement, or proactive regulatory communication — pushes projects to choose legalization, fragmentation, or death. This is the stage with the highest variance and is the most analytically valuable from an investment perspective. Polymarket's 2022 settlement with the CFTC, pump.fun's $500 million lawsuit, and any future enforcement actions against offshore perpetual venues are all here. Most projects cannot complete this stage entirely.

Phase 4 — Legal Economy. The part that has crossed over becomes enduring, auditable, and financable. Returns are compressed because business is now valued at a fintech valuation rather than a moonshot project valuation. Kalshi (CFTC-regulated, $22 billion valuation), Exodus (NYSE American, SEC filing), Circle (S-1 disclosure), and RedotPay (financed at a fintech comparable multiple) are all here.

Once the arc is unfolded, the question of the timing of investment becomes tangible. Stage 1 offers the most upside potential, but is essentially off-limits to institutional capital—a single regulatory decree could wipe out the underlying business, making underwriting practically impossible. Stage 4 is already fully priced; the multiples are fintech multiples, and the asymmetry has disappeared. Stage 2 has historically been the stage with the best VC returns in this sector, but the prerequisite is a credible path through Stage 3. The due diligence issue in Stage 2 is no longer "Is the product viable?"—Stage 2 clearly is. The question is whether the business model can survive within compliance.

Tron's shadow protocols cannot pass this test because their very reason for existence is to circumvent compliance. Once Vietnam enforces KYC on Tron USDT liquidity, CatFee's daily fee of $82,000 immediately disappears—users are not paying for utility but for "anonymity." There is no compliant business model underneath. This is the fundamental difference between a "protocol with product-market fit" and a "protocol only fitting regulatory arbitrage." Both can generate revenue, but only one is investable.

The DeFi mullet thesis is a direct derivation from this framework. Products like Ether.fi Cash and the next generation of Latin American fintech win because they wrap a compliance frontend around a crypto-native backend. Users neither see nor care what the chain is. Regulators see a regular fintech. The protocol captures the economics of "the cheapest lane." These projects currently do not have a token launch—this itself is a signal: value capture happens at the equity layer rather than the token layer, and in this cycle, the institutional investors that emerge victorious will be those holding equity stakes rather than token shares.

The three recurring structural opportunities highlighted throughout this briefing are also directly derived from this synthesis:

The cash-out infrastructure in emerging markets (where users are present but revenue is not yet realized); the e-commerce rails for cross-border B2B and freelancer payments (the part that can survive within the e-commerce gap); and the Tron adjacent protocol ecosystem still in Stage 2 untouched, all best entered through the DeFi mullet model; all reward category selection over decentralization purity; all underrated today as Western capital is still looking at the wrong dashboard.

Data Quality Appendix

All data in this report is accompanied by one of the following three confidence ratings:

· High — multiple independent sources, verifiable on-chain, or regulatory filings (e.g., Exodus SEC 8-K, TokenTerminal Daily Validation, Tether/Bitfinex Joint Disclosure)

· Medium — single trusted source, self-reported by the company with some independent corroboration (e.g., Travala Self-reported Revenue, Coins.ph Latka Estimate)

· Low — press release, unverified statement, or Growjo-level estimation (e.g., Telegram 150 million registrations, UQUID 220 million users, Bitget 90 million users)