BitMEX co-founder Arthur Hayes delivered a speech at the Bitcoin 2026 conference, where he outlined his bullish view on Bitcoin, why Kevin Wadsworth is not the hawk people fear, and how an unnoticed April 1st banking regulation could unleash trillions of dollars in new credit.

In addition, Hayes proposed a year-end target price of $125,000 for Bitcoin and explained his "money printing during wartime" theory behind this target.

PANews has compiled the highlights of this speech, as follows:

Over the past few days, I have thought deeply about how monetary policy will evolve, taking into account AI development and the situation of the Iran war, leading to the content of this speech. It is clear that my stance has turned more bullish, and I will now explain the reasons for this.

Of course, we cannot ignore the ongoing war. Therefore, before delving into the core argument, I must establish a few assumptions.

First, we will not die in nuclear destruction; because once nuclear destruction occurs, any investment will become meaningless, so we will set aside this concern for now.

Second, the market will see this event as some kind of "short-term" event, whatever that may mean. It is now time to think about money creation, printing, and what this means for Bitcoin.

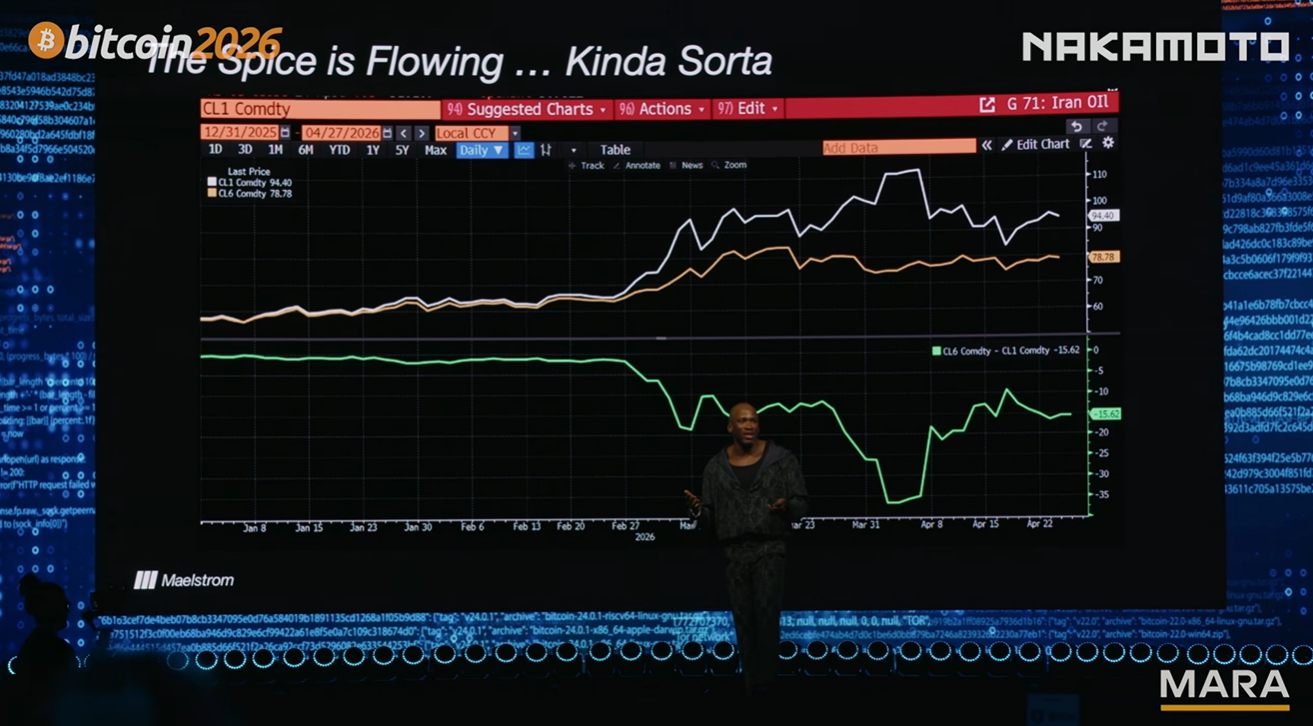

Every morning, I analyze the practical impact of the war on my investment portfolio through a chart on Bloomberg.

This chart shows the price difference between WTI crude oil six-month futures contracts and the spot-month contract. I do not care at all about the propaganda war between Trump and Iran; the only thing I care about is: whether there is enough commodity and oil flowing smoothly through the strait?

From the chart, the situation has improved, indicating that the front-end price is trending towards the back-end, which means that although the situation is bad, it is not as bad as it could be. So I can temporarily ignore it and continue to think about other things.

Every time I take the stage to speak, I always talk about money printing. From my last article about two weeks ago, my thoughts have changed. I believe that in the medium to long term, liquidity will turn positive. Therefore, if we consider it from a negative perspective, we will find that AI will bring about deflation.

There has been ongoing discussion about the potential unemployment of many knowledge workers due to highly efficient and low-cost models being able to perform knowledge work. Several months ago, I wrote an article outlining my expectations for these job losses. I believe this could result in losses of hundreds of billions of dollars for the banking system.

As for the Federal Reserve, more on that later.

The market is very concerned about Federal Reserve Chair nominee Kevin Worsh, with speculation on whether he is a hawk or a dove.

I will objectively analyze his remarks, essentially his remarks are neutral, having neither a positive nor negative impact on liquidity. Those market participants who are panicking about Worsh being a super hawkish Fed Chair have actually missed the signals behind it.

Finally, let's look at commercial bank lending. Why is commercial bank lending increasing? Why will the war economy in the U.S. and abroad lead banks to lend more to those involved in various weapon and related parts production? Additionally, changes in banking regulation will allow banks to increase the leverage on their balance sheets.

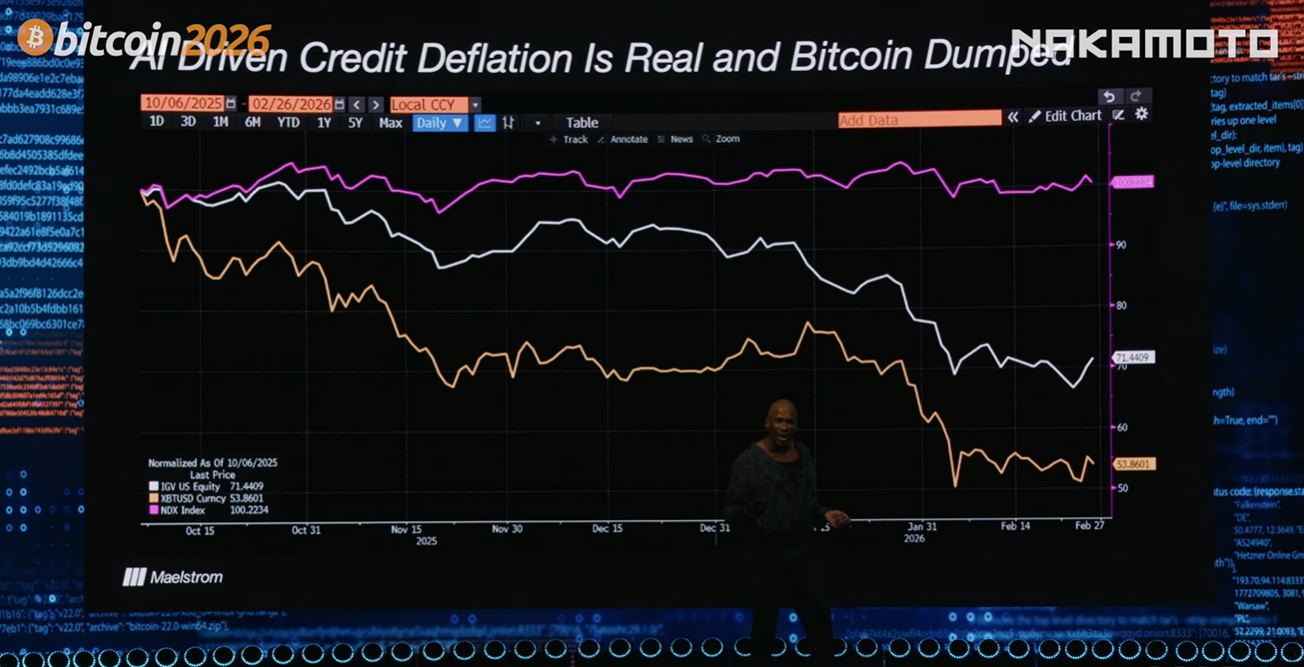

I have been monitoring this chart since October last year, with the magenta line representing the Nasdaq Index, the gold line representing the Bitcoin price, and the white line representing a U.S. tech stock ETF.

Now, most people, at least institutional investors, believe that the price of Bitcoin is nearing the Nasdaq Index, and over the past four to five years, it has indeed performed similarly. However, since Bitcoin hit a record high of $126,000 last October, it has fallen by about 50%, while the Nasdaq Index has remained stable. Large-cap tech stocks are doing fine.

But if you look closely at those tech stocks that have been hit hard, you will find they are almost all SaaS companies, whose products can now be completed with AI for just $10 per month, whereas they used to cost $10,000, or some other ridiculous high price.

These stocks have been devastated. I believe this foreshadows a credit tightening event, which central banks have not realized, as they have not printed enough money, and Bitcoin has been affected. This is the pre-war situation. The cutoff date for this chart is February 28.

My other wish is to fire all of my accountants and lawyers.

I have spent too much money on this. I am eager to have Claude take over everything. This will have a very bad effect on those who lend to high-salary individuals.

This is basically my take on AI becoming the new subprime crisis and what this could mean for the commercial banking system.

I believe it is this narrative that caused Bitcoin to drop from last October to the end of February during the US-Iran conflict.

But since the start of the war, Bitcoin has outperformed other stocks, surpassing the Nasdaq and SaaS stocks.

I think Bitcoin is now focused on wartime inflation.

Now that the US and many other countries have explicitly acknowledged that they are in a state of war, with inadequate defense spending, needing to print more money to make more bombs, what happens next?

So, let's set AI aside for now and talk about the Fed. In January this year, when Kevin Wash was nominated as Fed Chair, the market went into a panic. Since the 2008 financial crisis, he has been critical of the Fed's bloated balance sheet and openly stated his intentions to shrink the balance sheet and cut rates.

If you've read my articles, you know I've always argued that the quantity of money is more important than price. So I'm more concerned with his comments on the balance sheet than where short-term rates are headed.

If the market believes that Wash's tenure will reduce dollar liquidity in the market, they will be bearish on Bitcoin and other risk assets.

This is why we've recently seen the media talk about the "incoming super-hawk Fed Chair."

These regulations will restrict the way banks hold assets on their balance sheet and the capital they must hold for them.

But I don't think that will be the case. I believe the Fed will fundamentally shift reserves, treasuries, and repos onto the commercial banking system and operationalize it through new banking regulations.

These regulations will restrict the way banks hold assets on their balance sheet and the capital they must hold for them.

Finally, I think to understand Wash's impact on the Fed, it is most important to understand the very crucial constraint he faces, which is he must work closely with Treasury Secretary Scott Benson to ensure that any operation on the Fed's balance sheet does not impair Benson's ability to issue tens of billions of dollars in bonds.

Here is a very simplified balance sheet. There are no specific numbers here because I know this can be a bit complicated for some people. On the asset side, we have Treasury securities, Mortgage-Backed Securities (MBS), and Repurchase Agreements. These are tools that help people finance the purchase of Treasury securities. On the liability side, we have bank reserves, the Treasury General Account, government checking accounts, and currency in circulation.

Basically, from 2008 to the present, the Fed has increased the liability side with bank reserves and has purchased assets from the banking system.

These assets include Treasury securities, Mortgage-Backed Securities, and Repurchase Agreements. When Warren says the balance sheet is too big, he is referring to the Fed holding too many bonds, and he would like to shrink the balance sheet. So, he might sell bonds. But this would have a significant market impact.

Alternatively, I think what is currently implied is that he will engage in asset swaps with the U.S. banking system. The commercial banks' balance sheet, which is also the Fed's reserves, is considered an asset. There are around $30 trillion, and these reserves are all listed on the Fed's balance sheet. Their sources of funds include loans, deposits, and equity.

Therefore, for a certain size of the balance sheet, there must be a certain amount of equity to correspond to it. This is what is called the capital adequacy ratio. So, the Fed and the banks need to swap. The banks need to release reserves, reduce the demand for reserves, and use Treasury bonds and repurchase agreements to replace these reserves.

This is exactly what has been driven by the relaxation of regulations in the U.S. banking system. So, whenever you hear U.S. government currency officials talking about regulatory relief, what they mean is, we want to allow the banking system to absorb all the debt we create and remove it from the Fed's balance sheet.

The ultimate goal is for the U.S. commercial banks to take over the baton of currency creation from the Fed, with their balance sheets including Treasury bonds and repurchase agreements on the asset side and deposits and equity on the liability side.

The key to all of this is that the net impact on U.S. dollar liquidity is neutral.

Nothing is being sold, nothing is being bought, this is just a swap transaction. In terms of who can hold what, this is purely a regulatory workaround. But in the end, Powell can come out and tell everyone that he successfully reduced the Fed's balance sheet. But in reality, as investors, what we care about is the end result? In the end, there's no change.

Additionally, Powell will not clash with Bostic. They can just replace the photo with Powell's face instead of Powell's. At the end of the day, we have issued $38 trillion in debt, and the government needs funding. The Fed will do its job to ensure the markets function smoothly so that people can buy that debt.

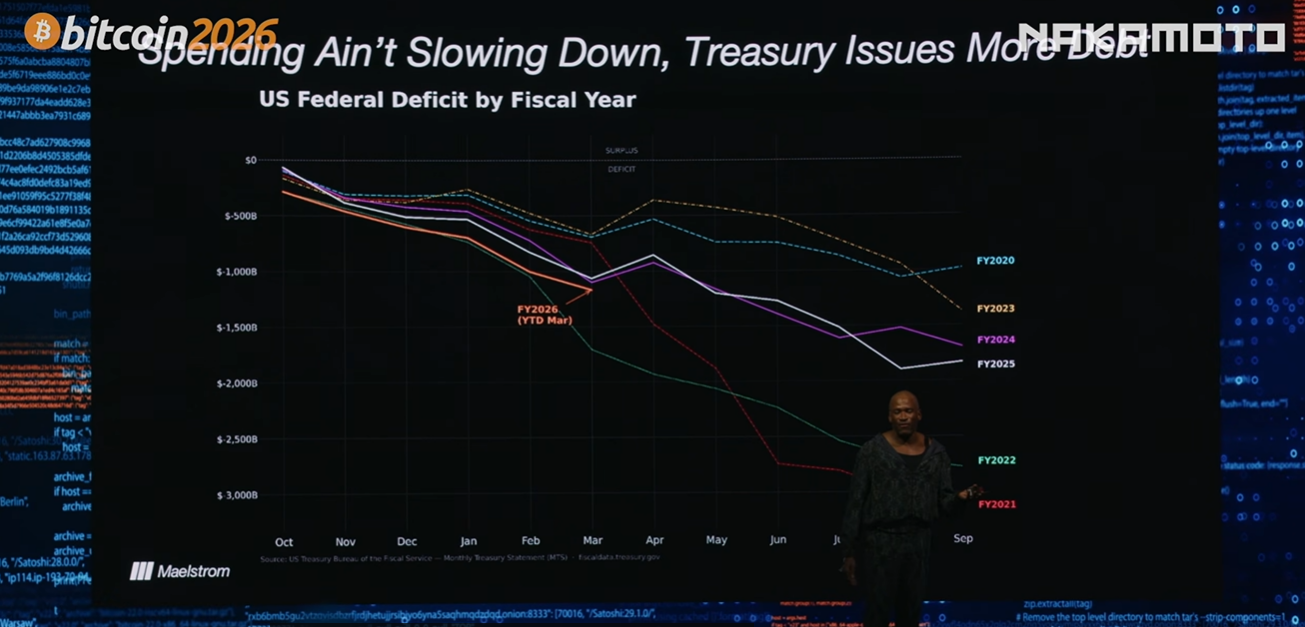

Let's now look at the expenditure side. Here is a chart for the current fiscal year, from October to the following September. As we can see, from the period of the COVID-19 pandemic to the presidential term, and now to the largest peacetime deficit in U.S. history, the 2026 fiscal year deficit is slightly higher than that of 2025.

The key point here is that the U.S. Treasury will not reduce spending. Trump did not mention significant spending cuts. The DOGE plan from last year has already been forgotten.

It's all wartime spending now. His new defense budget is 50% higher than before, reaching $1.5 trillion. This does not sound like the Treasury or politicians are looking to reduce spending together to allow the Fed to shrink its balance sheet.

Therefore, all the talk about the Fed shrinking its balance sheet doesn't make sense, as politicians and the Treasury behind them are continuously increasing the debt level.

Here is another chart. Who is buying this debt? The amount of debt purchased by foreigners is not as significant as before.

I have excluded countries that are usually engaged in basis trading for hedge funds. As we can see, the 25% share of debt held by foreigners has remained relatively stable, while the total debt has increased significantly. This implies the need for a new price-insensitive buyer to acquire all this debt, and this buyer is the U.S. commercial banking system.

The reason the banking system can increase its debt holdings is due to a new regulatory rule that just took effect on April 1 of this year: the Enhanced Supplementary Leverage Ratio (ESLR).

This new rule allows banks to hold less reserve capital and other types of assets to support their loans and other items on the balance sheet. This means that large banks like JPMorgan Chase and Citibank can issue more government bonds and repurchase agreements in the market and obtain extensions from the Fed.

And for small banks, which serve as the lending engine for the U.S. economy, they can increase the volume of commercial and industrial loans.

S&P Global estimates that this ESLR-induced balance sheet reduction will result in $1.3 trillion in new loans. So, why would banks have a demand for loans?

One criticism from some other macroeconomic analysts of this analysis is that they believe the banking system lacks demand, does not create enough loans, or that there is insufficient demand. However, there is a prime source of demand, the U.S. Department of Defense. They not only inject equity in certain transactions but also provide guarantees for underwriting production.

When a bank sees that a business has a guarantee customer like the government (which can print money), they will lend to them. They will also lend to resource miners who extract key resources needed for bomb manufacturing.

Lastly, all AI capital expenditures are now seen as a national security issue. Therefore, when a mega-cap company cannot debt finance itself with free cash flow and turns to market financing, they find large banks with massive balance sheets willing to provide debt backing.

So please pay close attention to construction industry loans, I believe you can receive relevant information weekly from the Fed.

The advantage of bank loans is that their multiplier effect is higher than central bank loans, and experience shows it is approximately three times higher. We have observed this through experience. This means that approximately $40 trillion in funds will be created, which is much greater than the credit losses that AI taking people's jobs could cause, which is also why I am more bullish on Bitcoin.

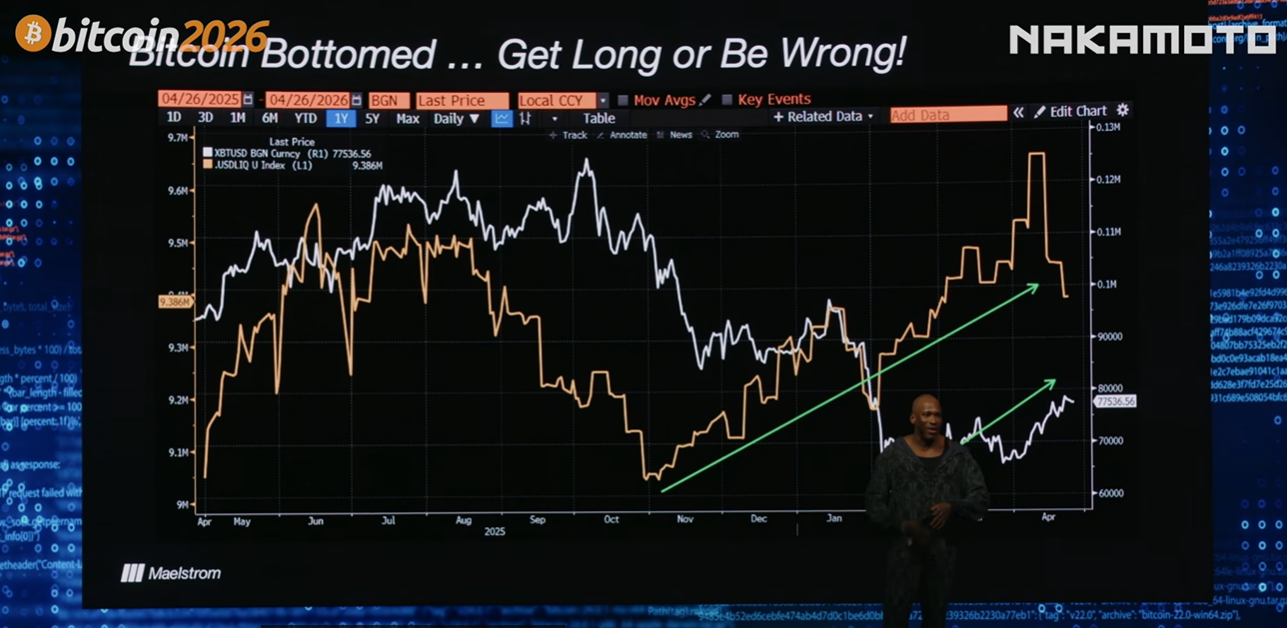

This liquidity chart reached its bottom in November last year, roughly the same time as Bitcoin. I think we have gone through some oscillation and some fluctuations. Now is the time for a breakthrough. That's why I believe Bitcoin will continue to rise. I think my year-end target price is around $125,000, but the specific number is not important either. Thank you, everyone.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia