Will copper become the new gold of this era?

Over the past two years, the market has understood AI infrastructure as a chip story. NVIDIA's GPUs, TSMC's capacity, HBM yields, CoWoS packaging bottlenecks—almost all discussions revolved around silicon. However, an AI data center is not simply about buying GPUs and plugging them in. It also requires grid connections, transformers, busbars, cables, liquid cooling systems, fiber interconnects, and a large amount of metal.

In the previous article "In the AI era, the "Great Famine" of Fiber Optics and Copper," we briefly discussed one thing: AI's demand is shifting from chips to fiber optics and copper.

This article will further delve into the narrative change of copper in the past year. Why does the market feel that copper is becoming more like gold? Why are macro funds starting to buy copper? Why are mining companies and commodity traders all saying "copper is not enough"? Why is it no longer just an industrial metal used to gauge the economic cycle?

Dr. Copper is not just a reflection of the manufacturing cycle anymore

In the English financial market, there is an old saying called Dr. Copper. This name implies that the price of copper, like an economic doctor, can diagnose the global economic situation in advance.

This is because the price of copper is inseparable from the manufacturing industry. When there is extensive property development in China, restocking in manufacturing, increased demand for appliances, automobiles, cables, pipes, etc., the price of copper rises. As the cycle goes down, copper also falls. The price of copper is fundamentally a reflection of China's real estate, global manufacturing, and trade cycles.

However, today copper's demand has new influencing variables: AI data centers, grid expansion, new energy vehicles, energy storage, military industry, and reindustrialization, all of which are increasing the structural demand for copper.

Anywhere electricity is used, copper is indispensable.

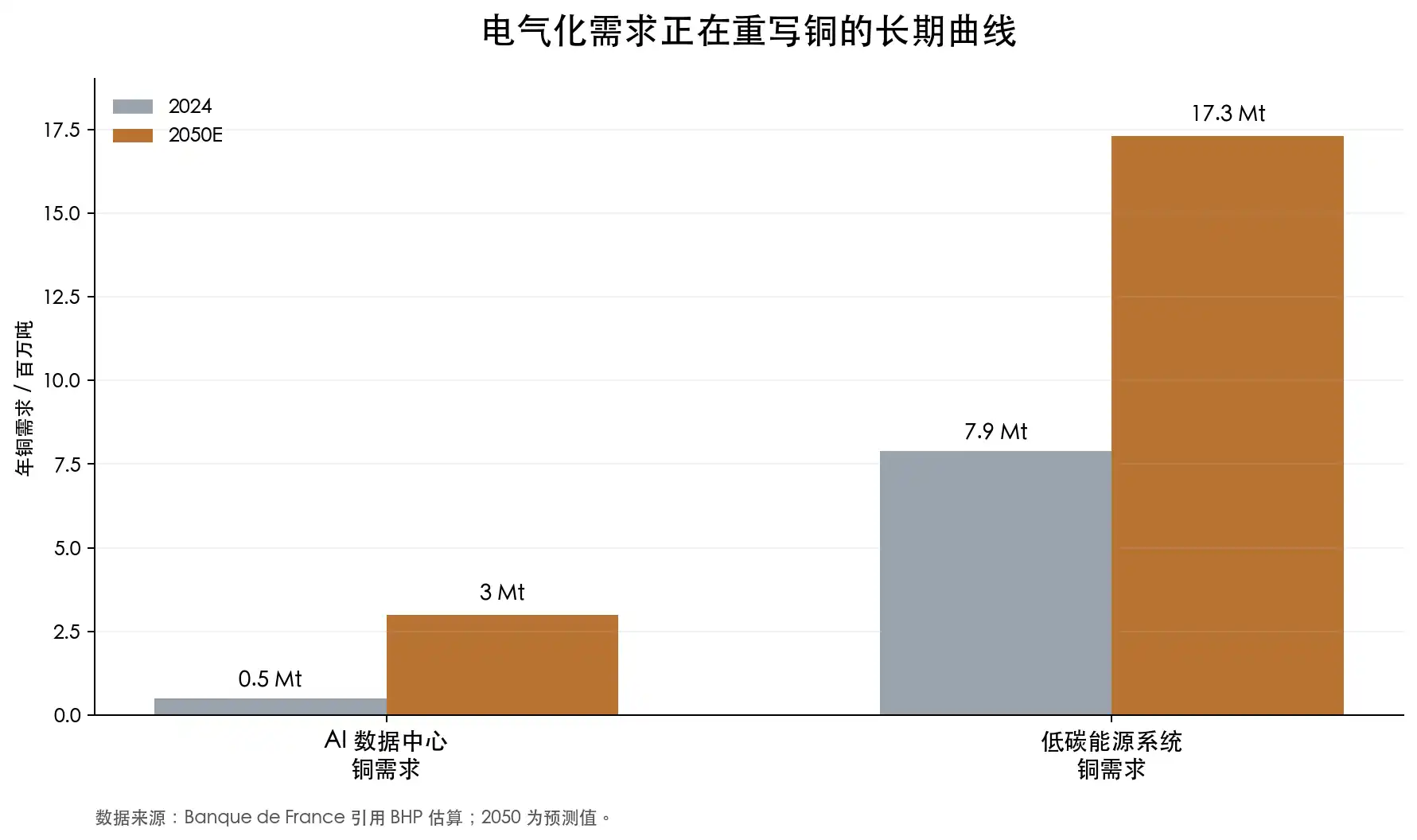

In an analysis by the Banque de France regarding AI data centers and the copper market, BHP's estimate is cited: the copper demand from AI data centers may increase from around 500,000 tons in 2024 to around 3 million tons in 2050. Concurrently, the copper demand from low-carbon energy systems may rise from 7.9 million tons to 17.3 million tons. The article also mentions a specific case: Microsoft's Chicago data center construction consumed 2,177 tons of copper.

Looking at this number alone, it is not particularly large in the global copper market. However, the key is not how much copper a single data center uses, but the fact that behind an AI data center is not a singular demand, but rather an entire set of power infrastructure requirements. The denser the GPU, the higher the cabinet power, making the data center more like a high-energy-consuming factory. A factory needs electricity, which requires a power grid, transformers, cables, busbars, switchgear, and cooling systems.

Of course, not all of copper's story can be simply attributed to AI.

Richard Holtum, CEO of global commodity trading giant Trafigura, reminded at the 2025 LME Week that data centers and defense are indeed hot, but the majority of copper demand in the next decade will still come from traditional infrastructure, construction, urbanization, and consumer goods. He also mentioned that copper used in air conditioning still exceeds that used in data centers.

This viewpoint gives us a new perspective: the increase in copper demand is not solely driven by AI, as its demand is expanding in almost all electricity usage scenarios simultaneously.

The Biggest Bull Case for Copper Is That It Can't Be Mined That Fast

Many people's first impression of copper is as an "industrial metal," always assuming that if the price rises, more mines will be dug, and supply will naturally increase. However, the reality is not so.

Large copper mines typically take over a decade from discovery, exploration, resource confirmation, feasibility studies, financing, permits, construction to production. An IEA report shows that new copper projects take an average of about 17 years from discovery to production. This means that if the market suddenly finds there is not enough copper in 2026, truly large-scale new supply may not appear in 2028 or 2029, with much of the supply waiting until the 2030s.

Robert Friedland, founder and co-chairman of Canadian mining company Ivanhoe Mines, has repeatedly emphasized this issue. He is one of the world's most prominent copper bulls and owns the world-class Kamoa-Kakula copper mine project in the DRC. His expression has always been quite aggressive: the world has not yet realized how much copper it actually needs. Over the past decade, the world has not prepared enough new copper mines for the electrification age.

This is not just his judgment. IEA data also supports this direction.

The average grade of global copper mines has dropped by about 40% since 1991. Grade decline means that in the past, more copper could be obtained from mining one ton of ore, whereas now, more ore needs to be mined, more electricity consumed, more water used, and more waste rock processed to obtain the same ton of copper. The IEA also mentions that in the past 35 years, only 5% of discovered copper deposits have occurred in the last decade. With few new discoveries, declining ore grades in old mines, longer project construction periods, and rising capital expenditures. The IEA estimates that based on the current project pipeline, the copper market could face a 30% supply shortfall by 2035.

So copper is not the kind of asset that sees immediate supply response after a price hike in a typical commodity cycle. Copper mining projects are becoming more like large-scale infrastructure projects: prospecting, permitting, community relations, water management, environmental impact assessments, and dealing with changes in resource-rich country tax policies.

Places like Chile, Peru, the Democratic Republic of the Congo, Zambia, Indonesia, and Mongolia all have significant copper resources but also various forms of political, tax, community, or operational risks. The more strategic copper is, the more incentive the resource-rich country has to increase its share of profits; the higher the copper price, the easier it is for mining companies to face higher taxes and renegotiation.

The smelting end is also facing tension.

After copper concentrate enters the smelter, it is processed into refined copper. Smelters charge treatment and refining fees, known in the industry as TC/RC, which stand for treatment charge and refining charge. Under normal circumstances, when the concentrate supply is sufficient, smelters have strong bargaining power, and TC/RC is high; when concentrate is tight, smelters compete for feedstock, and TC/RC decreases.

One unusual aspect of 2026 is that, despite the record-high copper price, smelting charges have dropped to historic lows. The IEA states that in 2026, the annual TC/RC benchmark fell to $0 per ton, and spot TC/RC has been negative since 2024.

This is more crucial than just looking at exchange inventories because the bottleneck for copper is not only in refined copper but also in mines and concentrates. If the upstream raw material is tight, even more smelters won't help. China has significantly expanded its copper smelting capacity over the past two decades, with the IEA stating that China accounted for over 90% of global copper smelting output growth since 2005 and is expected to represent about half of global copper smelting output by 2025. The midstream capacity is very strong, but with tight upstream mines, the fragility of the supply chain is magnified.

Gold's scarcity comes from reserves, extraction costs, and its monetary properties. Copper is certainly not gold, but as its new supply becomes slower, resources become more concentrated, and its strategic attributes become stronger, it is starting to have a kind of scarcity akin to gold.

Why Macro Funds Are Starting to Like Copper

Previously, copper was mainly in the realm of commodity traders and mining analysts. Now, it is increasingly attracting macro funds.

For example, Stanley Druckenmiller, one of America's most famous macro investors, who previously managed a quantum fund with Soros before establishing Duquesne Family Office. Known for making large-cycle, high-conviction trades, the market is now paying close attention to his views on AI, the US dollar, bonds, and commodities.

In a recent interview at Morgan Stanley, he mentioned that his portfolio has been primarily AI-driven in recent years, but has now shifted towards a more macro and geopolitical positioning. He talked about holding copper, betting against the US dollar, and also holding gold as a geopolitical hedge.

His logic is as follows: if the dollar weakens, dollar-denominated commodities will benefit. With an expanding fiscal deficit, continued government spending, and rising geopolitical risks, there is buying interest in gold; in the same environment, the renaissance of the grid, defense industry, AI data centers, energy systems, and manufacturing reshoring will also bring demand for physical assets, with copper positioned at the intersection of these trends.

Druckenmiller represents the perspective of macro funds, but there are even more aggressive expressions in the commodity trading circle.

One of the most typical is Pierre Andurand. He is a renowned European commodity hedge fund manager who started out in energy trading, co-founded BlueGold Capital, and later founded Andurand Capital. In an interview with the Financial Times, he made a very bold prediction: copper prices could soar to $40,000 per ton in the coming years.

Jeff Currie's views are also noteworthy. Jeff Currie, who was previously the head of commodity research at Goldman Sachs for many years before joining Carlyle, is one of the most influential figures on Wall Street in commodity research. He has long argued that "copper is the new oil," meaning that in the era of energy transition, copper may play a foundational role similar to oil in the old energy era. In 2024, he once again referred to copper as one of his highest-conviction trades.

There is also data showing money flowing in.

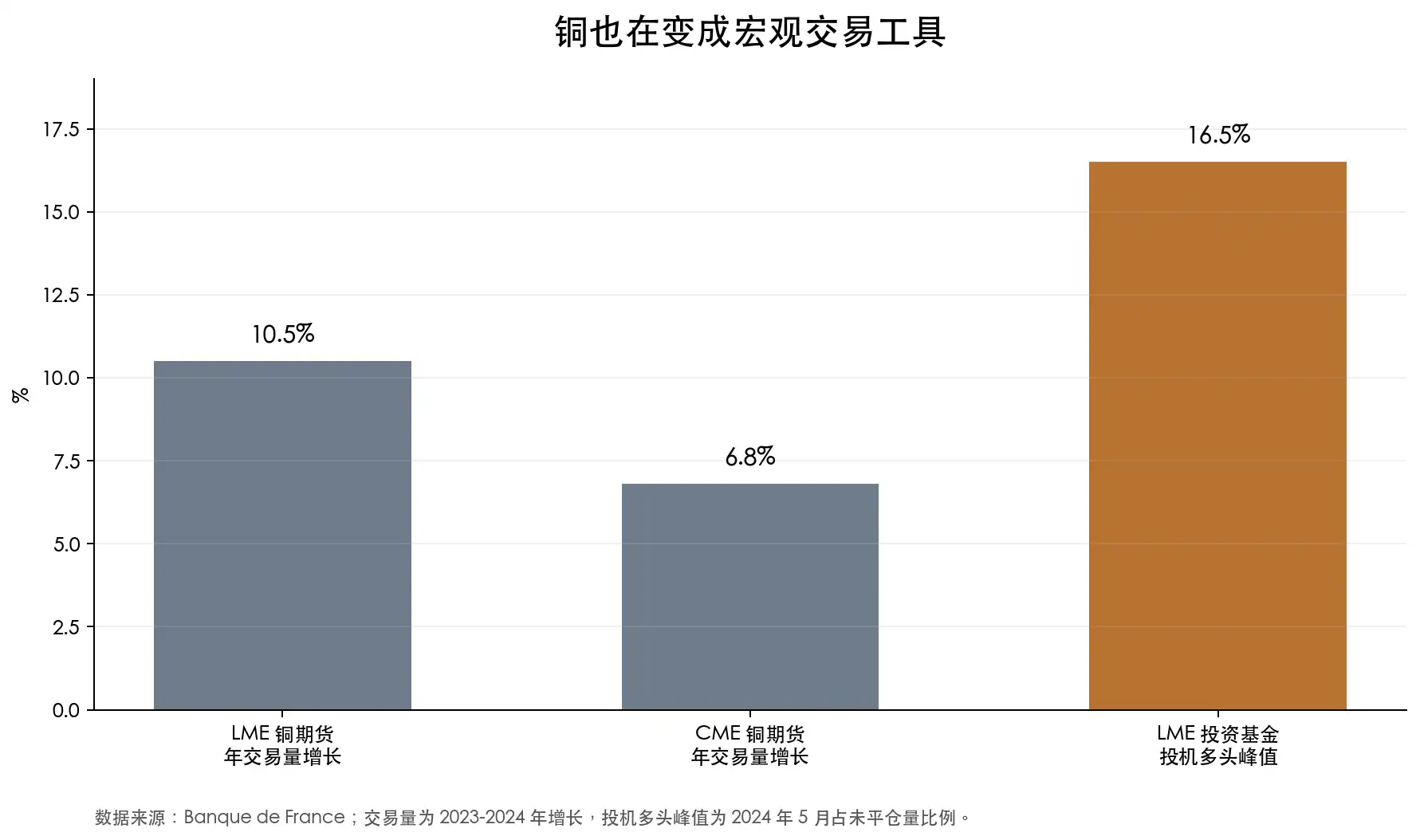

The Banque de France mentioned that from 2023 to 2024, LME copper futures' annual trading volume increased by 10.5%, CME copper futures' annual trading volume increased by 6.8%; in LME copper futures, speculative long positions from investment funds reached 16.5% of open interest in May 2024. This is not just physical restocking but financial funds treating copper as a macro trading tool.

Copper Mining Stocks: Leverage on Copper

During a gold bull market, gold stocks usually amplify gold price movements. Similarly, in a copper bull market, copper mining stocks also have a similar amplifier effect.

As copper prices rise, it creates cost pressure for end users. However, for mining companies that already have production capacity, this could lead to an expansion in profit margins. For example, if the copper price increases from $9,000 per ton to $12,000 per ton, and the mining company's cash costs do not rise in tandem, a significant portion of the additional $3,000 will directly flow into the profit statement. It is for this reason that copper mining stocks naturally possess operational leverage. As the copper price rises, a mining company's profits may increase even more; if the copper price falls back, profits may also contract more rapidly.

In the past two years, the market has already priced in this type of leverage trading.

Taking A-shares as an example, from June 2024 to June 2026, Luoyang Molybdenum is the most typical high-elasticity case. Its core focus is the copper-cobalt assets in the Congo, especially Tenke Fungurume and KFM. Based on the pre-adjusted closing price, Luoyang Molybdenum saw a price increase of about 129% during this two-year period, with a peak increase of nearly 260%. This performance is not typical of a cyclical stock but rather reflects the market's revaluation of overseas copper mining resources.

Companies like Jiangxi Copper, Tongling Nonferrous, and Yunnan Copper better demonstrate the volatility after the superimposition of copper prices and smelting attributes. Jiangxi Copper saw a price increase of about 82% during the period, with a peak increase of over 200%; Tongling Nonferrous saw a price increase of about 77%, with a peak increase of around 159%; Yunnan Copper only saw a price increase of about 29%, but with a peak increase of over 130%.

These stocks all illustrate another side of copper mining stocks: when the market is bullish, they exhibit significant elasticity; however, during market downturns, the pullback is sharp.

Looking at the retracement from the peak, the volatility is more evident. Yunnan Copper retraced about 45% from its interval peak, Jiangxi Copper retraced about 41%, while Luoyang Molybdenum, Northern Copper, and Zhijin Mining all experienced retracements of over 30%. Copper mining stocks do not solely reflect copper prices but are the result of the combined effect of copper prices, costs, inventory, TC/RC, project progress, resource country risks, and equity market sentiment.

In the U.S. stock market, the most typical representative of a copper mining stock is Freeport-McMoRan, with the ticker symbol FCX. It is one of the core copper producers in the United States, with assets including Morenci in the U.S., Cerro Verde in Peru, and Grasberg in Indonesia. Globally, FCX is one of the most commonly used U.S. stock instruments for copper price exposure. According to MarketWatch data, FCX reached a 52-week high of $72.09 on June 2, 2026, but experienced a single-day decline of 9.07% on June 5, retracting over 12% from the peak within a few days.

Southern Copper, with the ticker symbol SCCO, is another high-quality copper mining stock representative. Its assets are mainly in Peru and Mexico, with a high copper exposure and strong profitability. Earlier this year, IBD mentioned that SCCO had risen by 55% at one point and hit an all-time high. Compared to FCX, SCCO represents higher purity and better-profit quality copper mining assets, but it is also exposed to copper prices and resource country risks.

If investors prefer not to bet on a single company, they can also consider copper mining ETFs, such as the Global X Copper Miners ETF, which tracks global copper mining companies.

However, copper mining stocks are much more complex than copper itself.

The value of a mining company depends not only on the copper price, but also on ore grade, cash costs, reserve life, capital expenditures, location, national policies, tax regulations, labor relations, environmental permits, transportation conditions, and management execution. While the copper price can uplift the entire sector's valuation, significant divergences between companies will eventually emerge.

Country risk, especially, is crucial. Many high-quality copper mines are located in Chile, Peru, the Democratic Republic of the Congo, Zambia, Mongolia, and Indonesia. A favorable resource endowment does not guarantee stable shareholder returns. The higher the copper price, the more likely governments are to renegotiate royalties; the larger the project, the more challenging it becomes to address community, environmental, water usage, and infrastructure issues.

Cost inflation can also erode profits. During copper price upswings, energy, equipment, labor, steel, and financing costs often rise simultaneously. A seemingly attractive development project may end up not delivering much return to shareholders due to budget overruns, production delays, and permitting obstacles.

Early-stage copper mining companies carry higher risks. They focus on future reserves and future production, but each step—from resource estimation to proven reserves, from feasibility studies to financing, from permits to construction—holds the potential for failure. While the long-term logic of copper may hold true, not every copper mining stock will fulfill its promise.

Therefore, copper mining stocks are better understood as a leveraged expression of the copper price logic rather than a simple proxy for the price of copper itself. They can offer higher elasticity but also bring about more significant drawdowns. Companies worth studying are those with low costs, long mine life, clear expansion paths, robust balance sheets, and manageable political risks.

This is also part of the "goldification" of copper: the scarcity logic of copper is not limited to the spot and futures markets but is being repackaged by the stock market, ETFs, and speculative funds. While a copper price increase represents one layer of trading, an increase in copper mining stocks represents another layer. The former reflects the commodity itself, while the latter reflects how much the market is willing to imagine paying for this long-term scarcity.

The "Goldification" of Copper is Just Beginning

The world needs more electricity, and more electricity means more copper.

Of course, copper will not actually turn into gold. It does not have the same pure monetary properties as gold, and it is not immune to economic cycles. Global economic slowdowns, weakening manufacturing sectors, and cooling risk assets can all suppress the copper price. Copper will still fluctuate, possibly even dramatically.

However, what has changed is that the underlying logic of copper is no longer the same as before.

In the past, copper prices often experienced significant declines when demand weakened alongside supply surpluses. Today, the supply side is not as abundant. Factors such as aging mines, declining ore grades, longer permitting periods, smelters competing for raw materials, and resource-rich countries renegotiating profit-sharing have made copper increasingly difficult to categorize as a simple cyclical commodity.

It may still be an industrial metal, but it is no longer just a reflection of the industrial cycle.

The "goldification" of copper has only just begun.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia